PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2060327

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2060327

Industrial Valve Market by Valve (Globe, ball, butterfly, solenoid, plug, spring, tank vent, pinch, gate, diaphragm, pilot, check, safety, needle, relief), Size (<1",1"-6", 6"-25",25"-50", >50"), Media (Liquid, Gas, Slurry) -Global Forecast to 2032

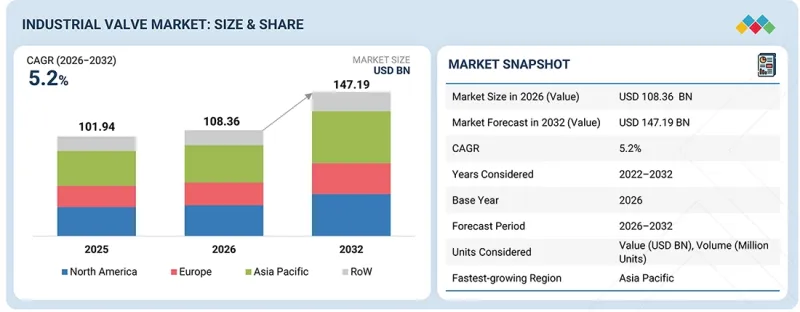

According to MarketsandMarkets, the industrial valve market is projected to reach USD 147.19 billion by 2032 from USD 108.36 billion in 2026, at a CAGR of 5.2%. The industrial valve market is projected to witness steady growth during the forecast period, driven by increasing demand for reliable flow control, isolation, pressure regulation, pressure relief, backflow prevention, throttling, diversion, and emergency shutdown applications across major industries. Rising investments in oil & gas pipelines, refineries, power plants, chemical processing facilities, water & wastewater treatment plants, and industrial infrastructure support the market growth.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Valve, Size, Media and Region |

| Regions covered | North America, Europe, APAC, RoW |

As industrial operations involve high-pressure fluids, corrosive media, steam, gas, slurry, and hazardous process conditions, end users are prioritizing durable and efficient valve systems to improve plant safety, reduce downtime, and ensure regulatory compliance. Additionally, the increasing adoption of actuated valves, control valves, smart valve monitoring systems, and IIoT-enabled predictive maintenance solutions is improving operational efficiency and process reliability. Demand for corrosion-resistant, high-pressure, and severe-service valves is also increasing across oil & gas, chemicals, energy & power, water & wastewater treatment, and other process industries. The long-term need for safer operations, infrastructure upgrades, automation, and efficient fluid handling is expected to support the continued growth of the global industrial valve market.

By valve type, linear valves will capture largest market share throughout forecast period

Linear valves are expected to hold the largest share of the industrial valve market due to their wide use in flow regulation, throttling, pressure control, backflow prevention, and safety applications. These valves are extensively used across oil & gas, chemicals, water & wastewater treatment, energy & power, pharmaceuticals, and process industries where reliable fluid control is critical. Their suitability for high-pressure, high-temperature, corrosive, and severe-service operating environments supports their adoption across industrial plants. Increasing demand for process efficiency, plant safety, and automation is further supporting the growth of the linear valve segment in the industrial valve market.

By valve size, 1" to 6" segment to capture significant market share during forecast period

1" to 6" valves are expected to capture a significant share of the industrial valve market due to their broad use across industrial pipelines, process control systems, utility lines, water treatment facilities, and manufacturing plants. These valves are widely used in medium-flow applications across oil & gas, chemicals, energy & power, water & wastewater treatment, food & beverages, and pharmaceuticals industries. Their ease of installation, compatibility with different valve types, and suitability across liquid, gas, and slurry applications make them highly preferred. Increasing investment in plant utilities, water infrastructure, and process automation is further driving the adoption of 1" to 6" valves.

Asia Pacific to be largest market for industrial valves during forecast period

Asia Pacific is likely to remain the largest market for industrial valves during the forecast period due to rapid industrialization, infrastructure development, and strong growth across key end-use industries. Increasing investments in oil & gas pipelines, refineries, chemical plants, power generation facilities, water & wastewater treatment systems, and manufacturing industries across China, India, Japan, South Korea, and Southeast Asia are significantly driving demand for industrial valves. The region's expanding industrial base, rising focus on automation, and growing need for reliable flow control, pressure regulation, isolation, and safety systems are supporting market growth. Additionally, strong demand for water infrastructure modernization, energy projects, and process industry expansion is strengthening the Asia Pacific's position in the global industrial valve market. The presence of large manufacturing hubs, cost-competitive valve suppliers, and increasing adoption of smart and automated valves are further enhancing regional market penetration. As industries continue to invest in safety, efficiency, and plant reliability, Asia Pacific is expected to maintain its leading position in the industrial valve market.

Breakdown of Primaries

A variety of executives from key organizations operating in the industrial valve market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 30%, and RoW - 10%

Note: The RoW region includes the Middle East, Africa, and South America. Other designations include product, sales, and marketing managers. Three tiers of companies have been defined based on their total revenues as of 2025: Tier 3: revenue less than USD 100 million; Tier 2: revenue between USD 100 million and USD 1 billion; and Tier 1: revenue more than USD 1 billion.

Major players profiled in this report are as follows: Major players operating in the industrial valve market include Emerson Electric Co. (US), SLB (US), Flowserve Corporation (US), IMI plc (UK), Neway Valve (China), Crane Co. (US), KITZ Corporation (Japan), Parker Hannifin Corporation (US), Alfa Laval AB (Sweden), KSB SE & Co. KGaA (Germany), Curtiss-Wright Corporation (US), Spirax Group (UK), Watts Water Technologies (US), Bray International (US), and CIRCOR International (US), among others.

These companies compete by continuously expanding their industrial valve portfolios, strengthening automation capabilities, and improving valve performance across flow control, isolation, pressure regulation, pressure relief, backflow prevention, throttling, diversion, and emergency shutdown applications. Strategic emphasis is placed on developing advanced rotary valves, linear valves, safety valves, actuators, control valves, and corrosion-resistant valve solutions for industries such as oil & gas, energy & power, water & wastewater treatment, chemicals, pharmaceuticals, food & beverages, metals & mining, and semiconductors. Market participants prioritize reliable performance, material compatibility, high-pressure handling, severe-service capability, regulatory compliance, and aftermarket support. Continued investments in smart valve monitoring, actuated valves, IIoT-enabled maintenance, and expansion across high-growth industrial regions are expected to sustain competition and accelerate adoption across the global industrial valve market.

The study provides a detailed competitive analysis of these key players in the industrial valve market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report on the industrial valve market presents a detailed analysis based on region, valve type, safety valve type, pressure range, media type, valve size, material, component, function, and end-use industry. By valve type, the market is segmented into rotary valves and linear valves. Rotary valves include ball, butterfly, and plug valves, while linear valves include globe, check, gate, diaphragm, safety, needle, pinch, solenoid, and angle valves. By pressure range, the market covers up to 50 bar, >50-350 bar, >350-700 bar, >700-1,000 bar, and >1,000 bar. By end-use industry, the market covers oil & gas, energy & power, water & wastewater treatment, chemicals, pharmaceuticals, building & construction, food & beverages, metals & mining, paper & pulp, agriculture, semiconductor, and other process industries. The regional analysis includes North America, Europe, Asia Pacific, and RoW, enabling evaluation of demand patterns, growth drivers, and industry trends. The components segment includes actuators, valve body, and other components, while the function segment comprises on-off and control functions.

