PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998731

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998731

Marine Propulsion Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

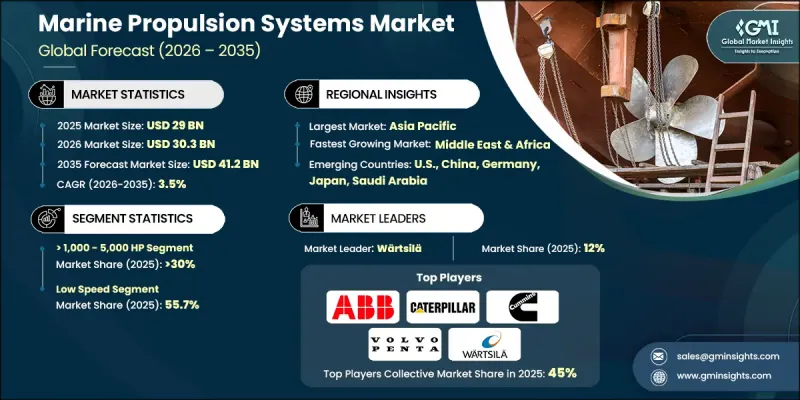

The Global Marine Propulsion Systems Market was valued at USD 29 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 41.2 billion by 2035.

Growth in the marine propulsion systems market is closely connected to increasing global maritime trade and the continued modernization of vessel technologies. As shipping volumes expand worldwide, vessel operators are seeking propulsion solutions capable of delivering reliable performance while handling heavier operational loads. At the same time, manufacturers are prioritizing the development of propulsion technologies that improve fuel efficiency, reduce operational expenses, and minimize environmental impact. Marine propulsion systems represent the core mechanical framework that enables vessels to move through water by converting generated power into thrust. These systems combine multiple elements, including power generation equipment, transmission components, and propulsive devices that work together as a unified operational system. Modern propulsion architectures incorporate both traditional power generation technologies and advanced hybrid or electric configurations designed to maintain performance across diverse marine conditions. Increasing integration of digital control platforms is also transforming system efficiency, allowing operators to monitor performance data and maintain stable propulsion output. Advanced diagnostic systems continuously track operational parameters, helping ensure reliability while minimizing unexpected maintenance interruptions. Improvements in hydrodynamic engineering have further enhanced propulsor performance, enabling smoother maneuverability and optimized energy efficiency during vessel operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $29 Billion |

| Forecast Value | $41.2 Billion |

| CAGR | 3.5% |

The >1,000-5,000 HP segment within the marine propulsion systems market accounted for 30% share in 2025 and is projected to grow at a CAGR of 3.5% from 2026 to 2035. Propulsion systems within this horsepower category support a wide range of commercial maritime activities due to their strong balance of power output and operational efficiency. These engines are widely valued for their ability to handle substantial operational loads while maintaining dependable performance during extended marine operations. Their durability, consistent torque generation, and compatibility with widely available fuel options contribute to their widespread use across numerous vessel categories. These performance characteristics continue to reinforce the importance of this horsepower range within the broader propulsion systems industry.

The low-speed marine propulsion systems market represented 55.7% share in 2025 and is expected to reach USD 20 billion by 2035. Demand for low-speed propulsion platforms is increasing as vessel operators prioritize operational stability and improved engine efficiency during long-distance marine operations. The integration of advanced engine management technologies is enabling more precise control over engine performance, helping maintain balanced thermal behavior and smoother mechanical operation. These systems are designed to deliver stable torque output at lower rotational speeds, which supports extended service intervals and reliable long-range maritime operations. Continued fleet modernization initiatives and the growing adoption of cleaner fuel solutions are also contributing to increased demand for these propulsion systems, as they can be efficiently integrated with energy-saving technologies and alternative fuel pathways.

