PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998684

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998684

Battery Separators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

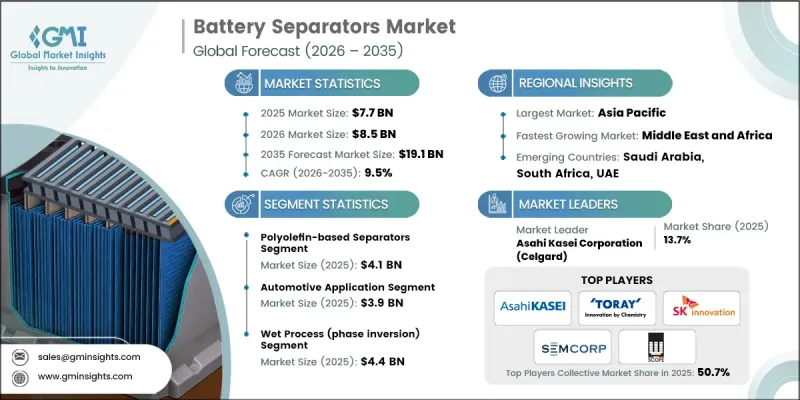

The Global Battery Separators Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 19.1 billion by 2035.

Market growth is driven by the increasing demand for high-performance and safe energy storage solutions across electric vehicles, consumer electronics, and industrial applications. Battery separators act as thin membranes that allow ion flow between anode and cathode while preventing direct electrical contact, ensuring safe operation and preventing short circuits that could lead to overheating or battery failure. These separators are typically made from polymeric materials such as polyethylene, polypropylene, and composite blends, designed to maintain thermal stability, chemical resistance, and mechanical strength across lithium-ion, lead-acid, and nickel-metal hydride batteries. Advanced separators incorporating ceramic coatings or nanostructures enhance thermal stability and electrolyte wettability, while ultra-thin designs reduce internal resistance, enabling higher power output without compromising safety. The push for high-energy-density batteries, fast-charging capabilities, and flexible wearable applications is further accelerating technological advancements and adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $19.1 Billion |

| CAGR | 9.5% |

The polyolefin-based separators segment reached USD 4.1 billion in 2025, offering affordability and chemical stability. Meanwhile, ceramic-coated and polymer-coated separators are gaining traction due to enhanced thermal protection and improved safety features. Aramid-based and nonwoven separators are increasingly used in high-performance batteries requiring long-lasting durability. Electrospun separators are emerging as advanced materials to support higher energy density, rapid charging, and flexible battery applications.

The lithium-ion battery separators segment generated USD 1 billion in 2025, reflecting their widespread use in electric vehicles, energy storage systems, and consumer electronics. Lead-acid battery separators remain essential for automotive starter batteries and industrial backup applications due to their cost-effectiveness and reliable performance.

North America Battery Separators Market is expected to grow from USD 1 billion in 2025 to USD 2.7 billion by 2035, driven by electric vehicle adoption, gigafactory development, supply chain restructuring, and government-backed initiatives supporting battery manufacturing. Research and development in high-safety and solid-state separators is positioning the region as a hub for next-generation energy storage solutions.

Prominent players in the Global Battery Separators Market include Asahi Kasei Corporation (Celgard), Toray Industries, Inc., SK Innovation Co., Ltd. (SK On), W-SCOPE Corporation, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, UBE Corporation, ENTEK International LLC, SEMCORP Co., Ltd., Arkema S.A., Solvay, Hollingsworth & Vose Company, Dreamweaver International, Blue Solutions (Bollore Group), Cangzhou Mingzhu Plastic Co., Ltd., Xinxiang Zhongke Science & Technology Co., Ltd., Shenzhen Senior Technology Material Co., Ltd. Key strategies employed by companies in the Global Battery Separators Market include investing in R&D to develop ultra-thin and high-safety separators, launching ceramic-coated and polymer-coated products, focusing on advanced lithium-ion and solid-state battery technologies, expanding manufacturing capacities through strategic partnerships and joint ventures, enhancing supply chain localization to ensure steady raw material availability, entering emerging markets with cost-effective solutions, providing technical support and training for battery manufacturers, integrating IoT-enabled monitoring for smart energy management, and promoting environmentally friendly and recyclable separator materials to align with sustainability trends.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material Type

- 2.2.2 Manufacturing Process

- 2.2.3 Thickness

- 2.2.4 Battery Chemistry

- 2.2.5 Application

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer interest in collagen-rich functional nutrition

- 3.2.1.2 Increasing adoption of paleo and keto lifestyles

- 3.2.1.3 Demand for dairy-free protein alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and sourcing costs

- 3.2.2.2 Limited appeal among vegetarian and vegan consumers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into ready-to-drink and convenience formats

