PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998741

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998741

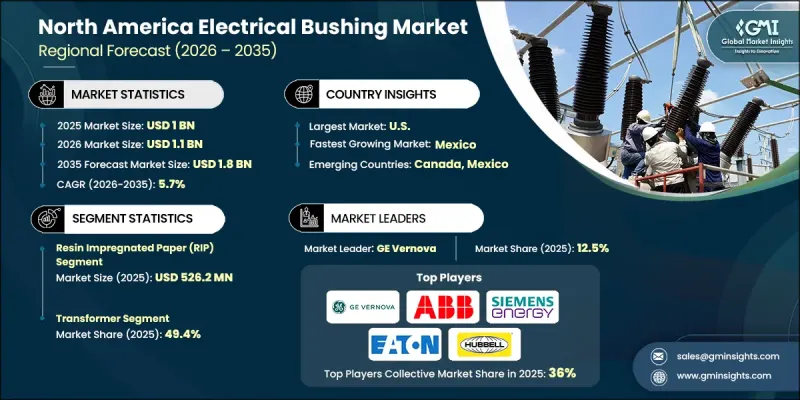

North America Electrical Bushing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Electrical Bushing Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 1.8 billion by 2035.

Utilities across North America are undergoing a multi-year grid modernization effort, emphasizing new transmission corridors, reconductoring, and station upgrades. This focus is driving the demand for transformers, reactors, and switchgear, where bushings serve as critical insulation interfaces for current transfer. Policy-driven funding and facilitation mechanisms are accelerating large-scale projects, reducing financing hurdles, and improving procurement clarity for long-lead components. Capital allocation has shifted toward transmission and distribution upgrades, sustaining bushing consumption in transformers, breakers, and bus interfaces. Aging infrastructure, urban load growth, and integration of intermittent energy sources require equipment replacements and capacity expansion. Compact, high-performance bushing designs that meet stricter insulation and thermal criteria are increasingly preferred, supporting substation resilience and enhanced transfer capabilities. Regional planning reforms and coordinated policies are aligning utilities and ISOs on transparent, long-term build plans, reinforcing steady market demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $1.8 Billion |

| CAGR | 5.7% |

The transformers segment held 49.4% share in 2025 and is expected to grow at a CAGR of 4.5% through 2035. Bushings are used in generator step-up units, autotransformers, shunt reactors, and distribution transformers across utilities and industrial plants. Condenser-graded designs (OIP/RIP) provide high dielectric strength, impulse performance, and current-carrying capacity for oil-to-air, oil-to-oil, and oil-to-SF connections. As utilities upgrade aging lines, rebuild substations, and enhance capacity, transformer bushing demand remains consistent, with specifications emphasizing partial discharge control, creepage distance, and seismic performance.

The lithium-ion segment held a 62.9% share in 2025, driven by increasing demand for reliable energy storage, fast response, and efficient peak shaving. Its widespread adoption is fueled by superior energy density, long cycle life, and high round-trip efficiency compared with alternative storage technologies. Lithium-ion batteries enable hybrid microgrids to provide rapid power dispatch during peak loads or grid interruptions, ensuring stable and continuous electricity for commercial, industrial, and institutional applications. Additionally, the scalability and modularity of lithium-ion systems allow integration with renewable energy sources such as solar and wind, supporting flexible energy management and reducing dependency on conventional grid power.

U.S Electrical Bushing Market held a 67% share, generating USD 694.7 million in 2025. U.S. grid modernization policies, DOE initiatives, and FERC-led interconnection reforms are driving long-distance transmission expansion, substation upgrades, and interregional transfer capabilities, directly stimulating high-voltage bushing demand for transformers, breakers, and wall applications.

Key players in the North America Electrical Bushing Market include ABB, CG Power and Industrial Solutions, Siemens Energy, Hitachi Energy, Eaton, General Electric, Barberi Rubinetterie Industriali S.r.l., Liyond, RHM International, LLC, Trench Group, GIPRO, Nexans, PFISTERER Holding SE, Poinsa, Maschinenfabrik Reinhausen GmbH, Polycast, Meister International, LLC, Elliot Industries, and Hubbell. Companies are strengthening their market position through strategic investments in R&D, focusing on enhanced insulation performance, thermal management, and compact designs for modern substations. Partnerships with utilities and EPC contractors help secure long-term supply contracts and project collaborations. Firms are expanding regional manufacturing and service networks to reduce lead times and improve customer support. Integration of digital monitoring technologies and predictive maintenance solutions enhances reliability and product differentiation. Active participation in standardization committees and regulatory initiatives allows companies to influence technical requirements while ensuring compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Bushing type trends

- 2.1.3 Insulation trends

- 2.1.4 Voltage trends

- 2.1.5 Application trends

- 2.1.6 End use trends

- 2.1.7 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.8 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Oil impregnated paper (OIP)

- 5.2.1 Mineral-based

- 5.2.2 Silicon-based

- 5.2.3 Others

- 5.3 Resin impregnated paper (RIP)

- 5.4 Others

Chapter 6 Market Size and Forecast, By Insulation, 2022 - 2035 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Porcelain

- 6.3 Polymeric

- 6.4 Glass

Chapter 7 Market Size and Forecast, By Voltage, 2022 - 2035 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Medium Voltage

- 7.3 High Voltage

- 7.4 Extra High Voltage

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 Transformer

- 8.3 Switchgear

- 8.4 Others

Chapter 9 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & '000 Units)

- 9.1 Key trends

- 9.2 Industries

- 9.3 Utility

- 9.4 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

- 10.1 Key trends

- 10.2 U.S.

- 10.3 Canada

- 10.4 Mexico

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Barberi Rubinetterie Industriali S.r.l.

- 11.3 CG Power and Industrial Solutions

- 11.4 Eaton

- 11.5 Elliot Industries

- 11.6 General Electric

- 11.7 GIPRO

- 11.8 Hitachi Energy

- 11.9 Hubbell

- 11.10 Liyond

- 11.11 Meister International, LLC

- 11.12 Maschinenfabrik Reinhausen GmbH

- 11.13 Nexans

- 11.14 Polycast

- 11.15 Poinsa

- 11.16 PFISTERER Holding SE

- 11.17 RHM International, LLC

- 11.18 Siemens Energy

- 11.19 Trench Group