PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998694

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998694

Europe E-Bike Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

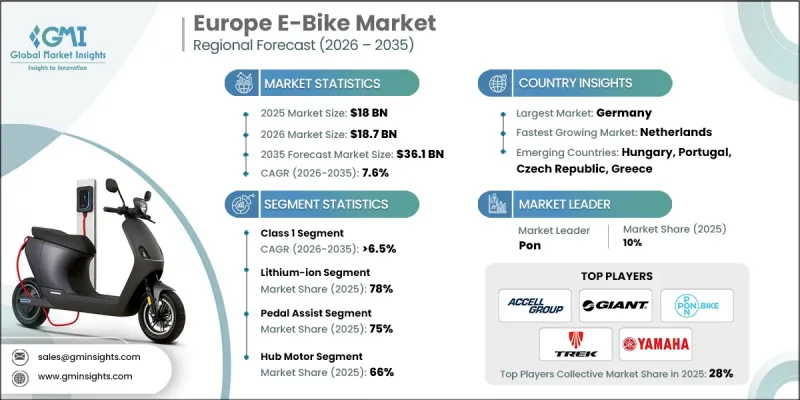

Europe E-Bike Market was valued at USD 18 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 36.1 billion by 2035.

Growing public awareness regarding environmentally responsible transportation options, combined with supportive mobility policies, is encouraging a wider transition toward electric bicycles. Many European governments have introduced financial incentives, policy frameworks, and regulatory support that make electric bikes more accessible to everyday commuters. These initiatives are reinforcing the role of e-bikes as a practical alternative to conventional urban transport. At the same time, urban mobility programs focused on reducing emissions and improving traffic efficiency are encouraging residents to adopt low-emission personal transportation options. Restrictions on conventional vehicles in certain urban areas and the expansion of cycling infrastructure are also contributing to the growing appeal of electric bicycles. As cities continue prioritizing cleaner mobility solutions and modern transportation planning, the Europe e-bike market is evolving into a significant component of the region's sustainable mobility ecosystem, supporting both personal commuting and broader environmental goals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18 Billion |

| Forecast Value | $36.1 Billion |

| CAGR | 7.6% |

Another important driver influencing the growth of the Europe e-bike market is the rapid expansion of online retail and last-mile delivery services. The rise in digital shopping activity has increased the need for efficient urban logistics solutions capable of operating within dense city environments. Many logistics operators are transitioning toward electrically powered bicycles to support delivery operations across congested urban areas. Electric bicycles offer several operational advantages, including lower emissions, reduced operating costs, and improved maneuverability in busy city streets compared to traditional delivery vehicles. Their ability to navigate narrow routes and reach destinations quickly makes them particularly suitable for urban distribution networks.

The Class 1 segment accounted for 61% share in 2025 and is projected to grow at a CAGR of 6.5% between 2026 and 2035. The popularity of this category is largely linked to increasing consumer preference for electric bicycles that comply with regulatory standards while maintaining safe and predictable riding performance. These pedal-assist bicycles operate within defined speed limitations and do not rely on throttle-based acceleration, allowing them to meet regional cycling regulations. Due to these characteristics, riders can easily utilize them within established cycling infrastructure across many European cities. Expanding networks of dedicated cycling routes, safe storage areas, and improved urban cycling connectivity are encouraging more commuters to adopt pedal-assist e-bikes for daily travel. As urban infrastructure continues to prioritize cycling accessibility, Class 1 e-bikes are expected to remain a dominant product category within the Europe e-bike market.

The lithium-ion batteries segment accounted for 78% share in 2025 and is expected to grow at a CAGR of 7.5% from 2026 to 2035. Lithium-ion battery systems are widely favored because they provide high energy density while maintaining relatively lightweight performance characteristics. These batteries enable longer riding distances, shorter charging times, and improved overall vehicle efficiency when compared with older battery technologies. As a result, both manufacturers and consumers increasingly prefer lithium-ion solutions for electric bicycles. Continuous technological advancements in battery management systems, cell architecture, and energy optimization are further improving the performance and reliability of electric bikes. These innovations support longer battery life cycles and improved operational stability, strengthening the role of lithium-ion technology as the dominant power source across the Europe e-bike market.

Germany E-Bike Market held 52% share, generating USD 5 billion in 2025. The country recorded about 1.4 million new e-bike registrations during the same year, reinforcing its position as one of the most influential markets in the region. Strong consumer purchasing power, well-developed cycling infrastructure, and supportive mobility initiatives have contributed significantly to rising demand. High sales volumes are encouraging manufacturers and retailers to broaden their product offerings, strengthen distribution networks, and invest in advanced electric bicycle technologies. A deeply established cycling culture combined with extensive infrastructure supporting bicycle transportation continues to accelerate the adoption of electric bicycles across the country. Wide networks of cycling paths, secure parking facilities, and well-integrated transportation planning have made cycling a convenient and widely accepted mode of transportation, further strengthening the demand for e-bikes in Germany.