- 3.2.3.2 Innovation in flavor enhancement and masking technologies

- 3.2.3.3 Growth in emerging health and wellness markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.1.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyolefin-based separators

- 5.2.1 Polypropylene (PP) separators

- 5.2.2 Polyethylene (PE) separators

- 5.2.3 Multi-layer PP/PE/PP separators

- 5.3 Ceramic-coated separators

- 5.3.1 Alumina (Al2O3) coated separators

- 5.3.2 Silica (SiO2) coated separators

- 5.3.3 Zirconia (ZrO2) coated separators

- 5.3.4 Boehmite coated separators

- 5.4 Polymer-coated separators

- 5.4.1 PVDF coated separators

- 5.4.2 PMMA coated separators

- 5.4.3 PVA coated separators

- 5.5 Aramid-based separators

- 5.5.1 Aramid nanofiber (ANF) separators

- 5.5.2 Meta-aramid nonwoven separators

- 5.5.3 Para-aramid composite separators

- 5.6 Nonwoven separators

- 5.6.1 Cellulose-based nonwoven separators

- 5.6.2 PET nonwoven separators

- 5.6.3 Glass fiber nonwoven separators

- 5.7 Electrospun separators

- 5.7.1 Nanofiber electrospun membranes

- 5.7.2 Composite electrospun separators

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Wet process (phase inversion)

- 6.2.1 Thermally induced phase separation (TIPS)

- 6.2.2 Non-solvent induced phase separation (NIPS)

- 6.3 Dry process (stretching)

- 6.3.1 Uniaxial stretching

- 6.3.2 Biaxial stretching

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Thickness, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ultra-thin separators (<12 µm)

- 7.3 Standard thickness separators (12-20 µm)

- 7.4 Thick separators (>20 µm)

Chapter 8 Market Estimates and Forecast, By Battery Chemistry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Lithium-ion battery separators

- 8.3 Lead-acid battery separators

- 8.4 Sodium-ion battery separators

- 8.5 Solid-state battery separators

- 8.6 Lithium-sulfur battery separators

Chapter 9 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Automotive applications

- 9.2.1 Battery electric vehicles (BEV)

- 9.2.2 Plug-in hybrid electric vehicles (PHEV)

- 9.2.3 Hybrid electric vehicles (HEV)

- 9.2.4 Electric two-wheelers

- 9.2.5 Electric commercial vehicles (buses, trucks)

- 9.2.6 Electric off-highway vehicles

- 9.2.7 Others

- 9.3 Consumer electronics

- 9.3.1 Smartphones

- 9.3.2 Laptops and tablets

- 9.3.3 Wearables (smartwatches, fitness trackers)

- 9.3.4 Power banks

- 9.3.5 E-cigarettes and vaping devices

- 9.3.6 Others

- 9.4 Energy storage systems (ESS)

- 9.4.1 Grid-scale energy storage

- 9.4.2 Residential energy storage

- 9.4.3 Commercial and industrial (C&I) storage

- 9.4.4 Utility-scale storage

- 9.4.5 Others

- 9.5 Industrial applications

- 9.5.1 Material handling equipment (forklifts)

- 9.5.2 UPS (uninterruptible power supply)

- 9.5.3 Telecom backup power

- 9.5.4 Medical devices

- 9.5.5 Others

- 9.6 Power tools and equipment

- 9.6.1 Cordless power tools

- 9.6.2 Garden equipment

- 9.6.3 Others

- 9.7 Marine and aerospace

- 9.7.1 Electric marine propulsion

- 9.7.2 Aerospace applications

- 9.7.3 Others

- 9.8 Renewable energy integration

- 9.8.1 Solar + storage systems

- 9.8.2 Wind + storage systems

- 9.8.3 Others

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Asahi Kasei Corporation (Celgard)

- 11.2 Toray Industries, Inc.

- 11.3 SK Innovation Co., Ltd. (SK On)

- 11.4 W-SCOPE Corporation

- 11.5 Sumitomo Chemical Co., Ltd.

- 11.6 Mitsubishi Chemical Group Corporation

- 11.7 UBE Corporation

- 11.8 ENTEK International LLC

- 11.9 SEMCORP Co., Ltd.

- 11.10 Arkema S.A.

- 11.11 Solvay S.A.

- 11.12 Hollingsworth & Vose Company

- 11.13 Dreamweaver International

- 11.14 Blue Solutions (Bollore Group)

- 11.15 Cangzhou Mingzhu Plastic Co., Ltd.

- 11.16 Xinxiang Zhongke Science & Technology Co., Ltd.

- 11.17 Shenzhen Senior Technology Material Co., Ltd.