Reasons to Buy the Report

The report will help leaders and new entrants in the industrial valve market with information on the closest approximations of the revenue numbers for the overall market and its subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the industrial valve market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (increasing need to establish new power plants and revamp existing ones, Growing use of connected networks and smart industrial valves), restraints (high capital investments and low profit margins, volatility in raw material prices, particularly steel and alloys), opportunities (integration of industrial valves with IIoT, AI, Industry 5.0, and additive manufacturing, Increasing investments in water & wastewater treatment infrastructure), and challenges (intense price competition due to fragmented market structure).

ensuring durability and performance in extreme operating conditions influencing the growth of the hydrogen sensor market

- Product Development/Innovation: Detailed insights on upcoming valve technologies, smart actuators, control valves, corrosion-resistant valves, pressure-relief valves, and new product launches in the industrial valve market

- Market Development: Comprehensive information about attractive markets by analyzing industrial valve demand across North America, Europe, Asia Pacific, and RoW

- Market Diversification: Exhaustive information about new products, services, untapped geographies, recent developments, and investments across valve OEMs, actuator suppliers, automation providers, and aftermarket service companies

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Emerson Electric Co. (US), SLB (US), Flowserve Corporation (US), IMI plc (UK), Neway Valve (China), Crane Co. (US), KITZ Corporation (Japan), Parker Hannifin Corporation (US), Alfa Laval AB (Sweden), and KSB SE & Co. KGaA (Germany).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN INDUSTRIAL VALVE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES IN INDUSTRIAL VALVE MARKET

- 3.2 INDUSTRIAL VALVE MARKET, BY LINEAR VALVE TYPE, 2026 VS. 2032

- 3.3 INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026 VS. 2032

- 3.4 INDUSTRIAL VALVE MARKET, BY PRESSURE RANGE, 2026 VS. 2032

- 3.5 INDUSTRIAL VALVE MARKET, BY MATERIAL, 2026 VS. 2032

- 3.6 INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026 VS. 2032

- 3.7 INDUSTRIAL VALVE MARKET, BY GEOGRAPHY, 2026-2032

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing need to establish new power plants and revamp existing ones

- 4.2.1.2 Growing use of connected networks and smart industrial valves

- 4.2.1.3 Expansion of oil & gas and energy infrastructure

- 4.2.1.4 Rapid industrialization and manufacturing growth in emerging economies

- 4.2.1.5 Rising adoption of automation and process optimization technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital investments and low profit margins

- 4.2.2.2 Volatility in raw material prices, particularly steel and alloys

- 4.2.2.3 Stringent regulatory and certification requirements across industries

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of industrial valves with IIoT, AI, Industry 5.0, and additive manufacturing

- 4.2.3.2 Increasing investments in water & wastewater treatment infrastructure

- 4.2.3.3 Rising demand for high-performance valves in extreme environments (high pressure, temperature, corrosive media)

- 4.2.3.4 Emerging applications in hydrogen, LNG, and carbon capture systems

- 4.2.3.5 Expansion of aftermarket services and valve replacement demand

- 4.2.4 CHALLENGES

- 4.2.4.1 Intense price competition due to fragmented market structure

- 4.2.4.2 Ensuring durability and performance in extreme operating conditions

- 4.2.4.3 Supply chain disruptions and dependency on industrial demand cycles

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 BARGAINING POWER OF SUPPLIERS

- 5.2.2 BARGAINING POWER OF BUYERS

- 5.2.3 THREAT OF NEW ENTRANTS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL OIL & GAS INDUSTRY

- 5.3.4 TRENDS IN GLOBAL WATER & WASTEWATER TREATMENT INDUSTRY

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 COMPANY-WISE INDICATIVE SELLING PRICE OF INDUSTRIAL VALVES, BY VALVE TYPE, 2025

- 5.6.2 AVERAGE SELLING PRICE OF INDUSTRIAL VALVES OFFERED BY KEY PLAYERS, BY TYPE, 2025

- 5.6.3 INDICATIVE PRICE TREND OF INDUSTRIAL VALVES, BY REGION

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (8481)

- 5.7.2 EXPORT SCENARIO (8481)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 EUROPEAN LNG PLANT IMPROVES MAIN CRYOGENIC HEAT EXCHANGER PERFORMANCE WITH FISHER JT CONTROL VALVE

- 5.11.2 FLOWSERVE (MOGAS) SEVERE SERVICE ISOLATION VALVES SOLVE EXTREME PROCESS CONDITIONS IN MINING & MINERAL EXTRACTION

- 5.11.3 LEAKING GLOBE VALVES REPLACED WITH ZERO-LEAKAGE BALL VALVES IN HRSG POWER PLANT

- 5.11.4 SPECIALTY PAPER MILL SOLVES STEAM LEAKAGE WITH METAL-SEATED BALL VALVES

- 5.11.5 REMOTE ALASKA PIPELINE RECEIVES FAIL-SAFE, SELF-RESETTING ESD VALVE ACTUATION IN EXTREME CONDITIONS

- 5.12 IMPACT OF 2025 US TARIFF - INDUSTRIAL VALVE MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SMART VALVE POSITIONERS

- 6.1.2 ADVANCE SEALING TECHNOLOGIES

- 6.1.3 HIGH-PRESSURE SAFETY MECHANISMS

- 6.1.4 ANTI-CORROSION MATERIALS

- 6.1.5 LOW-EMISSION VALVE TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INDUSTRIAL ACTUATORS

- 6.2.2 INDUSTRIAL SENSORS

- 6.2.3 INDUSTRIAL CONNECTIVITY PLATFORMS (SCADA/DCS/IIOT)

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INDUSTRIAL PUMPS

- 6.3.2 COMPRESSORS

- 6.3.3 FLOW METERS

- 6.3.4 PRESSURE REGULATORS

- 6.3.5 EXPANSION VALVES

- 6.4 TECHNOLOGY/ PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI/GEN AI ON INDUSTRIAL VALVE MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN INDUSTRIAL VALVE MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN INDUSTRIAL VALVE MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATION IN INDUSTRIAL VALVE

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 REGULATIONS

- 7.1.3.1 North America

- 7.1.3.1.1 US

- 7.1.3.1.2 Canada

- 7.1.3.2 Europe

- 7.1.3.2.1 European Union

- 7.1.3.2.2 Germany

- 7.1.3.2.3 UK

- 7.1.3.3 Asia Pacific

- 7.1.3.3.1 China

- 7.1.3.3.2 Japan

- 7.1.3.1 North America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS INDUSTRIES

9 INDUSTRIAL VALVE MARKET, BY VALVE SEALING

- 9.1 INTRODUCTION

- 9.2 SOFT-SEATED VALVES

- 9.2.1 ZERO-LEAKAGE SEALING AND LOWER LIFECYCLE COST TO SUPPORT DEMAND

- 9.3 METAL-SEATED VALVES

- 9.3.1 DURABILITY IN HIGH-TEMPERATURE, HIGH-PRESSURE, AND ABRASIVE SERVICES TO SUPPORT MARKET GROWTH

- 9.4 PACKING-SEATED VALVES

- 9.4.1 ADJUSTABLE STEM SEALING AND MAINTENANCE FLEXIBILITY TO SUPPORT DEMAND

10 INDUSTRIAL VALVE MARKET, BY VALVE TYPE

- 10.1 INTRODUCTION

- 10.2 ROTARY VALVES

- 10.2.1 BALL VALVES

- 10.2.1.1 Tight sealing and low operating torque to drive demand

- 10.2.1.2 Trunnion-mounted ball valves

- 10.2.1.3 Floating ball valves

- 10.2.1.4 Rising stem ball valves

- 10.2.2 BUTTERFLY VALVES

- 10.2.2.1 Cost-effectiveness and compact design to boost market growth

- 10.2.2.2 Zero-offset butterfly valves

- 10.2.2.3 Double-offset butterfly valves

- 10.2.2.4 Triple-offset butterfly valves

- 10.2.3 PLUG VALVES

- 10.2.3.1 Easy sealing and isolation to boost adoption in wastewater treatment plants

- 10.2.1 BALL VALVES

- 10.3 LINEAR VALVES

- 10.3.1 GLOBE VALVES

- 10.3.1.1 Precise flow control requirements in process industries to drive demand for globe valve

- 10.3.2 DIAPHRAGM VALVES

- 10.3.2.1 Corrosion resistance and contamination-free operation to support adoption

- 10.3.3 GATE VALVES

- 10.3.3.1 Reliable isolation performance in large-diameter pipelines to drive gate valve adoption

- 10.3.3.2 Standard plate gate valves

- 10.3.3.3 Wedge-type gate valves

- 10.3.3.4 Knife gate valves

- 10.3.4 SAFETY VALVES

- 10.3.4.1 Overpressure protection demand from oil & gas, power, and chemical industries to support growth

- 10.3.5 CHECK VALVES

- 10.3.5.1 Reverse-flow prevention in pipelines to support check valve demand

- 10.3.6 NEEDLE VALVES

- 10.3.6.1 Precision flow regulation to drive use in oil & gas, pharmaceuticals, and water applications

- 10.3.7 PINCH VALVES

- 10.3.7.1 Abrasive-media handling and low-maintenance slurry control to support adoption

- 10.3.8 SOLENOID VALVES

- 10.3.8.1 Automation-led demand for fast and efficient fluid control systems to support growth

