PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998813

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998813

Epoxy Active Diluent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

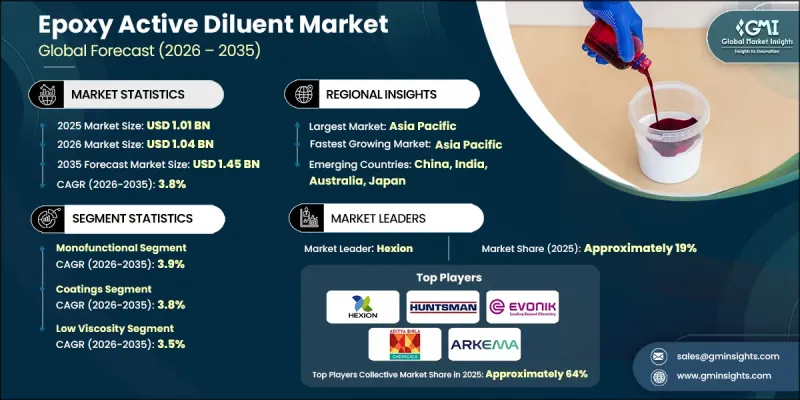

The Global Epoxy Active Diluent Market was valued at USD 1.01 billion in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 1.45 billion by 2035.

Epoxy active diluents are widely used additives designed to reduce the viscosity of epoxy resins, which improves their handling, processing, and application efficiency in industrial environments. These materials play an important role in enhancing the performance of epoxy systems across a range of manufacturing processes. Increasing demand from sectors such as automotive manufacturing, construction materials, and electronic component production continues to support market expansion. Industries rely on epoxy systems for their strong mechanical performance, durability, and chemical resistance, which makes active diluents essential for achieving optimal formulation properties. Demand is also being influenced by the growing need for high-performance surface treatments that provide protection, durability, and long-term structural stability. Another notable trend shaping the market is the shift toward environmentally responsible chemical solutions. Epoxy active diluents are gaining attention because they generate lower volatile organic compound emissions compared with many conventional solvent-based materials, which supports compliance with tightening environmental regulations. In addition, manufacturers are exploring the development of bio-derived diluent technologies to address sustainability goals. Continued innovation in epoxy formulation technology and increasing preference for advanced epoxy-based materials in specialized industrial applications are expected to support stable market growth in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.01 Billion |

| Forecast Value | $1.45 Billion |

| CAGR | 3.8% |

The monofunctional segment reached USD 0.61 billion in 2025. Monofunctional diluents maintain a strong market position due to their versatility and consistent performance across multiple industrial processes. These materials are widely incorporated into epoxy formulations because they help improve curing efficiency, enhance chemical resistance, and strengthen adhesion properties. Their ability to regulate resin viscosity while maintaining stable processing characteristics makes them highly suitable for applications that require controlled formulation behavior. As a result, monofunctional diluents are commonly selected for industrial uses where precision, durability, and reliable performance are essential.

The coatings segment accounted for USD 0.38 billion in 2025 and is expected to grow at a CAGR of 3.8% through 2035. Coatings represent one of the largest application areas for epoxy active diluents because epoxy-based systems provide strong protective and decorative properties. When incorporated into coating formulations, active diluents enhance the workability of epoxy resins while maintaining the durability and performance characteristics required in demanding environments. Industries increasingly depend on epoxy coatings to protect surfaces from corrosion, environmental exposure, and mechanical wear. In addition, epoxy coating technologies are widely utilized to improve surface longevity and maintain structural integrity in various industrial settings, which continues to support steady demand for epoxy active diluents within this application category.

North America Epoxy Active Diluent Market reached USD 0.31 billion in 2025. Regional demand is supported by steady consumption across several industrial sectors that rely on epoxy formulations for protective and structural applications. The market in North America shows a strong preference for low-viscosity diluent grades that are commonly used in floor coatings, bonding materials, and protective surface treatments. Meanwhile, advanced manufacturing sectors continue to drive demand for specialized diluent formulations with different viscosity ranges designed for more complex industrial requirements. Increasing investment in composite manufacturing and industrial renovation projects is also contributing to additional demand for epoxy-based materials across the region.

Key companies participating in the Global Epoxy Active Diluent Market include Evonik, Arkema, Huntsman Corporation, Hexion, and Aditya Birla Chemicals, along with several other industry participants. Companies operating in the epoxy active diluent market are implementing multiple strategic initiatives to strengthen their competitive positioning and expand global market presence. Many organizations are prioritizing research and development activities to create advanced diluent formulations that improve epoxy resin performance while meeting evolving environmental regulations. Manufacturers are also focusing on developing sustainable and bio-based chemical alternatives that align with industry demand for environmentally responsible materials. Strategic collaborations with resin producers, coatings manufacturers, and industrial end users are helping companies strengthen supply chains and expand application opportunities. In addition, businesses are investing in production capacity expansion and improving distribution networks to better serve regional markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Aircraft Platform

- 2.2.4 Component Type

- 2.2.5 Product Type

- 2.2.6 Manufacturing Process

- 2.2.7 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Monofunctional

- 5.3 Difunctional

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Coatings

- 6.2.1 Industrial coatings

- 6.2.2 Marine coatings

- 6.2.3 Protective coatings

- 6.3 Adhesives and sealants

- 6.3.1 Structural adhesives

- 6.3.2 Non-structural adhesives

- 6.4 Composite material

- 6.5 Electrical and electronics

- 6.6 Construction

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Viscosity Grade, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Ultra-Low Viscosity

- 7.3 Low Viscosity

- 7.4 Medium Viscosity

- 7.5 High Viscosity

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Air Products and Chemicals

- 9.2 Hexion

- 9.3 Arkema

- 9.4 Cardolite

- 9.5 Sakamoto Yakuhin Kogyo

- 9.6 Arnette Polymers

- 9.7 Aditya Birla Chemicals

- 9.8 Huntsman Corporation

- 9.9 Dow Chemical Company (Dow, Inc.)

- 9.10 Gabriel Chem (Huntsman Corporation)

- 9.11 King Industries, Inc.

- 9.12 EMS-CHEMIE HOLDING AG, LLC

- 9.13 Brenntag (DB US Holding Corporation)

- 9.14 SACHEM Inc.

- 9.15 Evonik