PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038398

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038398

Reactive Diluents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

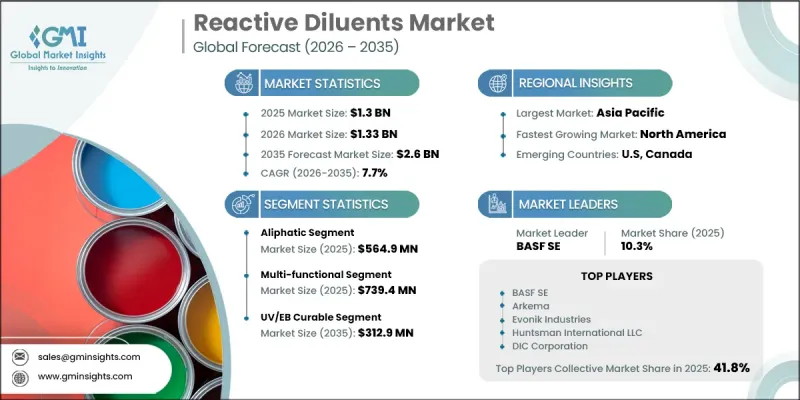

The Global Reactive Diluents Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 2.6 billion by 2035.

The reactive diluents industry continues to expand steadily as these specialty chemicals play a critical role in improving resin formulation efficiency and processing performance. These materials are widely incorporated into resin systems to lower viscosity, enabling easier handling and improved application during manufacturing processes. Unlike conventional additives, reactive diluents chemically integrate into the polymer matrix during curing, becoming a permanent part of the final structure. This functionality allows manufacturers to enhance product performance while optimizing production costs. The materials are commonly utilized across epoxy, polyester, and vinyl ester systems to meet specific processing and end-use requirements. Their ability to modify viscosity without relying on additional solvents contributes to improved adhesion, controlled curing behavior, and consistent output quality. Industries producing coatings, sealants, adhesives, and composite materials rely heavily on these formulations to maintain uniformity and operational efficiency. The market is also witnessing a shift toward customized solutions designed to match precise application needs and resin compatibility, supporting innovation and performance optimization across various industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 7.7% |

The aliphatic segment accounted for USD 564.9 million in 2025, establishing its leading position within the reactive diluents market. This segment is widely preferred due to its ability to provide flexibility, durability, and resistance to environmental exposure, making it suitable for applications that require long-term performance. At the same time, other types continue to serve specialized requirements where enhanced mechanical strength, thermal stability, and faster curing characteristics are necessary. The balance between performance attributes and application-specific functionality continues to shape demand across different product categories, reinforcing the importance of tailored formulations within the industry.

The UV/EB curable segment reached USD 312.9 million in 2025, highlighting its strong presence within the reactive diluents industry. This segment benefits from rapid curing capabilities, energy efficiency, and the ability to deliver high-performance outcomes in demanding applications. Its adoption is driven by the need for faster production cycles and improved process efficiency. Meanwhile, other curing systems remain relevant for applications that require controlled processing conditions and consistent material performance. The role of reactive diluents in enabling precise viscosity control and ensuring proper curing continues to support their widespread use across various manufacturing environments.

North America Reactive Diluents Market is expected to grow from USD 378 million in 2025 to USD 781.6 million by 2035, reflecting steady expansion across the region. The presence of a well-established industrial base, including coatings, adhesives, and composite manufacturing sectors, continues to drive demand for advanced formulation solutions. Industries in the region emphasize performance consistency, reduced solvent usage, and compliance with environmental and safety standards. The need for materials that offer controlled processing characteristics and reliable end-product quality further supports market growth, positioning North America as a key contributor to global demand.

Key companies operating in the Global Reactive Diluents Market include BASF SE, Arkema, Huntsman International LLC., Evonik Industries, Aditya Birla Chemicals, Atul Ltd, ADEKA Corporation, Cargill, DIC Corporation, GEO Specialty Chemicals, Bodo Moller Chemie GmbH, and NIPPON SHOKUBAI CO., LTD. Companies in the Reactive Diluents Market are focusing on innovation, product differentiation, and strategic collaborations to strengthen their market position. Investment in research and development is enabling the creation of advanced formulations that meet evolving industry requirements for performance, sustainability, and regulatory compliance. Firms are expanding their product portfolios with application-specific solutions tailored to different resin systems and end-use industries. Partnerships with manufacturers and end users are helping improve market reach and ensure alignment with customer needs. Companies are also enhancing production capabilities and adopting efficient manufacturing processes to improve scalability and cost-effectiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Function

- 2.2.3 Curing Mechanism

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for low viscosity systems

- 3.2.1.2 Expanding use in coatings applications

- 3.2.1.3 Growing focus on solvent reduction

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Performance variation across resin types

- 3.2.2.2 Sensitivity to formulation compatibility

- 3.2.3 Opportunities

- 3.2.3.1 Increasing adoption in composite materials

- 3.2.3.2 Development of application specific formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aliphatic

- 5.3 Aromatic

- 5.4 Cycloaliphatic

Chapter 6 Market Estimates and Forecast, By Function, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Supermarkets/hypermarkets

- 6.3 Specialty stores

- 6.4 Discount stores

- 6.5 Convenience stores

- 6.6 E-commerce

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Curing Mechanism, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 UV/EB curable

- 7.3 Thermal cure

- 7.4 Moisture cure

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Huntsman International LLC.

- 9.2 Aditya Birla Chemicals

- 9.3 Arkema

- 9.4 Evonik Industries

- 9.5 Atul Ltd

- 9.6 ADEKA CORPORATION

- 9.7 DIC CORPORATION

- 9.8 GEO Specialty Chemicals

- 9.9 BASF SE

- 9.10 NIPPON SHOKUBAI CO., LTD

- 9.11 Cargill

- 9.12 Bodo Moller Chemie GmbH