- 10.3.1 GLOBE VALVES

11 INDUSTRIAL VALVE MARKET, BY SAFETY VALVE TYPE

- 11.1 INTRODUCTION

- 11.2 VALVE TYPE

- 11.2.1 SPRING

- 11.2.2 PILOT

- 11.2.3 VENT

- 11.2.4 RUPTURE DISCS

- 11.3 PRESSURE RANGE

- 11.3.1 <50 BAR

- 11.3.2 50-350 BAR

- 11.3.3 350-700 BAR

- 11.3.4 700-1000 BAR

- 11.3.5 >1000 BAR

- 11.4 MEDIA TYPE

- 11.4.1 LIQUID

- 11.4.2 GAS

- 11.4.3 SLURRY

- 11.5 VALVE SIZE

- 11.5.1 < 1"

- 11.5.2 1-6"

- 11.5.3 7-25"

- 11.5.4 26-50"

- 11.5.5 >50"

- 11.6 VALVE MATERIAL

- 11.6.1 STEEL

- 11.6.2 ALLOY-BASED

- 11.6.3 CAST IRON

- 11.6.4 ALUMINUM

- 11.6.5 PLASTIC

- 11.6.6 OTHER MATERIALS

- 11.7 END-USE INDUSTRY

- 11.7.1 OIL & GAS

- 11.7.2 ENERGY & POWER

- 11.7.3 WATER & WASTEWATER TREATMENT

- 11.7.4 CHEMICAL

- 11.7.5 PHARMACEUTICALS

- 11.7.6 BUILDING & CONSTRUCTION

- 11.7.7 FOOD & BEVERAGES

- 11.7.8 METALS & MINING

- 11.7.9 PAPER & PULP

- 11.7.10 AGRICULTURE

- 11.7.11 SEMICONDUCTOR

- 11.7.12 OTHER END-USE INDUSTRIES

12 INDUSTRIAL VALVE MARKET, BY MEDIA TYPE

- 12.1 INTRODUCTION

- 12.2 LIQUID

- 12.2.1 WATER TREATMENT, PROCESS AUTOMATION, AND LEAK-CONTROL NEEDS TO SUPPORT DEMAND

- 12.2.2 WATER VALVES

- 12.2.2.1 Rising investments in water infrastructure and treatment facilities to drive demand for industrial water valves

- 12.2.3 OIL VALVES

- 12.2.3.1 Increasing oil & gas exploration, production, and pipeline investments to drive demand for industrial oil valves

- 12.2.4 CHEMICAL VALVES

- 12.2.4.1 Increasing use of corrosive and hazardous chemicals to drive growth in chemical valve installations

- 12.3 GAS

- 12.3.1 SAFETY-FOCUSED GAS FLOW CONTROL TO SUPPORT DEMAND IN PIPELINES, REFINERIES, AND INDUSTRIAL SYSTEMS

- 12.3.2 NATURAL GAS

- 12.3.2.1 Natural gases to boost demand for industrial valves in extraction and distribution

- 12.3.2.2 Methane

- 12.3.2.3 Ethane

- 12.3.2.4 Propane

- 12.3.3 COMPRESSED AIR

- 12.3.3.1 Automation and energy-efficiency need to support demand

- 12.3.4 INDUSTRIAL GAS

- 12.3.4.1 Reliable gas-flow regulation and safety compliance to support demand

- 12.3.4.2 Hydrogen

- 12.3.4.3 Nitrogen

- 12.3.4.4 Oxygen

- 12.3.4.5 Other industrial gases

- 12.4 SLURRY

- 12.4.1 ABRASION-RESISTANT SLURRY FLOW CONTROL TO SUPPORT DEMAND IN MINING, WASTEWATER, AND POWER APPLICATIONS

- 12.4.2 CEMENT

- 12.4.2.1 Rising demand to manage flow of abrasive and viscous cement slurries used in construction and oilfield applications to drive market

- 12.4.3 SLUDGE

- 12.4.3.1 Designed to manage flow of sludge slurries encountered in wastewater treatment, mining, and industrial processes

13 INDUSTRIAL VALVE MARKET, BY COMPONENT

- 13.1 INTRODUCTION

- 13.2 ACTUATORS

- 13.2.1 PNEUMATIC ACTUATORS

- 13.2.1.1 Automation, compressed-air efficiency, and cost advantages to support demand

- 13.2.1.2 Diaphragm actuators

- 13.2.1.3 Piston actuators

- 13.2.2 ELECTRIC ACTUATORS

- 13.2.2.1 Remote operation and precise valve positioning to support demand in water, wastewater, and chemical plants

- 13.2.3 HYDRAULIC ACTUATORS

- 13.2.3.1 Integration of hydraulic actuators in HVAC, fire protection, and irrigation systems to propel growth

- 13.2.1 PNEUMATIC ACTUATORS

- 13.3 VALVE BODIES

- 13.3.1 CORROSION-RESISTANT AND PRESSURE-RATED VALVE BODIES TO SUPPORT DURABILITY IN CHEMICAL AND PROCESS APPLICATIONS

- 13.4 OTHER COMPONENTS

14 INDUSTRIAL VALVE MARKET, BY FUNCTION

- 14.1 INTRODUCTION

- 14.2 ON/OFF VALVES

- 14.2.1 INCREASING USE IN THROTTLING APPLICATIONS TO DRIVE MARKET

- 14.3 CONTROL VALVES

- 14.3.1 NEED TO CONTROL TEMPERATURE, FLOW, AND PRESSURE IN INDUSTRIAL PROCESSES TO FAVOR MARKET GROWTH

- 14.3.2 MODULATING VALVES

- 14.3.3 POSITION-CONTROLLED VALVES

- 14.3.3.1 Quarter-turn valves

- 14.3.3.2 Multi-turn valves

15 INDUSTRIAL VALVE MARKET, BY MATERIAL

- 15.1 INTRODUCTION

- 15.2 STEEL

- 15.2.1 STRESS-CORROSION RESISTANCE AND HIGH-PRESSURE RELIABILITY TO SUPPORT STEEL VALVE ADOPTION IN NATURAL GAS AND PROCESS INDUSTRIES

- 15.3 CAST IRON

- 15.3.1 WATER AND WASTEWATER INFRASTRUCTURE DEMAND TO SUPPORT ADOPTION

- 15.4 ALUMINUM

- 15.4.1 LIGHTWEIGHT AND CORROSION-RESISTANT VALVE MATERIALS TO SUPPORT AEROSPACE, AUTOMOTIVE, HVAC, AND COMPACT SYSTEM APPLICATIONS

- 15.5 ALLOY-BASED

- 15.5.1 HIGH-STRENGTH ALLOY MATERIALS TO SUPPORT VALVE USE IN HIGH-PRESSURE, HIGH-TEMPERATURE PROCESSES

- 15.5.2 NICKEL-ALUMINUM

- 15.5.3 NICKEL-CHROMIUM

- 15.6 PLASTIC

- 15.6.1 CORROSION-RESISTANT AND LIGHTWEIGHT PLASTIC VALVES TO SUPPORT DEMAND IN CHEMICAL, WATER, AND LOW-PRESSURE FLUID APPLICATIONS

- 15.7 OTHER MATERIALS

- 15.7.1 BRONZE

- 15.7.2 BRASS

16 INDUSTRIAL VALVE MARKET, BY VALVE SIZE

- 16.1 INTRODUCTION

- 16.2 <1"

- 16.2.1 INCREASING NEED FOR COMPACT AND EFFECTIVE TECHNOLOGIES TO DRIVE MARKET

- 16.3 1-6"

- 16.3.1 COMPACT SIZE TO INCREASE ADOPTION IN OIL & GAS AND CHEMICAL INDUSTRIES

- 16.4 6-25"

- 16.4.1 INCREASING ADOPTION IN OIL & GAS INDUSTRY TO CREATE OPPORTUNITIES FOR VALVE PROVIDERS

- 16.5 25-50"

- 16.5.1 GROWING NEED FOR FUNCTIONAL VALVES IN HIGH-TEMPERATURE AND HIGH-PRESSURE ENVIRONMENTS TO PROPEL MARKET

- 16.6 >50"

- 16.6.1 INCREASED ADOPTION OF HIGH-CAPACITY SYSTEMS TO BOOST MARKET DEMAND

17 INDUSTRIAL VALVE MARKET, BY PRESSURE RANGE

- 17.1 INTRODUCTION

- 17.2 <50 BAR

- 17.2.1 LOW-PRESSURE VALVE DEMAND IN HVAC, FOOD & BEVERAGE, AND PHARMACEUTICAL FLOW-CONTROL APPLICATIONS TO DRIVE MARKET

