PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998771

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998771

Middle East and Africa Subsea Flowlines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

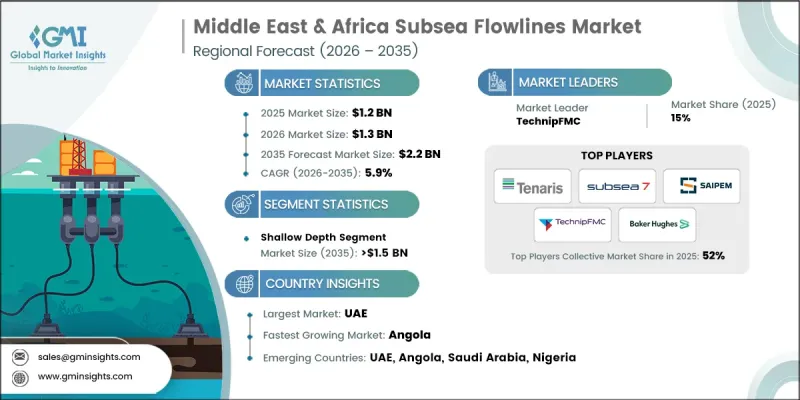

Middle East & Africa Subsea Flowlines Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 2.2 billion by 2035.

The market expansion is driven by increasing investments in deepwater and ultradeep water oil and gas exploration, fueled by rising energy demand and the growing deployment of floating production systems. Offshore operations in challenging environments across key countries, including UAE, Angola, and Nigeria, are accelerating the development of advanced subsea infrastructure. Operators are seeking efficient and reliable systems to transport hydrocarbons from offshore wells to processing facilities, supporting the need for sophisticated subsea flowline networks. Investments in maintaining existing offshore assets and expanding hydrocarbon production across various water depths further bolster market growth. The push toward deep offshore field development, coupled with changing exploration dynamics, continues to enhance the adoption of subsea flowlines across the region.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.9% |

The shallow depth segment is anticipated to generate USD 1.5 billion by 2035. Growth in this segment is supported by rising offshore oil and gas projects and the implementation of advanced recovery techniques. Increasing automation, digitalization, and the strategic allocation of substantial budgets by regional operators are driving the adoption of shallow-water subsea flowline systems. These developments allow operators to improve efficiency and performance while ensuring reliable transport of oil and gas from nearshore fields.

UAE Subsea Flowlines Market is expected to reach USD 469.5 million by 2035. The presence of significant offshore oil and gas reserves, coupled with ongoing exploration and production activities, is boosting demand. A strategic focus on energy conservation and growing investments in unconventional resource development and newly discovered crude reserves are further shaping the regional market, enhancing opportunities for subsea flowline deployment.

Major players operating in the Middle East & Africa Subsea Flowlines Industry include Baker Hughes, McDermott, NOV, Saipem, Subsea7, TechnipFMC, Halliburton, John Wood Group, Alleima, ArcelorMittal Energy Projects, Butting Group, Cactus Wellhead, EnerMech, Maillefer, Marubeni-Itochu Tubulars, Prysmian Group, Syensqo, Tenaris, Tubacex, and Vallourec. Key strategies adopted by companies in the Middle East & Africa Subsea Flowlines Market include investing in R&D to enhance pipe materials, coatings, and jointing technologies for deepwater applications. Firms are forging strategic partnerships with regional operators to secure long-term contracts for offshore projects. Focusing on digitalization, automation, and predictive maintenance solutions helps improve operational efficiency and service reliability. Expanding manufacturing facilities locally reduces lead times and supports the rapid deployment of flowline systems. Companies are also prioritizing sustainability by developing eco-friendly and corrosion-resistant materials to comply with regulatory standards, enhancing their competitive positioning across challenging offshore markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by country

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Water depth trends

- 2.4 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Price trend analysis (USD/feet)

- 3.7.1 By water depth

- 3.7.2 By country

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 Angola

- 4.2.2 Nigeria

- 4.2.3 Egypt

- 4.2.4 Qatar

- 4.2.5 Saudi Arabia

- 4.2.6 UAE

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Water Depth, 2022 - 2035, (USD Million and '000 Feet)

- 5.1 Key trends

- 5.2 Shallow

- 5.3 Deep

- 5.4 Ultra Deep

Chapter 6 Market Size and Forecast, By Country, 2022 - 2035, (USD Million and '000 Feet)

- 6.1 Key trends

- 6.2 Angola

- 6.3 Nigeria

- 6.4 Egypt

- 6.5 Qatar

- 6.6 Saudi Arabia

- 6.7 UAE

Chapter 7 Company Profiles

- 7.1 Alleima

- 7.2 ArcelorMittal Energy Projects

- 7.3 Baker Hughes

- 7.4 Butting Group

- 7.5 Cactus Wellhead

- 7.6 EnerMech

- 7.7 Halliburton

- 7.8 John Wood Group

- 7.9 Maillefer

- 7.10 Marubeni-Itochu Tubulars

- 7.11 McDermott

- 7.12 NOV

- 7.13 Prysmian Group

- 7.14 Saipem

- 7.15 Subsea7

- 7.16 Syensqo

- 7.17 TechnipFMC

- 7.18 Tenaris

- 7.19 Tubacex

- 7.20 Vallourec