PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998763

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998763

Degaussing System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

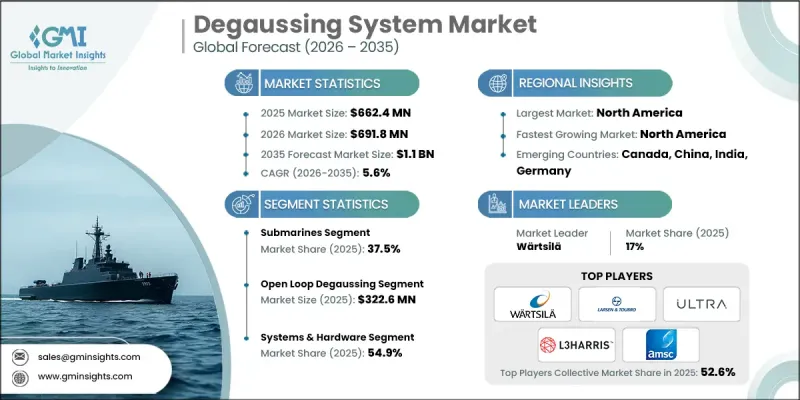

The Global Degaussing System Market was valued at USD 662.4 million in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 1.1 billion in 2035.

The market expansion is driven by growing naval modernization programs, increasing fleet expansions, and the rising need to counter threats from magnetic mines and influence-based underwater weapons. Navies worldwide emphasize vessel stealth and magnetic signature management while integrating advanced digital monitoring technologies to enhance fleet survivability and protection. Geopolitical tensions and maritime security concerns are accelerating the adoption of degaussing systems, while the increasing focus on energy-efficient and low-maintenance technologies reinforce demand. The modernization of warships and mine countermeasure programs has elevated the significance of magnetic signature control systems, particularly in submarines and advanced combat vessels. Rising investment in digital monitoring and operational cost reduction across fleets is expected to sustain market momentum through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $662.4 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 5.6% |

The submarines segment held a 37.5% share in 2025, due to the critical requirement for magnetic signature reduction in stealth operations. Submarines operate in sensitive and hostile underwater environments, making them highly vulnerable to detection and magnetic mines. The continuous deployment of conventional and nuclear-powered submarines by major navies globally ensures consistent demand for advanced degaussing systems designed to maintain operational security and enhance stealth capabilities.

The open-loop degaussing systems segment generated USD 322.6 million in 2025, as they provide reliable magnetic reduction for naval vessels. These systems use predetermined electrical current levels to neutralize permanent and induced magnetism in ships, offering operational efficiency with reduced complexity. Their proven reliability, straightforward integration, and adaptability across a range of naval platforms make them essential for long-term magnetic management and fleet safety.

North America Degaussing System Market held 36.5% share in 2025, driven by continuous naval modernization initiatives. The region benefits from advanced naval fleets and the presence of leading defense contractors specializing in magnetic signature management solutions. Governments are investing heavily in mine countermeasure systems, fleet survivability technologies, and digital vessel monitoring platforms. Continuous upgrades and fleet sustainment programs are expected to maintain North America as a key contributor to degaussing system adoption through 2035, underpinned by strong defense budgets and technological advancements.

Leading companies operating in the Global Degaussing System Market include Ultra Electronics Holdings Plc, Polyamp, American Superconductor Corporation, Larsen & Toubro Limited, HAELOG, Hitzinger GmbH, L3Harris Technologies Inc., DA-Group, Dayatech Merin, STL Systems AG, K&G Marine, Surma Ltd., Wartsila, IFEN, and Magnetics International. Key players in the Global Degaussing System Market are employing strategies to strengthen their foothold and expand their market presence. Companies are investing in R&D to develop energy-efficient, low-maintenance, and digitally integrated degaussing solutions suitable for modern naval fleets. Strategic partnerships with defense contractors, governments, and shipbuilding companies enhance technology adoption and global reach. Firms are also focusing on modular and scalable systems to address different vessel classes, including submarines and surface combatants. Expanding into emerging maritime markets and offering maintenance, training, and lifecycle support services further improves customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vessel type trends

- 2.2.2 System type trends

- 2.2.3 Offering trends

- 2.2.4 Installation type trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising naval modernization and fleet expansion programs

- 3.2.1.2 Growing threats from magnetic mines/torpedoes

- 3.2.1.3 Increased focus on vessel stealth and survivability

- 3.2.1.4 Technological advances in degaussing automation

- 3.2.1.5 Data center and secure data destruction requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited impact on solid-state storage devices

- 3.2.2.2 Competition from alternative suppression technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with unmanned vessel platforms

- 3.2.3.2 Integration with digital monitoring/IoT systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vessel Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Surface combatants

- 5.2.1 Frigates

- 5.2.2 Destroyers

- 5.2.3 Corvettes

- 5.2.4 Cruisers

- 5.3 Aircraft carriers & amphibious vessels

- 5.3.1 Landing helicopter dock (LHD)

- 5.3.2 Landing platform dock (LPD)

- 5.3.3 Landing ship tank (LST)

- 5.4 Submarines

- 5.4.1 Attack submarines

- 5.4.2 Ballistic missile submarines

- 5.4.3 Cruise missile submarines

- 5.5 Patrol & support vessels

- 5.5.1 Offshore patrol vessels (OPV)

- 5.5.2 Mine countermeasure vessels (MCMV)

- 5.5.3 Fast attack craft (FAC)

- 5.5.4 Auxiliary & support ships

Chapter 6 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Open loop degaussing

- 6.2.1 Gyro / geomagnetic map control

- 6.2.2 Manual mode systems

- 6.2.3 Legacy fleet systems

- 6.3 Closed loop degaussing

- 6.3.1 Magnetometer-based control

- 6.3.2 Signature prediction systems

- 6.3.3 Reduced range dependency systems

- 6.4 Hybrid systems

- 6.4.1 Multi-mode systems

- 6.4.2 Upgrade-ready platforms

- 6.4.3 Modular systems

Chapter 7 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Systems & hardware

- 7.2.1 Degaussing coil assemblies

- 7.2.2 Power supply units

- 7.2.3 Control cabinets

- 7.2.4 Magnetometers & sensors

- 7.2.5 Bipolar amplifiers & conductors

- 7.2.6 Embedded control software

- 7.3 Services

- 7.3.1 Installation & commissioning

- 7.3.2 Preventive maintenance

- 7.3.3 Repairs & troubleshooting

- 7.3.4 System modernization

- 7.3.5 Calibration & verification

- 7.3.6 Technical support & training

Chapter 8 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 New build (OEM integration)

- 8.3 Retrofit / modernization

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Wartsila

- 10.1.2 L3Harris Technologies Inc.

- 10.1.3 Larsen & Toubro Limited

- 10.1.4 Ultra Electronics Holdings Plc

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 American Superconductor Corporation

- 10.2.1.2 Magnetics International

- 10.2.2 Asia Pacific

- 10.2.2.1 Surma Ltd.

- 10.2.2.2 Dayatech Merin

- 10.2.3 Europe

- 10.2.3.1 Polyamp

- 10.2.3.2 Hitzinger GmbH

- 10.2.3.3 STL Systems AG

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 IFEN

- 10.3.2 K&G Marine

- 10.3.3 Meriton Industries

- 10.3.4 DA-Group

- 10.3.5 HAELOG