- 17.3 50-350 BAR

- 17.3.1 SMART MANUFACTURING AND MEDIUM-PRESSURE PROCESS CONTROL TO SUPPORT DEMAND

- 17.4 350-700 BAR

- 17.4.1 HIGH-PRESSURE PROCESS CONTROL IN OIL & GAS, CHEMICAL, AND POWER APPLICATIONS TO DRIVE DEMAND

- 17.5 700-1000 BAR

- 17.5.1 ULTRA-HIGH-PRESSURE VALVE PERFORMANCE TO SUPPORT AEROSPACE, HYDRAULIC, AND CHEMICAL PROCESSING APPLICATIONS

- 17.6 >1000 BAR

- 17.6.1 NEED FOR EQUIPMENT THAT CAN PERFORM UNDER EXTREME CONDITIONS TO DRIVE MARKET

18 INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY

- 18.1 INTRODUCTION

- 18.2 OIL & GAS

- 18.2.1 PIPELINE EXPANSION, DEEPWATER OPERATIONS, AND REFINERY MAINTENANCE TO SUPPORT OIL & GAS VALVE DEMAND

- 18.2.2 UPSTREAM

- 18.2.3 MIDSTREAM

- 18.2.4 DOWNSTREAM

- 18.3 WATER & WASTEWATER TREATMENT

- 18.3.1 HIGH INVESTMENTS IN ESTABLISHING WATER TREATMENT PLANTS TO PROPEL MARKET GROWTH

- 18.3.2 WATER DISTRIBUTION SYSTEMS

- 18.3.3 DESALINATION UNITS

- 18.4 ENERGY & POWER

- 18.4.1 RISING ELECTRICITY DEMAND, POWER-PLANT UPGRADES, AND CLEAN-ENERGY INVESTMENTS TO SUPPORT VALVE DEMAND

- 18.4.2 CONVENTIONAL POWER PLANTS

- 18.4.3 RENEWABLE ENERGY PLANTS

- 18.5 PHARMACEUTICALS

- 18.5.1 AUTOMATION, STERILE PROCESSING, AND RELIABLE DRUG SUPPLY NEEDS TO SUPPORT PHARMACEUTICAL VALVE DEMAND

- 18.5.2 STERILIZATION PROCESS

- 18.5.3 PACKAGING & FILLING

- 18.6 FOOD & BEVERAGES

- 18.6.1 LEAKPROOF, CLEANABLE, AND AUTOMATED VALVE SYSTEMS TO SUPPORT FOOD & BEVERAGE PROCESSING DEMAND

- 18.6.2 BEVERAGE PRODUCTION

- 18.6.3 DAIRY PRODUCTION

- 18.7 CHEMICALS

- 18.7.1 EMISSION CONTROL, PLANT SAFETY, AND CORROSION-RESISTANT FLOW MANAGEMENT TO SUPPORT VALVE DEMAND IN CHEMICAL PROCESSING

- 18.7.2 BATCH PROCESSING

- 18.7.3 FILTRATION PROCESS

- 18.8 BUILDING & CONSTRUCTION

- 18.8.1 INCREASING INFRASTRUCTURAL INVESTMENTS AND GROWING FOCUS ON BETTER SAFETY STANDARDS TO AID MARKET GROWTH

- 18.8.2 HVAC APPLICATION

- 18.8.3 FIRE PROTECTION

- 18.9 PAPER & PULP

- 18.9.1 ENERGY-EFFICIENT PULP PROCESSING, RECYCLING, AND CHEMICAL RECOVERY TO SUPPORT DEMAND

- 18.9.2 PAPER FORMATION

- 18.9.3 BLENDING

- 18.10 METALS & MINING

- 18.10.1 INDUSTRIAL VALVES IN MINING OPERATIONS TO ENSURE EFFICIENT OPERATIONS

- 18.10.2 HYDROMETALLURGY

- 18.10.3 CONVEYOR SYSTEMS

- 18.11 AGRICULTURE

- 18.11.1 PRECISION IRRIGATION, CLOG PREVENTION, AND AUTOMATED WATER CONTROL TO SUPPORT AGRICULTURAL VALVE DEMAND

- 18.11.2 SPRINKLER SYSTEMS

- 18.11.3 WATER STORAGE TANKS

- 18.12 SEMICONDUCTOR

- 18.12.1 CHIP DEMAND FROM ELECTRONICS, AUTOMOTIVE, AND AI APPLICATIONS TO SUPPORT ULTRA-HIGH-PURITY VALVE ADOPTION

- 18.12.2 WAFER PROCESSING

- 18.12.3 VACUUM SYSTEMS

- 18.13 OTHER END-USE INDUSTRIES

19 INDUSTRIAL VALVE MARKET, BY REGION

- 19.1 INTRODUCTION

- 19.2 NORTH AMERICA

- 19.2.1 US

- 19.2.1.1 Development of shale oil and gas resources to drive demand

- 19.2.2 CANADA

- 19.2.2.1 Natural gas pipeline expansion, critical minerals development, and HVAC demand to support market growth

- 19.2.3 MEXICO

- 19.2.3.1 Manufacturing integration, semiconductor supply-chain development, and oil & gas projects to drive demand

- 19.2.1 US

- 19.3 EUROPE

- 19.3.1 UK

- 19.3.1.1 Strong water regulation, pharmaceutical manufacturing, and UK-based valve OEM presence to drive market growth

- 19.3.2 GERMANY

- 19.3.2.1 Rising adoption of automated valves across chemical and process industries to drive market growth

- 19.3.3 FRANCE

- 19.3.3.1 Focus on renewable energy development to drive demand for industrial valves

- 19.3.4 ITALY

- 19.3.4.1 Increasing investments in water infrastructure and chemical processing to boost industrial valve demand

- 19.3.5 REST OF EUROPE

- 19.3.1 UK

- 19.4 ASIA PACIFIC

- 19.4.1 CHINA

- 19.4.1.1 Strong industrial base, pharmaceutical innovation, and process automation to support valve demand

- 19.4.2 JAPAN

- 19.4.2.1 Renewable energy, nuclear restart, and semiconductor manufacturing to support valve demand

- 19.4.3 SOUTH KOREA

- 19.4.3.1 Hydrogen economy, carbon-free energy, and semiconductor supply-chain growth to support industrial valve demand

- 19.4.4 INDIA

- 19.4.4.1 Increasing investments in power, oil & gas, water, and manufacturing sectors to drive market

- 19.4.5 REST OF ASIA PACIFIC

- 19.4.1 CHINA

- 19.5 REST OF THE WORLD

- 19.5.1 MIDDLE EAST

- 19.5.1.1 Oil & gas, petrochemical expansion, and desalination projects to support industrial valve demand

- 19.5.1.2 GCC Countries

- 19.5.1.2.1 Rising investments in oil & gas, petrochemical, and water management sectors to aid market growth

- 19.5.2 SOUTH AMERICA

- 19.5.2.1 Oil & gas, mining, and industrial investment to support valve demand

- 19.5.3 AFRICA

- 19.5.3.1 Water infrastructure, mining, and energy investments to create market opportunities

- 19.5.1 MIDDLE EAST

20 COMPETITIVE LANDSCAPE

- 20.1 INTRODUCTION

- 20.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 20.3 REVENUE ANALYSIS, 2021-2025

- 20.4 MARKET SHARE ANALYSIS, 2025

- 20.5 COMPANY VALUATION AND FINANCIAL METRICS

- 20.6 BRAND COMPARISON

- 20.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 20.7.1 STARS

- 20.7.2 EMERGING LEADERS

- 20.7.3 PERVASIVE PLAYERS

- 20.7.4 PARTICIPANTS

- 20.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 20.7.5.1 Company footprint

- 20.7.5.2 Region footprint

- 20.7.5.3 Valve type footprint

- 20.7.5.4 Media type footprint

- 20.7.5.5 End-use industry footprint

- 20.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 20.8.1 PROGRESSIVE COMPANIES

- 20.8.2 RESPONSIVE COMPANIES

- 20.8.3 DYNAMIC COMPANIES

- 20.8.4 STARTING BLOCKS

- 20.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 20.8.5.1 Detailed list of key startups/SMEs

- 20.8.5.2 Competitive benchmarking of key startups/SMEs

- 20.8.5.2.1 Competitive benchmarking of key startups/SMEs, by region

- 20.8.5.2.2 Competitive benchmarking of key startups/SMEs, by type

- 20.8.5.2.3 Competitive benchmarking of key startups/SMEs, by media type

- 20.8.5.2.4 Competitive benchmarking of key startups/SMEs, by end-use industry

- 20.9 COMPETITIVE SCENARIO

- 20.9.1 PRODUCT LAUNCHES

- 20.9.2 DEALS

- 20.9.3 EXPANSIONS

- 20.9.4 OTHER DEVELOPMENTS

21 COMPANY PROFILES

- 21.1 KEY PLAYERS

- 21.1.1 EMERSON ELECTRIC CO.

