PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998787

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998787

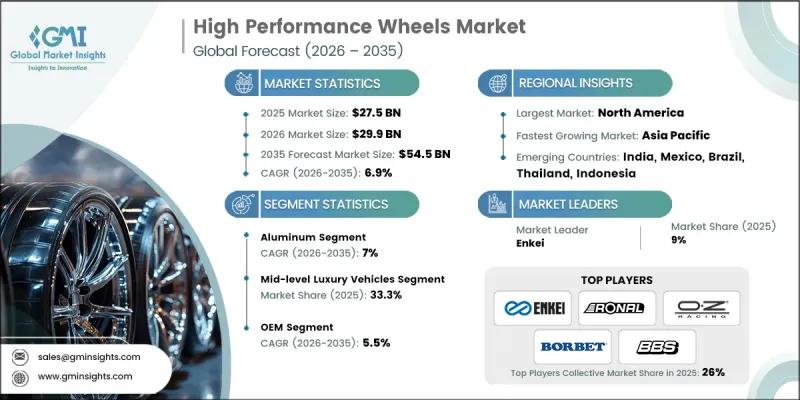

High Performance Wheels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global High Performance Wheels Market was valued at USD 27.5 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 54.5 billion by 2035.

Growth in the high performance wheels industry is strongly influenced by increasing demand for lightweight automotive components that improve efficiency and driving dynamics. Automotive manufacturers are widely adopting advanced materials such as forged aluminum and carbon fiber to reduce vehicle weight, enhance durability, and support improved fuel efficiency. Lightweight wheel technologies also play a crucial role in reducing emissions and improving vehicle performance across modern automotive platforms. In addition, the rising adoption of electric vehicles is accelerating the demand for aerodynamic and energy-efficient wheel designs that reduce rolling resistance and extend battery range. Premium and performance vehicle manufacturers are increasingly equipping their models with larger-diameter alloy and forged wheels to enhance handling, braking performance, and overall aesthetics. Growing interest in motorsports, performance upgrades, and customization culture is also fueling strong demand in the aftermarket segment. These factors collectively continue to drive innovation in wheel design, materials engineering, and manufacturing technologies across the global automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.5 Billion |

| Forecast Value | $54.5 Billion |

| CAGR | 6.9% |

The aluminum wheels segment held a 60% share in 2025 and is expected to grow at a CAGR of 7% between 2026 and 2035. Aluminum alloys remain the preferred material because they provide an optimal balance between strength, lightweight construction, corrosion resistance, and manufacturing cost. The increasing integration of aluminum wheels in original equipment manufacturing, particularly in electric vehicles and premium passenger vehicles, is further strengthening segment growth. Advanced manufacturing techniques such as flow-forming and forging enable manufacturers to produce lightweight wheels that deliver improved structural rigidity and enhanced driving stability. These technologies also support improved heat dissipation and durability, which are essential for high-performance automotive applications.

The mid-level luxury vehicle segment accounted for 33.3% share in 2025 and is expected to grow at a CAGR of 7.9% from 2026 to 2035. Vehicles within this category are increasingly equipped with performance-oriented wheels that combine aesthetic appeal with improved vehicle dynamics. Automotive manufacturers are introducing optional packages that include lightweight performance wheels designed to enhance acceleration, braking, and road grip. Consumer demand for vehicles that deliver both style and performance continues to grow, encouraging automakers to integrate premium wheel technologies into mid-tier luxury models. The adoption of advanced wheel manufacturing processes also enables brands to offer visually distinctive designs while maintaining cost efficiency and structural strength.

U.S. High Performance Wheels Market reached USD 8.1 billion in 2025. The strong presence of luxury and performance vehicles in the country creates significant opportunities for original equipment manufacturers to integrate advanced wheel technologies. Automotive brands operating in the U.S. market are increasingly focusing on forged and aerodynamically optimized wheel designs to meet rising consumer expectations for performance, ride comfort, and visual appeal. The growing popularity of large-diameter premium wheels, particularly in specialized vehicle segments, is contributing to higher demand for high-value wheel products. In addition, increasing consumer interest in vehicle customization and performance enhancement continues to stimulate the aftermarket segment, supporting overall market expansion.