Major companies operating in the Europe E-Bike Market include Accell, Baltik Vairas, Brompton, CUBE, Giant Bicycles, KTM, Pon, Rad Power Bikes, Trek Bicycle, and Yamaha. Companies competing in the Europe E-Bike Market are implementing several strategies to reinforce their market presence and expand their competitive positioning. Manufacturers are prioritizing technological innovation by improving battery efficiency, motor performance, and smart connectivity features in their electric bicycles. Many companies are also investing in expanding production capacity and strengthening regional supply chains to meet rising demand across European markets. Partnerships with mobility providers, retailers, and urban transport networks are helping companies improve distribution reach and accessibility for consumers. In addition, firms are introducing diverse product portfolios tailored to commuting, leisure, and commercial mobility applications. Enhanced after-sales services, digital retail platforms, and customer experience initiatives are also being adopted to strengthen brand loyalty and establish long-term market leadership within the rapidly growing Europe e-bike market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Class

- 2.2.3 Battery

- 2.2.4 Motor

- 2.2.5 Propulsion

- 2.2.6 Ownership

- 2.2.7 Power Output

- 2.2.8 Application

- 2.2.9 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Government incentives and urban mobility policies

- 3.2.1.2 Rising demand for sustainable transport

- 3.2.1.3 Expansion of cycling infrastructure

- 3.2.1.4 Growth in urban commuting and last-mile mobility

- 3.2.1.5 Technological advancements in e-bike components

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial purchase cost

- 3.2.2.2 Battery safety and recycling concerns

- 3.2.2.3 Supply chain disruptions

- 3.2.2.4 Regulatory variations across countries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of cargo and utility e-bikes

- 3.2.3.2 Growth of e-bike leasing and sharing services

- 3.2.3.3 Integration of smart technologies

- 3.2.3.4 Rising popularity of e-bike tourism

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Western

- 3.4.1.1 EU regulation on type approval for two- or three-wheel vehicles and quadricycles (Regulation (EU) No 168/2013)

- 3.4.1.2 EN 15194 standard for electrically power assisted cycles (EPAC)

- 3.4.1.3 CE marking and conformity assessment requirements

- 3.4.1.4 Battery directive and waste electrical and electronic equipment (WEEE) directive

- 3.4.1.5 National cycling and road safety regulations

- 3.4.2 Eastern

- 3.4.2.1 EU EPAC standard EN 15194 compliance requirements

- 3.4.2.2 CE certification and product safety compliance rules

- 3.4.2.3 National road traffic acts governing e-bike classification and usage

- 3.4.2.4 Battery recycling and environmental compliance regulations

- 3.4.2.5 Local vehicle registration and speed limit regulations for electric bicycles

- 3.4.3 Northern

- 3.4.3.1 EU regulation on electric bicycle classification and safety standards

- 3.4.3.2 EN 15194 technical requirements for electric pedal assisted cycles

- 3.4.3.3 National transport authority guidelines for e-bike road usage

- 3.4.3.4 Environmental and battery recycling regulations

- 3.4.3.5 Urban mobility and cycling infrastructure policy frameworks

- 3.4.4 Southern

- 3.4.4.1 EU EPAC compliance and CE marking requirements

- 3.4.4.2 National road transport regulations for pedal assisted electric bicycles

- 3.4.4.3 Safety standards for electric bicycle components and battery systems

- 3.4.4.4 Environmental directives for battery disposal and recycling

- 3.4.4.5 Municipal mobility regulations promoting cycling and e-bike adoption

- 3.4.1 Western

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price analysis (Driven by Primary Research)

- 3.10.1 Historical Price Trend Analysis

- 3.10.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.11 Trade data analysis (Driven by Paid Research)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis (Driven by Primary Research)

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Impact of AI & generative AI on the market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Capacity & production landscape (Driven by Primary Research)

- 3.16.1 Installed capacity by region & key producer

- 3.16.2 Capacity utilization rates & expansion pipelines

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Western

- 4.2.2 Eastern

- 4.2.3 Northern

- 4.2.4 Southern

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Class, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Class 1

- 5.3 Class 2

- 5.4 Class 3

Chapter 6 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Lead-acid

- 6.3 Lithium-ion

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Motor, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Hub motor

- 7.3 Mid motor

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Pedal assist

- 8.3 Throttle control

Chapter 9 Market Estimates & Forecast, By Ownership, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Shared

- 9.3 Personal

Chapter 10 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 Below 250W

- 10.3 250W to 750W

- 10.4 Above 750W

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 City/Urban

- 11.3 Trekking

- 11.4 Cargo

- 11.5 Mountain/Off-Road

- 11.6 Others

Chapter 12 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 Online

- 12.3 Offline

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 13.1 Key trends

- 13.2 Western Europe

- 13.2.1 Germany

- 13.2.2 Austria

- 13.2.3 France

- 13.2.4 Switzerland

- 13.2.5 Belgium

- 13.2.6 Luxembourg

- 13.2.7 Netherlands

- 13.2.8 Portugal

- 13.3 Eastern Europe

- 13.3.1 Poland

- 13.3.2 Romania

- 13.3.3 Czech Republic

- 13.3.4 Slovenia

- 13.3.5 Hungary

- 13.3.6 Bulgaria

- 13.4 Northern Europe

- 13.4.1 UK

- 13.4.2 Denmark

- 13.4.3 Sweden

- 13.4.4 Finland

- 13.4.5 Norway

- 13.5 Southern Europe

- 13.5.1 Italy

- 13.5.2 Spain

- 13.5.3 Greece

Chapter 14 Company Profiles

- 14.1 Global Players

- 14.1.1 Accell

- 14.1.2 Bianchi

- 14.1.3 Giant Bicycles

- 14.1.4 Pon

- 14.1.5 Trek Bicycle

- 14.1.6 Yamaha

- 14.2 Regional Players

- 14.2.1 Baltik Vairas

- 14.2.2 BH Bikes

- 14.2.3 Brompton

- 14.2.4 CUBE

- 14.2.5 Haibike

- 14.2.6 Himiway

- 14.2.7 KTM

- 14.2.8 Moustache Bikes

- 14.2.9 Pedego

- 14.2.10 Riese & Muller

- 14.3 Emerging Players

- 14.3.1 ENGWE

- 14.3.2 Gocycle

- 14.3.3 Himiway

- 14.3.4 Rad Power Bikes

- 14.3.5 VanMoof