- 21.1.1.1 Business overview

- 21.1.1.2 Products offered

- 21.1.1.3 Recent developments

- 21.1.1.3.1 Product launches

- 21.1.1.4 MnM view

- 21.1.1.4.1 Key strengths/Right to win

- 21.1.1.4.2 Strategic choices

- 21.1.1.4.3 Weaknesses/Competitive threats

- 21.1.2 SLB

- 21.1.2.1 Business overview

- 21.1.2.2 Products offered

- 21.1.2.3 Recent developments

- 21.1.2.3.1 Expansions

- 21.1.2.4 MnM view

- 21.1.2.4.1 Key strengths/Right to win

- 21.1.2.4.2 Strategic choices

- 21.1.2.4.3 Weaknesses/Competitive threats

- 21.1.3 FLOWSERVE CORPORATION

- 21.1.3.1 Business overview

- 21.1.3.2 Products offered

- 21.1.3.3 Recent developments

- 21.1.3.3.1 Product launches

- 21.1.3.3.2 Deals

- 21.1.3.3.3 Other developments

- 21.1.3.4 MnM view

- 21.1.3.4.1 Key strengths/Right to win

- 21.1.3.4.2 Strategic choices

- 21.1.3.4.3 Weaknesses/Competitive threats

- 21.1.4 IMI

- 21.1.4.1 Business overview

- 21.1.4.2 Products offered

- 21.1.4.3 Recent developments

- 21.1.4.3.1 Product launches

- 21.1.4.3.2 Expansions

- 21.1.4.4 MnM view

- 21.1.4.4.1 Key strengths/Right to win

- 21.1.4.4.2 Strategic choices

- 21.1.4.4.3 Weaknesses/Competitive threats

- 21.1.5 CRANE HOLDINGS, CO.

- 21.1.5.1 Business overview

- 21.1.5.2 Products offered

- 21.1.5.3 Recent developments

- 21.1.5.3.1 Deals

- 21.1.5.3.2 Expansions

- 21.1.5.4 MnM view

- 21.1.5.4.1 Key strengths/Right to win

- 21.1.5.4.2 Strategic choices

- 21.1.5.4.3 Weaknesses/Competitive threats

- 21.1.6 VALMET

- 21.1.6.1 Business overview

- 21.1.6.2 Products offered

- 21.1.6.3 Recent developments

- 21.1.6.3.1 Product launches

- 21.1.6.3.2 Deals

- 21.1.7 NEWAY VALVE

- 21.1.7.1 Business overview

- 21.1.7.2 Products offered

- 21.1.7.3 Recent developments

- 21.1.7.3.1 Product launches

- 21.1.8 SPIRAX SARCO LIMITED

- 21.1.8.1 Business overview

- 21.1.8.2 Products offered

- 21.1.8.3 Recent developments

- 21.1.8.3.1 Deals

- 21.1.9 KITZ CORPORATION

- 21.1.9.1 Business overview

- 21.1.9.2 Products offered

- 21.1.9.3 Recent developments

- 21.1.9.3.1 Product launches

- 21.1.9.3.2 Deals

- 21.1.9.3.3 Expansions

- 21.1.10 KSB SE & CO. KGAA

- 21.1.10.1 Business overview

- 21.1.10.2 Products offered

- 21.1.10.3 Recent developments

- 21.1.10.3.1 Product launches

- 21.1.10.3.2 Expansions

- 21.1.11 ALFA LAVAL

- 21.1.11.1 Business overview

- 21.1.11.2 Products offered

- 21.1.11.3 Recent developments

- 21.1.11.3.1 Product launches

- 21.1.11.3.2 Deals

- 21.1.11.3.3 Other developments

- 21.1.12 CURTISS-WRIGHT CORPORATION

- 21.1.12.1 Business overview

- 21.1.12.2 Products offered

- 21.1.12.3 Recent developments

- 21.1.12.3.1 Product launches

- 21.1.13 PARKER HANNIFIN CORP.

- 21.1.13.1 Business overview

- 21.1.13.2 Products offered

- 21.1.13.3 Recent developments

- 21.1.13.3.1 Product launches

- 21.1.13.3.2 Deals

- 21.1.14 BRAY INTERNATIONAL

- 21.1.14.1 Business overview

- 21.1.14.2 Products offered

- 21.1.14.3 Recent developments

- 21.1.14.3.1 Product launches

- 21.1.14.3.2 Deals

- 21.1.15 BAKER HUGHES COMPANY

- 21.1.15.1 Business overview

- 21.1.15.2 Products offered

- 21.1.15.3 Recent developments

- 21.1.15.3.1 Product launches

- 21.1.15.3.2 Deals

- 21.1.1 EMERSON ELECTRIC CO.

- 21.2 OTHER KEY PLAYERS

- 21.2.1 CIRCOR INTERNATIONAL, INC.

- 21.2.2 ROTORK

- 21.2.3 WATTS

- 21.2.4 VELAN INC.

- 21.2.5 DANFOSS

- 21.2.6 GEORG FISCHER LTD.

- 21.2.7 SAMSON AG

- 21.2.8 AVK HOLDING A/S

- 21.2.9 KLINGER HOLDING

- 21.2.10 TRILLIUM FLOW TECHNOLOGIES

- 21.3 OTHER PLAYERS

- 21.3.1 EBRO ARMATUREN GEBR. BROER GMBH

- 21.3.2 VALVITALIA SPA

- 21.3.3 GEFA PROCESSTECHNIK GMBH

- 21.3.4 AVCON CONTROLS PVT LTD.

- 21.3.5 FORBES MARSHALL

- 21.3.6 FRENSTAR

- 21.3.7 HAM-LET GROUP

- 21.3.8 DWYER INSTRUMENTS LLC

- 21.3.9 NOVEL VALVES INDIA PVT. LTD.

- 21.3.10 L&T VALVES LIMITED

22 RESEARCH METHODOLOGY

- 22.1 RESEARCH APPROACH

- 22.1.1 SECONDARY AND PRIMARY RESEARCH

- 22.1.2 SECONDARY DATA

- 22.1.2.1 List of major secondary sources

- 22.1.2.2 Key data from secondary sources

- 22.1.3 PRIMARY DATA

- 22.1.3.1 Breakdown of primaries

- 22.1.3.2 Key data from primary sources

- 22.1.3.3 Key primary participants

- 22.1.3.4 Key industry insights

- 22.2 MARKET SIZE ESTIMATION

- 22.2.1 BOTTOM-UP APPROACH

- 22.2.2 TOP-DOWN APPROACH

- 22.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 22.3 MARKET FORECAST APPROACH

- 22.3.1 SUPPLY SIDE

- 22.3.2 DEMAND SIDE

- 22.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 22.5 RESEARCH ASSUMPTIONS

- 22.6 RISK ASSESSMENT

23 APPENDIX

- 23.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 23.2 CUSTOMIZATION OPTIONS

- 23.3 RELATED REPORTS

- 23.4 AUTHOR DETAILS

List of Tables

- TABLE 1 INDUSTRIAL VALVE MARKET: INCLUSION/EXCLUSION DETAILS

- TABLE 2 SUMMARY OF CHANGES MADE IN UPDATED REPORT VERSION

- TABLE 3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- TABLE 4 STRATEGIC FOCUS OF MAJOR COMPANIES IN INDUSTRIAL VALVE MARKET

- TABLE 5 INDUSTRIAL VALVE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 GDP GROWTH RATES (%), BY KEY COUNTRY, 2022-2030

- TABLE 7 ROLE OF PLAYERS IN ECOSYSTEM

- TABLE 8 COMPANY-WISE INDICATIVE SELLING PRICE OF INDUSTRIAL VALVES, BY VALVE TYPE, 2025

- TABLE 9 AVERAGE SELLING PRICE OF INDUSTRIAL VALVES OFFERED BY KEY PLAYERS, BY TYPE, 2025

- TABLE 10 INDICATIVE SELLING PRICE OF INDUSTRIAL VALVES, BY REGION, 2022-2025

- TABLE 11 IMPORT DATA FOR HS CODE 8481-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 12 EXPORT DATA FOR HS CODE 8481-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 13 INDUSTRIAL VALVE MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 14 FISHER JT CONTROL VALVE BOOSTS MAIN CRYOGENIC HEAT EXCHANGER EFFICIENCY AT EUROPEAN LNG PLANT