U.S. Marine Propulsion Systems Market accounted for 65% share in 2025 and generated USD 2.8 billion. Market growth in the United States is supported by expanding maritime logistics activity and continued investment in domestic shipbuilding programs. Increased modernization of commercial vessel fleets is also contributing to higher demand for advanced propulsion technologies that meet evolving regulatory requirements while delivering improved operational efficiency. Additionally, upgrades across inland and coastal maritime fleets are encouraging the adoption of propulsion systems specifically engineered to meet domestic maritime operational needs.

Major companies operating in the Global Marine Propulsion Systems Market include Wartsila, Caterpillar, Cummins, Rolls-Royce, Hyundai Heavy Industries, Mitsubishi Heavy Industries, Kawasaki Heavy Industries, ABB, AB Volvo Penta, Scania, Yamaha Motor, Weichai, YANMAR Marine International, IHI Power Systems, MITSUI E&S Co., DEUTZ AG, Deere & Company, Anglo Belgian Corporation, Everllence, and Daihatsu Infinearth MFG. Companies competing in the Marine Propulsion Systems Market are strengthening their industry position through technological innovation, strategic partnerships, and expanded manufacturing capabilities. Many manufacturers are investing heavily in research and development to create propulsion solutions that improve energy efficiency, reduce emissions, and support alternative fuel compatibility. Firms are also integrating advanced digital monitoring systems that allow real-time performance tracking and predictive maintenance. Strategic collaborations with shipbuilders and maritime operators enable companies to develop propulsion technologies tailored to evolving vessel requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Power trends

- 2.1.4 Technology trends

- 2.1.5 Propulsion trends

- 2.1.6 Application trends

- 2.1.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of marine propulsion systems

- 3.8 Emerging propulsion technologies & opportunities

- 3.9 Smart Propulsion Technologies & IoT-Enabled Monitoring

- 3.10 Investment landscape & growth prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Wind & solar

- 5.4 Gas turbine

- 5.5 Fuel cell

- 5.6 Steam turbine

- 5.7 Natural gas

- 5.8 Hybrid

- 5.9 Others

Chapter 6 Market Size and Forecast, By Power, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 ≤ 1,000 HP

- 6.3 > 1,000 - 5,000 HP

- 6.4 > 5,000 - 10,000 HP

- 6.5 > 10,000 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 Medium speed

- 7.4 High speed

Chapter 8 Market Size and Forecast, By Propulsion, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 2-stroke

- 8.3 4-stroke

Chapter 9 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Merchant

- 9.2.1 Container vessels

- 9.2.2 Tankers

- 9.2.3 Bulk carriers

- 9.2.4 RO-RO

- 9.2.5 Others

- 9.3 Offshore

- 9.3.1 Drilling rigs & ships

- 9.3.2 Anchor handling vessels

- 9.3.3 Offshore support vessels

- 9.3.4 Floating production units

- 9.3.5 Platform supply vessels

- 9.4 Cruise & ferry

- 9.4.1 Cruise vessels

- 9.4.2 Passenger vessels

- 9.4.3 Passenger/cargo vessels

- 9.4.4 Others

- 9.5 Navy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 Norway

- 10.3.5 France

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.3.8 Netherlands

- 10.3.9 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.4.7 Singapore

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Angola

- 10.5.5 Egypt

- 10.5.6 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 AB Volvo Penta

- 11.2 ABB

- 11.3 Anglo Belgian Corporation

- 11.4 Caterpillar

- 11.5 Cummins

- 11.6 DAIHATSU INFINEARTH MFG.

- 11.7 Deere & Company

- 11.8 DEUTZ AG

- 11.9 Everllence

- 11.10 Hyundai Heavy Industries

- 11.11 IHI Power Systems

- 11.12 Kawasaki Heavy Industries

- 11.13 Mitsubishi Heavy Industries

- 11.14 MITSUI E&S Co.

- 11.15 Rolls-Royce

- 11.16 Scania

- 11.17 Wartsila

- 11.18 Weichai

- 11.19 Yamaha Motor

- 11.20 YANMAR Marine International