PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998783

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998783

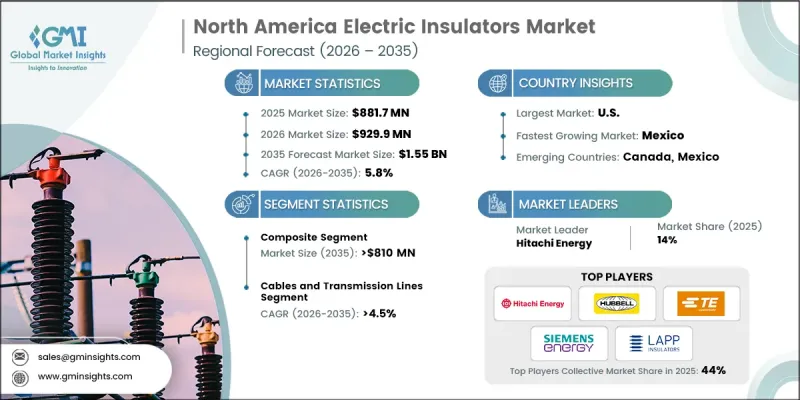

North America Electric Insulators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Electric Insulators Market was valued at USD 881.7 million in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 1.55 billion by 2035.

The growth of the sector is fueled by rising electricity demand, initiatives to modernize transmission and distribution grids, and efforts by utilities and authorities to ensure reliable power delivery while minimizing outages. Government investments aimed at enhancing grid infrastructure, combined with increasing capital expenditures on medium- and high-voltage insulator systems, are driving market expansion. Ongoing replacement of traditional insulators, refurbishment of aging networks, and the adoption of higher-performance solutions in critical infrastructure further reinforce demand. Extreme weather events have also underscored the need for resilient electrical infrastructure, prompting utilities to invest in certified, high-quality insulators. The market is positioned for steady growth as operators prioritize reliability, resilience, and adoption of advanced materials across transmission and distribution networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $881.7 Million |

| Forecast Value | $1.55 Billion |

| CAGR | 5.8% |

The composite insulator segment is expected to reach USD 810 million by 2035. Rising adoption of advanced insulator materials, along with continuous modernization of transmission networks, supports the expansion of composite insulators. These materials provide improved durability, environmental resistance, and performance under high-voltage conditions, making them increasingly preferred for new installations and replacement projects. Investments in high-voltage infrastructure refurbishment are accelerating the deployment of composite solutions, reflecting the shift toward reliable, long-lasting, and high-performance electrical components.

The cables and transmission lines segment is projected to grow at a CAGR of 4.5% through 2035. Increasing electricity demand, supportive government initiatives, and the need for high-capacity transmission lines are driving adoption. These systems help prevent leakage currents, enhance line efficiency, and resist environmental stresses, supporting uninterrupted electricity delivery. Modernization of aging grids and the development of advanced transmission networks further stimulate market growth.

U.S. Electric Insulators Market held a 71.8% share in 2025, generating USD 632.7 million. Expansion of power generation capacity, rising electricity consumption, and favorable policies for grid development are supporting market growth. Investments in upgrading existing infrastructure, along with the deployment of electricity networks in remote regions, are reinforcing industry momentum and creating demand for reliable, high-quality insulator products.

Prominent players operating in the North America Electric Insulators Industry include Elsewedy Electric, Dow, Gamma Insulators, Victor Insulator, TE Connectivity, Asasoft, Sediver, Lapp Insulators US, Ensto, Siemens Energy, K-Line Insulators, PPC Austria, Polycast, Multico, Comptec, Pfisterer, Global Insulator Group, Maschinenfabrik Reinhausen, Hitachi Energy, Hubbell, and Power Grid Components. Companies in the North America Electric Insulators Market are adopting multiple strategies to strengthen their market position. Key approaches include expanding manufacturing facilities and regional distribution networks to ensure timely supply, investing in R&D to develop high-performance, weather-resistant, and energy-efficient products, and forming partnerships with utilities, grid operators, and infrastructure developers for long-term contracts. Firms are also focusing on regulatory compliance, product certification, and quality assurance to meet stringent grid standards. Mergers and acquisitions, technology licensing, and collaborations with material science innovators help enhance portfolio diversity, improve cost efficiencies, and reinforce brand credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by country

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Material trends

- 2.4 Voltage trends

- 2.5 Application trends

- 2.6 Product trends

- 2.7 End-Use trends

- 2.8 Rating trends

- 2.9 Installation trends

- 2.10 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of electric insulators

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Material, 2022 - 2035, (USD Million)

- 5.1 Key trends

- 5.2 Ceramic/porcelain

- 5.3 Glass

- 5.4 Composite

Chapter 6 Market Size and Forecast, By Voltage, 2022 - 2035, (USD Million)

- 6.1 Key trends

- 6.2 High Voltage

- 6.3 Medium Voltage

- 6.4 Low Voltage

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035, (USD Million)

- 7.1 Key trends

- 7.2 Cables and transmission lines

- 7.3 Switchgears

- 7.4 Transformer

- 7.5 Bus Bars

- 7.6 Others

Chapter 8 Market Size and Forecast, By Product, 2022 - 2035, (USD Million)

- 8.1 Key trends

- 8.2 Pin insulators

- 8.3 Suspension insulators

- 8.4 Shackle insulators

- 8.5 Other insulators

Chapter 9 Market Size and Forecast, By End-Use, 2022 - 2035, (USD Million)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & industrial

- 9.4 Utilities

Chapter 10 Market Size and Forecast, By Rating, 2022 - 2035, (USD Million)

- 10.1 Key trends

- 10.2 ≤ 11 kV

- 10.3 > 11 kV to ≤ 22 kV

- 10.4 > 22 kV to ≤ 33 kV

- 10.5 > 33 kV to ≤ 72.5 kV

- 10.6 > 72.5 kV to ≤ 145 kV

- 10.7 > 145 kV to ≤ 220 kV

- 10.8 > 220 kV to ≤ 400 kV

- 10.9 > 400 kV to ≤ 800 kV

- 10.10 > 800 kV to ≤ 1,200 kV

- 10.11 > 1,200 kV

Chapter 11 Market Size and Forecast, By Installation, 2022 - 2035, (USD Million)

- 11.1 Key trends

- 11.2 Distribution

- 11.3 Transmission

- 11.4 Substation

- 11.5 Railways

- 11.6 Others

Chapter 12 Market Size and Forecast, By Country, 2022 - 2035, (USD Million)

- 12.1 Key trends

- 12.2 U.S.

- 12.3 Canada

- 12.4 Mexico

Chapter 13 Company Profiles

- 13.1 Asasoft

- 13.2 Comptec

- 13.3 Dow

- 13.4 Elsewedy Electric

- 13.5 Ensto

- 13.6 Gamma Insulators

- 13.7 Global Insulator Group

- 13.8 Hitachi Energy

- 13.9 Hubbell

- 13.10 K-Line Insulators

- 13.11 Lapp Insulators US

- 13.12 Maschinenfabrik Reinhausen

- 13.13 Multico

- 13.14 NGK Insulators

- 13.15 Pfisterer

- 13.16 Polycast

- 13.17 Power Grid Components

- 13.18 PPC Austria

- 13.19 Sediver

- 13.20 Siemens Energy

- 13.21 TE Connectivity

- 13.22 Victor Insulator