- TABLE 15 MOGAS SEVERE SERVICE ISOLATION VALVES IMPROVE RELIABILITY IN MINING & MINERAL EXTRACTION OPERATIONS

- TABLE 16 VALVTECHNOLOGIES ZERO-LEAKAGE BALL VALVES IMPROVE HRSG POWER PLANT EFFICIENCY

- TABLE 17 VALVTECHNOLOGIES ZERO-LEAKAGE METAL-SEATED BALL VALVES REDUCE STEAM LEAKAGE IN SPECIALTY PAPER MILL OPERATIONS

- TABLE 18 AVC FAIL-SAFE ESD VALVE ACTUATION SYSTEM IMPROVES PIPELINE SAFETY IN REMOTE ALASKA OPERATIONS

- TABLE 19 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 20 TECHNOLOGY ROADMAP IN INDUSTRIAL VALVE MARKET

- TABLE 21 INDUSTRIAL VALVE MARKET: LIST OF KEY PATENTS, 2022-2025

- TABLE 22 TOP USE CASES AND MARKET POTENTIAL

- TABLE 23 BEST PRACTICES FOLLOWED BY COMPANIES IN INDUSTRIAL VALVE MARKET

- TABLE 24 CASE STUDIES RELATED TO AI IMPLEMENTATION IN INDUSTRIAL VALVE

- TABLE 25 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 26 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 28 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 29 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 30 INDUSTRY VALVE INDUSTRY STANDARDS

- TABLE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR MAJOR INDUSTRIES (%)

- TABLE 32 KEY BUYING CRITERIA FOR MAJOR INDUSTRIES

- TABLE 33 UNMET NEEDS IN INDUSTRIAL VALVE MARKET, BY INDUSTRY

- TABLE 34 INDUSTRIAL VALVE MARKET, BY VALVE TYPE, 2022-2025 (USD MILLION)

- TABLE 35 INDUSTRIAL VALVE MARKET, BY VALVE TYPE, 2026-2032 (USD MILLION)

- TABLE 36 INDUSTRIAL VALVE MARKET, BY VALVE TYPE, 2022-2025 (MILLION UNITS)

- TABLE 37 INDUSTRIAL VALVE MARKET, BY VALVE TYPE, 2026-2032 (MILLION UNITS)

- TABLE 38 ROTARY VALVES: INDUSTRIAL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 39 ROTARY VALVES: INDUSTRIAL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 40 ROTARY VALVES: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 41 ROTARY VALVES: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 42 BALL VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 43 BALL VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 44 BUTTERFLY VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 45 BUTTERFLY VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 46 PLUG VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 47 PLUG VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 48 LINEAR VALVES: INDUSTRIAL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 49 LINEAR VALVES: INDUSTRIAL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 50 LINEAR VALVES: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 51 LINEAR VALVES: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 52 GLOBE VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 53 GLOBE VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 54 DIAPHRAGM VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 55 DIAPHRAGM VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 56 GATE VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 57 GATE VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 58 SAFETY VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 59 SAFETY VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 60 CHECK VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 61 CHECK VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 62 NEEDLE VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 63 NEEDLE VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 64 PINCH VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 65 PINCH VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 66 SOLENOID VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 67 SOLENOID VALVES: INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 68 SAFETY VALVE MARKET, BY VALVE TYPE, 2022-2025 (USD MILLION)

- TABLE 69 SAFETY VALVE MARKET, BY VALVE TYPE, 2026-2032 (USD MILLION)

- TABLE 70 SAFETY VALVE MARKET, BY PRESSURE RANGE, 2022-2025 (USD MILLION)

- TABLE 71 SAFETY VALVE MARKET, BY PRESSURE RANGE, 2026-2032 (USD MILLION)

- TABLE 72 SAFETY VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 73 SAFETY VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 74 SAFETY VALVE MARKET, BY VALVE SIZE, 2022-2025 (USD MILLION)

- TABLE 75 SAFETY VALVE MARKET, BY VALVE SIZE, 2026-2032 (USD MILLION)

- TABLE 76 SAFETY VALVE MARKET, BY VALVE MATERIAL, 2022-2025 (USD MILLION)

- TABLE 77 SAFETY VALVE MARKET, BY VALVE MATERIAL, 2026-2032 (USD MILLION)

- TABLE 78 SAFETY VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 79 SAFETY VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 80 INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2022-2025 (USD MILLION)

- TABLE 81 INDUSTRIAL VALVE MARKET, BY MEDIA TYPE, 2026-2032 (USD MILLION)

- TABLE 82 INDUSTRIAL VALVE MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 83 INDUSTRIAL VALVE MARKET, BY COMPONENT, 2026-2032 (USD MILLION)

- TABLE 84 ACTUATORS: INDUSTRIAL VALVE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 85 ACTUATORS: INDUSTRIAL VALVE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 86 INDUSTRIAL VALVE MARKET, BY FUNCTION, 2022-2025 (USD MILLION)

- TABLE 87 INDUSTRIAL VALVE MARKET, BY FUNCTION, 2026-2032 (USD MILLION)

- TABLE 88 INDUSTRIAL VALVE MARKET, BY MATERIAL, 2022-2025 (USD MILLION)

- TABLE 89 INDUSTRIAL VALVE MARKET, BY MATERIAL, 2026-2032 (USD MILLION)

- TABLE 90 INDUSTRIAL VALVE MARKET, BY VALVE SIZE, 2022-2025 (USD MILLION)

- TABLE 91 INDUSTRIAL VALVE MARKET, BY VALVE SIZE, 2026-2032 (USD MILLION)

- TABLE 92 INDUSTRIAL VALVE MARKET, BY PRESSURE RANGE, 2022-2025 (USD MILLION)

- TABLE 93 INDUSTRIAL VALVE MARKET, BY PRESSURE RANGE, 2026-2032 (USD MILLION)

- TABLE 94 INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 95 INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 96 OIL & GAS: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 97 OIL & GAS: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 98 OIL & GAS: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 99 OIL & GAS: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 100 OIL & GAS: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 101 OIL & GAS: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 102 WATER & WASTEWATER TREATMENT: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 103 WATER & WASTEWATER TREATMENT: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 104 WATER & WASTEWATER TREATMENT: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 105 WATER & WASTEWATER TREATMENT: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 106 WATER & WASTEWATER TREATMENT: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 107 WATER & WASTEWATER TREATMENT: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 108 ENERGY & POWER: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 109 ENERGY & POWER: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 110 ENERGY & POWER: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 111 ENERGY & POWER: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 112 ENERGY & POWER: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 113 ENERGY & POWER: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 114 PHARMACEUTICALS: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 115 PHARMACEUTICALS: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 116 PHARMACEUTICALS: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 117 PHARMACEUTICALS: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 118 PHARMACEUTICALS: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 119 PHARMACEUTICALS: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 120 FOOD & BEVERAGES: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 121 FOOD & BEVERAGES: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 122 FOOD & BEVERAGES: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 123 FOOD & BEVERAGES: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 124 FOOD & BEVERAGES: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 125 FOOD & BEVERAGES: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 126 CHEMICALS: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 127 CHEMICALS: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 128 CHEMICALS: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 129 CHEMICALS: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 130 CHEMICALS: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 131 CHEMICALS: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 132 BUILDING & CONSTRUCTION: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 133 BUILDING & CONSTRUCTION: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 134 BUILDING & CONSTRUCTION: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 135 BUILDING & CONSTRUCTION: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 136 BUILDING & CONSTRUCTION: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 137 BUILDING & CONSTRUCTION: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 138 PAPER & PULP: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 139 PAPER & PULP: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 140 PAPER & PULP: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 141 PAPER & PULP: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 142 PAPER & PULP: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 143 PAPER & PULP: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 144 METALS & MINING: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 145 METALS & MINING: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 146 METALS & MINING: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 147 METALS & MINING: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 148 METALS & MINING: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 149 METALS & MINING: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 150 AGRICULTURE: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 151 AGRICULTURE: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 152 AGRICULTURE: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 153 AGRICULTURE: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 154 AGRICULTURE: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 155 AGRICULTURE: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 156 SEMICONDUCTOR: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 157 SEMICONDUCTOR: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 158 SEMICONDUCTOR: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025 (USD MILLION)