Key players in the Global High Performance Wheels Market include BBS, Borbet, Carbon Rev, Enkei, HRE, OZ Racing, Rays, Ronal, Vossen, and Work. Companies operating in the Global High Performance Wheels Market focus on innovation in materials engineering and manufacturing processes to strengthen their competitive position. Many manufacturers invest heavily in research and development to create lighter, stronger, and more aerodynamic wheel designs that improve vehicle efficiency and handling. Strategic collaborations with automotive manufacturers allow companies to supply wheels directly to original equipment production lines, strengthening long-term partnerships. Firms also expand their product portfolios through advanced forging technologies and customized design solutions to address the growing demand for premium vehicle personalization. Global expansion strategies, combined with strong distribution networks and aftermarket presence, help companies increase brand visibility and maintain market leadership while meeting evolving automotive performance requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Vehicle

- 2.2.4 Sales channel

- 2.2.5 Distribution channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for lightweight vehicles

- 3.2.1.2 Growth in premium & luxury vehicle sales

- 3.2.1.3 Expansion of motorsports industry

- 3.2.1.4 Aftermarket customization trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs

- 3.2.2.2 Volatility in raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing OEM partnerships

- 3.2.3.2 Growing EV aftermarket segment

- 3.2.3.3 Advancements in hybrid forging techniques

- 3.2.3.4 Emerging automotive markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Whole Vehicle Type Approval (WVTA)

- 3.4.2.2 ECE Regulation 124 (R124)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automotive Standards Organization (JASO)

- 3.4.3.2 AIS (Automotive Industry Standards) - India

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) - Resolution 242

- 3.4.4.2 Mexican NOM Standards (Normas Oficiales Mexicanas)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Cost breakdown analysis

- 3.10 Price analysis (Driven by Primary Research)

- 3.10.1 Historical Price Trend Analysis

- 3.10.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & Generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Quality standards & testing protocols

- 3.15.1 International quality certification standards (ISO, TUV, JWL)

- 3.15.2 Performance testing methodologies

- 3.15.3 Safety & durability requirements

- 3.15.4 Counterfeit product identification & prevention

- 3.16 Consumer behavior & buying patterns analysis

- 3.16.1 Purchase decision drivers

- 3.16.2 Brand loyalty & switching behavior

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Magnesium

- 5.4 Steel

- 5.5 Carbon fiber

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Entry-level performance vehicles

- 6.3 Mid-level luxury vehicles

- 6.4 Top-end luxury vehicles

- 6.5 Supercars & hypercars

- 6.6 Performance SUVs & crossovers

- 6.7 Motorsport & racing

Chapter 7 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Distribution channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Offline channel

- 8.3 Online channel

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 BBS Motorsport

- 10.1.2 Borbet

- 10.1.3 Carbon Revolution

- 10.1.4 Enkei

- 10.1.5 HRE Performance Wheels

- 10.1.6 OZ Racing

- 10.1.7 Rays Engineering / Volk Racing

- 10.1.8 Ronal

- 10.1.9 Vossen

- 10.1.10 Work Wheels

- 10.2 Regional players

- 10.2.1 Advan Racing / Yokohama

- 10.2.2 BC Forged

- 10.2.3 Dymag

- 10.2.4 Forgeline

- 10.2.5 Speedline Corse

- 10.2.6 SSR Wheels

- 10.2.7 TSW Alloy Wheels

- 10.2.8 Weds Sport

- 10.3 Emerging players

- 10.3.1 Cosmis Wheels

- 10.3.2 Fifteen52

- 10.3.3 Rotiform

- 10.3.4 Titan7