PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998821

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998821

Industrial Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

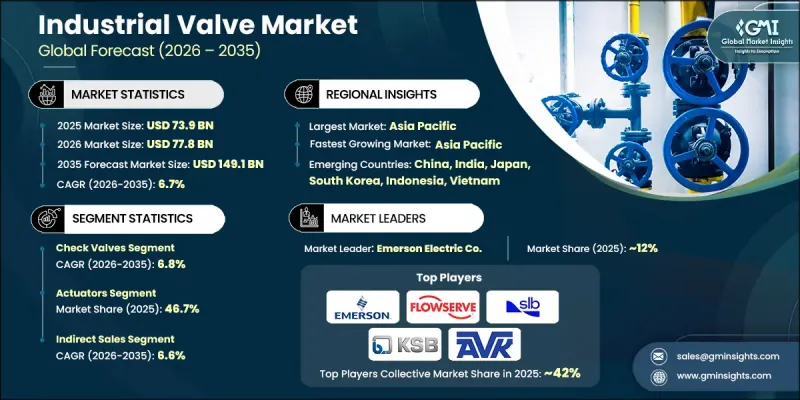

The Global Industrial Valve Market was valued at USD 73.9 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 149.1 billion by 2035.

The industrial valve market continues to gain momentum as global investment in energy generation and large-scale infrastructure development accelerates. Both public and private sector organizations are increasing capital spending on power plants, utility systems, and industrial processing facilities, which significantly boosts the demand for advanced valve technologies. Valves play a fundamental role in managing flow control and pressure stability across industrial systems, particularly in energy production and resource extraction activities. As renewable energy installations expand globally, complex piping networks used in modern energy systems require highly reliable valves to regulate fluid movement efficiently. Infrastructure upgrades across urban regions are also contributing to market growth, particularly as water distribution and wastewater treatment systems expand to meet rising population demands. Industrial valves remain essential components in maintaining pipeline safety, operational reliability, and efficient process control across numerous industrial environments. Growing petrochemical production capacity further contributes to demand, as processing facilities require extensive valve installations to support continuous operations. Additionally, large engineering and construction projects increasingly incorporate valve systems during the design and planning stages to ensure long-term operational efficiency and safety compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $73.9 Billion |

| Forecast Value | $149.1 Billion |

| CAGR | 6.7% |

The check valves segment generated USD 14.4 billion in 2025 and is expected to grow at a CAGR of 6.8% from 2026 through 2035. Check valves represent one of the most widely used valve types because they play a critical role in preventing reverse flow within pipeline systems. By maintaining one-directional fluid movement, these valves help protect pumps, pipelines, and process equipment from operational damage. Their relatively simple mechanical design reduces maintenance requirements while ensuring dependable system performance. High durability under demanding pressure conditions further strengthens their suitability for industrial environments. Ongoing expansion of pipeline infrastructure and industrial facilities continues to reinforce global demand for these valve systems.

The actuators segment held 46.7% share in 2025 and is forecast to grow at a CAGR of 7.2% between 2026 and 2035. Actuators have emerged as the leading component category due to the increasing adoption of automation across industrial operations. Automated valve systems significantly enhance process precision, operational reliability, and overall system efficiency. Industries operating complex processing environments increasingly rely on actuator-driven valves to enable remote operation and centralized process management. Advanced actuator technologies improve system responsiveness while minimizing the need for manual adjustments. Integration with digital control systems also allows real-time performance monitoring and operational optimization. As industries continue modernizing facilities to improve productivity and safety standards, actuator adoption is expected to remain strong worldwide.

China Industrial Valve Market accounted for USD 9.20 billion in 2025. The country's market growth is supported by extensive industrial manufacturing capacity and large-scale energy infrastructure development. Significant investments in power generation facilities are contributing to higher demand for industrial valve installations across multiple industrial segments. Expansion of petrochemical production infrastructure is also increasing the need for high-performance valves capable of handling demanding operational conditions. In addition, large urban infrastructure programs aimed at improving water management systems are generating consistent procurement demand for valve technologies. Domestic manufacturers continue expanding production capacity to support major industrial and infrastructure projects. Export-oriented equipment manufacturing further sustains steady replacement demand in global markets.

Major companies participating in the Global Industrial Valve Market include Emerson Electric Co., Crane Company, Danfoss, Baker Hughes Company, SLB, TechnipFMC plc, The Weir Group PLC, ITT Inc., KITZ Corporation, KSB SE & Co. KGaA, Hitachi Ltd., Georg Fischer Ltd., Mueller Co. LLC., AVK Holding A/S, and Alfa Laval. Companies operating in the Industrial Valve Market are strengthening their competitive position by focusing on innovation, strategic partnerships, and global expansion initiatives. Many manufacturers are investing in advanced valve technologies that support automation, digital monitoring, and predictive maintenance capabilities. Continuous research and development efforts are helping companies improve valve durability, operational efficiency, and compatibility with complex industrial systems. Strategic acquisitions and collaborations allow firms to expand their product portfolios and gain access to specialized technologies and regional markets. Manufacturers are also increasing investments in production facilities and supply chain networks to support growing infrastructure and energy projects worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Material

- 2.2.3 Component

- 2.2.4 Size

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding energy and infrastructure investments

- 3.2.1.2 Adoption of smart and IoT-enabled valve technologies

- 3.2.1.3 Industrial automation and Industry 4.0 implementation

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Raw material price volatility and supply chain instability

- 3.2.2.2 Stringent regulatory compliance and certification demands

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into renewable and clean energy infrastructure

- 3.2.3.2 Development of corrosion-resistant and performance-enhancing materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code - 8481)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Ball Valves

- 5.3 Check Valves

- 5.4 Butterfly Valves

- 5.5 Gate Valves

- 5.6 Globe Valves

- 5.7 Plug Valves

- 5.8 Diaphragm Valves

- 5.9 Safety Valves

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Plastic

- 6.4 Cast Iron

- 6.5 Alloy Based

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Component, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Actuators

- 7.3 Valve Body

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Size, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 <1"

- 8.3 1" to 6"

- 8.4 7" to 25"

- 8.5 26" to 50"

- 8.6 >50"

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Chemical

- 9.3 Energy & Utilities

- 9.4 Construction

- 9.5 Metal & Mining

- 9.6 Agriculture

- 9.7 Pharmaceutical

- 9.8 Food & Beverage

- 9.9 Pulp & Paper

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 ALFA LAVAL

- 12.2 AVK Holding A/S

- 12.3 Baker Hughes Company

- 12.4 Crane Company

- 12.5 Danfoss

- 12.6 Emerson Electric Co.

- 12.7 Georg Fischer Ltd.

- 12.8 Hitachi, Ltd.

- 12.9 ITT INC.

- 12.10 KITZ Corporation

- 12.11 KSB SE & Co. KGaA

- 12.12 Mueller Co. LLC.

- 12.13 SLB (Schlumberger Limited.)

- 12.14 TechnipFMC plc

- 12.15 The Weir Group PLC