- TABLE 159 SEMICONDUCTOR: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 160 SEMICONDUCTOR: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 161 SEMICONDUCTOR: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 162 OTHER END-USE INDUSTRIES: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 163 OTHER END-USE INDUSTRIES: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 164 OTHER END-USE INDUSTRIES: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2022-2025(USD MILLION)

- TABLE 165 OTHER END-USE INDUSTRIES: INDUSTRIAL VALVE MARKET, BY ROTARY VALVE, 2026-2032 (USD MILLION)

- TABLE 166 OTHER END-USE INDUSTRIES: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2022-2025 (USD MILLION)

- TABLE 167 OTHER END-USE INDUSTRIES: INDUSTRIAL VALVE MARKET, BY LINEAR VALVE, 2026-2032 (USD MILLION)

- TABLE 168 INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 169 INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 170 NORTH AMERICA: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 171 NORTH AMERICA: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 172 NORTH AMERICA: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 173 NORTH AMERICA: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 174 EUROPE: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 175 EUROPE: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 176 EUROPE: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 177 EUROPE: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 178 ASIA PACIFIC: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 179 ASIA PACIFIC: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 180 ASIA PACIFIC: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 181 ASIA PACIFIC: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 182 REST OF THE WORLD: INDUSTRIAL VALVE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 183 REST OF THE WORLD: INDUSTRIAL VALVE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 184 REST OF THE WORLD: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 185 REST OF THE WORLD: INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 186 MIDDLE EAST: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 187 MIDDLE EAST: INDUSTRIAL VALVE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 188 INDUSTRIAL VALVE MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2022-APRIL 2026

- TABLE 189 INDUSTRIAL VALVE MARKET: DEGREE OF COMPETITION, 2025

- TABLE 190 INDUSTRIAL VALVE MARKET: REGION FOOTPRINT

- TABLE 191 INDUSTRIAL VALVE MARKET: VALVE TYPE FOOTPRINT

- TABLE 192 INDUSTRIAL VALVE MARKET: MEDIA TYPE FOOTPRINT

- TABLE 193 INDUSTRIAL VALVE MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 194 INDUSTRIAL VALVE MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 195 INDUSTRIAL VALVE MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES, BY REGION

- TABLE 196 INDUSTRIAL VALVE MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES, BY TYPE

- TABLE 197 INDUSTRIAL VALVE MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES, BY MEDIA TYPE

- TABLE 198 INDUSTRIAL VALVE MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES, BY END-USE INDUSTRY

- TABLE 199 INDUSTRIAL VALVE MARKET: PRODUCT LAUNCHES, JANUARY 2021-APRIL 2026

- TABLE 200 INDUSTRIAL VALVE MARKET: DEALS, JANUARY 2021-APRIL 2026

- TABLE 201 INDUSTRIAL VALVE MARKET: EXPANSIONS, JANUARY 2021-APRIL 2026

- TABLE 202 INDUSTRIAL VALVE MARKET: OTHER DEVELOPMENTS, JANUARY 2021-APRIL 2026

- TABLE 203 EMERSON ELECTRIC CO.: COMPANY OVERVIEW

- TABLE 204 EMERSON ELECTRIC CO.: PRODUCTS OFFERED

- TABLE 205 EMERSON ELECTRIC CO.: PRODUCT LAUNCHES

- TABLE 206 SLB: COMPANY OVERVIEW

- TABLE 207 SLB: PRODUCTS OFFERED

- TABLE 208 SLB: EXPANSIONS

- TABLE 209 FLOWSERVE CORPORATION: COMPANY OVERVIEW

- TABLE 210 FLOWSERVE CORPORATION: PRODUCTS OFFERED

- TABLE 211 FLOWSERVE CORPORATION: PRODUCT LAUNCHES

- TABLE 212 FLOWSERVE CORPORATION: DEALS

- TABLE 213 FLOWSERVE CORPORATION: OTHER DEVELOPMENTS

- TABLE 214 IMI: COMPANY OVERVIEW

- TABLE 215 IMI: PRODUCTS OFFERED

- TABLE 216 IMI: PRODUCT LAUNCHES

- TABLE 217 IMI: EXPANSIONS

- TABLE 218 CRANE HOLDINGS, CO.: COMPANY OVERVIEW

- TABLE 219 CRANE HOLDINGS, CO.: PRODUCTS OFFERED

- TABLE 220 CRANE HOLDINGS, CO.: DEALS

- TABLE 221 CRANE HOLDINGS, CO.: EXPANSIONS

- TABLE 222 VALMET: COMPANY OVERVIEW

- TABLE 223 VALMET: PRODUCTS OFFERED

- TABLE 224 VALMET: PRODUCT LAUNCHES

- TABLE 225 VALMET: DEALS

- TABLE 226 NEWAY VALVE: COMPANY OVERVIEW

- TABLE 227 NEWAY VALVE: PRODUCTS OFFERED

- TABLE 228 NEWAY VALVE: PRODUCT LAUNCHES

- TABLE 229 SPIRAX SARCO LIMITED: COMPANY OVERVIEW

- TABLE 230 SPIRAX SARCO LIMITED: PRODUCTS OFFERED

- TABLE 231 SPIRAX SARCO LIMITED: DEALS

- TABLE 232 KITZ CORPORATION: COMPANY OVERVIEW

- TABLE 233 KITZ CORPORATION: PRODUCTS OFFERED

- TABLE 234 KITZ CORPORATION: PRODUCT LAUNCHES

- TABLE 235 KITZ CORPORATION: DEALS

- TABLE 236 KITZ CORPORATION: EXPANSIONS

- TABLE 237 KSB SE & CO. KGAA: COMPANY OVERVIEW

- TABLE 238 KSB SE & CO. KGAA: PRODUCTS OFFERED

- TABLE 239 KSB SE & CO. KGAA: PRODUCT LAUNCHES

- TABLE 240 KSB SE & CO. KGAA: EXPANSIONS

- TABLE 241 ALFA LAVAL: COMPANY OVERVIEW

- TABLE 242 ALFA LAVAL: PRODUCTS OFFERED

- TABLE 243 ALFA LAVAL: PRODUCT LAUNCHES

- TABLE 244 ALFA LAVAL: DEALS

- TABLE 245 ALFA LAVAL: OTHER DEVELOPMENTS

- TABLE 246 CURTISS-WRIGHT CORPORATION: COMPANY OVERVIEW

- TABLE 247 CURTISS-WRIGHT CORPORATION: PRODUCTS OFFERED

- TABLE 248 CURTISS-WRIGHT CORPORATION: PRODUCT LAUNCHES

- TABLE 249 PARKER HANNIFIN CORP.: COMPANY OVERVIEW

- TABLE 250 PARKER HANNIFIN CORP.: PRODUCTS OFFERED

- TABLE 251 PARKER HANNIFIN CORP.: PRODUCT LAUNCHES

- TABLE 252 PARKER HANNIFIN CORP.: DEALS

- TABLE 253 BRAY INTERNATIONAL: COMPANY OVERVIEW

- TABLE 254 BRAY INTERNATIONAL: PRODUCTS OFFERED

- TABLE 255 BRAY INTERNATIONAL: PRODUCT LAUNCHES

- TABLE 256 BRAY INTERNATIONAL: DEALS

- TABLE 257 BAKER HUGHES COMPANY: COMPANY OVERVIEW

- TABLE 258 BAKER HUGHES COMPANY: PRODUCTS OFFERED

- TABLE 259 BAKER HUGHES COMPANY: PRODUCT LAUNCHES

- TABLE 260 BAKER HUGHES COMPANY: DEALS

- TABLE 261 CIRCOR INTERNATIONAL, INC.: COMPANY OVERVIEW

- TABLE 262 ROTORK: COMPANY OVERVIEW

- TABLE 263 WATTS: COMPANY OVERVIEW

- TABLE 264 VELAN INC.: COMPANY OVERVIEW

- TABLE 265 DANFOSS: COMPANY OVERVIEW

- TABLE 266 GEORG FISCHER LTD.: COMPANY OVERVIEW

- TABLE 267 SAMSON AG: COMPANY OVERVIEW

- TABLE 268 AVK HOLDING A/S: COMPANY OVERVIEW

- TABLE 269 KLINGER HOLDING: COMPANY OVERVIEW

- TABLE 270 TRILLIUM FLOW TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 271 EBRO ARMATUREN GEBR. BROER GMBH: COMPANY OVERVIEW

- TABLE 272 VALVITALIA SPA: COMPANY OVERVIEW

- TABLE 273 GEFA PROCESSTECHNIK GMBH: COMPANY OVERVIEW

- TABLE 274 AVCON CONTROLS PVT LTD.: COMPANY OVERVIEW

- TABLE 275 FORBES MARSHALL: COMPANY OVERVIEW

- TABLE 276 FRENSTAR: COMPANY OVERVIEW

- TABLE 277 HAM-LET GROUP: COMPANY OVERVIEW

- TABLE 278 DWYER INSTRUMENTS LLC: COMPANY OVERVIEW

- TABLE 279 NOVEL VALVES INDIA PVT. LTD.: COMPANY OVERVIEW

- TABLE 280 L&T VALVES LIMITED: COMPANY OVERVIEW

- TABLE 281 INDUSTRIAL VALVE MARKET: RISK ASSESSMENT

List of Figures

- FIGURE 1 INDUSTRIAL VALVE MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 DURATION COVERED

- FIGURE 3 MARKET SCENARIO

- FIGURE 4 GLOBAL INDUSTRIAL VALVE MARKET, 2022-2032

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN INDUSTRIAL VALVE MARKET, 2022-2025

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF INDUSTRIAL VALVE MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN INDUSTRIAL VALVE MARKET, 2026-2032

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN INDUSTRIAL VALVE MARKET, IN TERMS OF VALUE, DURING FORECAST PERIOD

- FIGURE 9 RAPID INDUSTRIALIZATION IN EMERGING ECONOMIES TO DRIVE MARKET

- FIGURE 10 GLOBE VALVES TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 11 LIQUID SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 12 <50 BAR VALVES TO COMMAND LARGEST MARKET SHARE IN 2032

- FIGURE 13 PLASTIC MATERIAL TO REGISTER HIGHEST CAGR DURING STUDY PERIOD

- FIGURE 14 WATER & WASTEWATER TREATMENT INDUSTRY TO DOMINATE MARKET DURING STUDY PERIOD

- FIGURE 15 INDIA TO REGISTER HIGHEST CAGR IN GLOBAL INDUSTRIAL VALVE MARKET DURING STUDY PERIOD

- FIGURE 16 INDUSTRIAL VALVE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 17 IMPACT OF DRIVERS ON INDUSTRIAL VALVE MARKET

- FIGURE 18 IMPACT OF RESTRAINTS ON INDUSTRIAL VALVE MARKET

- FIGURE 19 IMPACT OF OPPORTUNITIES ON INDUSTRIAL VALVE MARKET

- FIGURE 20 IMPACT OF CHALLENGES ON INDUSTRIAL VALVE MARKET

- FIGURE 24 AVERAGE SELLING PRICE OF INDUSTRIAL VALVES OFFERED BY KEY PLAYERS, BY TYPE, 2025

- FIGURE 25 INDICATIVE SELLING PRICE OF INDUSTRIAL VALVES, BY REGION, 2020-2025

- FIGURE 31 DECISION-MAKING FACTORS CONSIDERED WHILE BUYING INDUSTRIAL VALVE

- FIGURE 32 INFLUENCE OF STAKEHOLDERS FROM MAJOR INDUSTRIES ON BUYING PROCESS

- FIGURE 33 KEY BUYING CRITERIA FOR MAJOR INDUSTRIES

- FIGURE 34 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 35 INDUSTRIAL VALVE MARKET, BY VALVE SEALING

- FIGURE 36 INDUSTRIAL VALVE MARKET, BY VALVE TYPE

- FIGURE 37 ROTARY VALVES TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 38 BALL VALVES TO COMMAND LARGEST SHARE IN ROTARY VALVES MARKET DURING FORECAST PERIOD

- FIGURE 39 GLOBE VALVES TO ACCOUNT FOR LARGEST SHARE OF LINEAR VALVES MARKET FROM 2026 TO 2032

- FIGURE 40 SPRING SAFETY VALVES HOLD A SIGNIFICANT SHARE IN SAFETY VALVE MARKET

- FIGURE 41 INDUSTRIAL VALVE MARKET, BY MEDIA TYPE

- FIGURE 42 LIQUID VALVES TO EXHIBIT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 43 INDUSTRIAL VALVE MARKET, BY COMPONENT

- FIGURE 44 ACTUATORS TO COMMAND LARGEST MARKET SHARE IN 2032

- FIGURE 45 INDUSTRIAL VALVE MARKET, BY FUNCTION

- FIGURE 46 ON/OFF VALVES TO DOMINATE MARKET DURING STUDY PERIOD

- FIGURE 47 INDUSTRIAL VALVE MARKET, BY MATERIAL

- FIGURE 48 STEEL TO HOLD LARGEST MARKET SHARE FROM 2026 TO 2032

- FIGURE 49 INDUSTRIAL VALVE MARKET, BY VALVE SIZE

- FIGURE 50 1-6" SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 51 INDUSTRIAL VALVE MARKET, BY PRESSURE RANGE

- FIGURE 52 <50 BAR SEGMENT TO COMMAND LARGEST MARKET SHARE DURING STUDY PERIOD

- FIGURE 53 INDUSTRIAL VALVE MARKET, BY END-USE INDUSTRY

- FIGURE 54 WATER & WASTEWATER TREATMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 55 INDUSTRIAL VALVE MARKET, BY REGION

- FIGURE 56 ASIA PACIFIC TO REGISTER HIGHEST CAGR FROM 2026 TO 2032

- FIGURE 57 NORTH AMERICA: INDUSTRIAL VALVE MARKET SNAPSHOT

- FIGURE 58 EUROPE: INDUSTRIAL VALVE MARKET SNAPSHOT

- FIGURE 59 ASIA PACIFIC: INDUSTRIAL VALVE MARKET SNAPSHOT

- FIGURE 60 REST OF THE WORLD: INDUSTRIAL VALVE MARKET SNAPSHOT

- FIGURE 61 REST OF THE WORLD: INDUSTRIAL VALVE MARKET, 2026-2032

- FIGURE 62 INDUSTRIAL VALVE MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2021-2025

- FIGURE 63 INDUSTRIAL VALVE MARKET SHARE OF KEY PLAYERS, 2025

- FIGURE 64 INDUSTRIAL VALVE MARKET: COMPANY VALUATION

- FIGURE 65 INDUSTRIAL VALVE MARKET: FINANCIAL METRICS (EV/EBITDA)

- FIGURE 66 INDUSTRIAL VALVE MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS FOR KEY PLAYERS

- FIGURE 67 INDUSTRIAL VALVE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 68 INDUSTRIAL VALVE MARKET: COMPANY FOOTPRINT

- FIGURE 69 INDUSTRIAL VALVE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 70 EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

- FIGURE 71 SLB: COMPANY SNAPSHOT

- FIGURE 72 FLOWSERVE CORPORATION: COMPANY SNAPSHOT

- FIGURE 73 IMI: COMPANY SNAPSHOT

- FIGURE 74 CRANE HOLDINGS, CO.: COMPANY SNAPSHOT

- FIGURE 75 VALMET: COMPANY SNAPSHOT

- FIGURE 76 SPIRAX SARCO LIMITED: COMPANY SNAPSHOT

- FIGURE 77 KITZ CORPORATION: COMPANY SNAPSHOT

- FIGURE 78 KSB SE & CO. KGAA: COMPANY SNAPSHOT

- FIGURE 79 ALFA LAVAL: COMPANY SNAPSHOT

- FIGURE 80 CURTISS-WRIGHT CORPORATION: COMPANY SNAPSHOT

- FIGURE 81 PARKER HANNIFIN CORP.: COMPANY SNAPSHOT

- FIGURE 82 BAKER HUGHES COMPANY: COMPANY SNAPSHOT

- FIGURE 83 INDUSTRIAL VALVE MARKET: RESEARCH DESIGN

- FIGURE 84 INDUSTRIAL VALVE MARKET: SECONDARY AND PRIMARY RESEARCH

- FIGURE 85 INDUSTRIAL VALVE MARKET: BOTTOM-UP APPROACH

- FIGURE 86 INDUSTRIAL VALVE MARKET: TOP-DOWN APPROACH

- FIGURE 87 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- FIGURE 88 DATA TRIANGULATION

- FIGURE 89 ASSUMPTIONS OF RESEARCH STUDY