PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998835

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998835

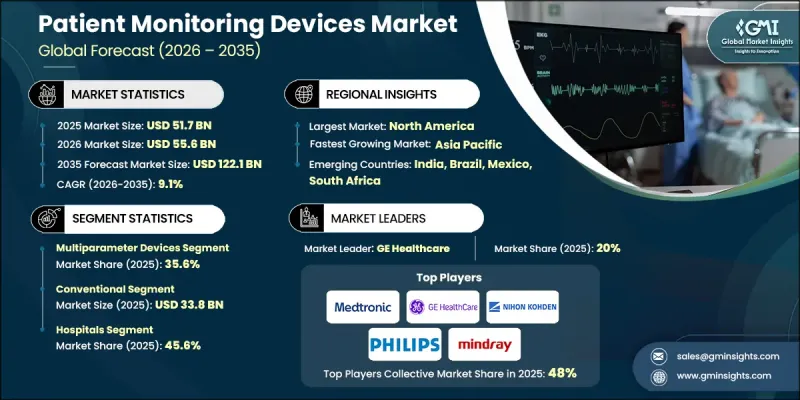

Patient Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Patient Monitoring Devices Market was valued at USD 51.7 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 122.1 billion by 2035.

The market is witnessing strong expansion owing to the rising prevalence of chronic diseases, increasing geriatric populations, technological advancements, and higher healthcare spending in emerging economies. Aging demographics are driving demand, as older populations face a growing incidence of cardiovascular, respiratory, and metabolic conditions that require continuous monitoring. Innovations in patient monitoring devices, particularly the integration of IoT and AI technologies, allow real-time health data collection, predictive analytics, and automated decision-making. These advancements enable clinicians to detect risks early and deliver personalized care. Modern devices now offer wireless connectivity, cloud-based data management, modular designs, and improved portability, enhancing workflow efficiency in critical care, surgical, and home care settings. Advanced monitors provide reliable measurements even under challenging conditions, helping healthcare professionals make faster, accurate clinical decisions while improving patient outcomes globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $51.7 Billion |

| Forecast Value | $122.1 Billion |

| CAGR | 9.1% |

The multiparameter devices segment reached USD 18.4 billion in 2025, representing 35.6%. Multiparameter monitors track multiple vital signs simultaneously, consolidating data on a single platform. They are widely used in ICUs, operating rooms, and emergency care settings, offering customizable settings, high-resolution displays, and modular configurations for tailored patient monitoring.

The conventional segment accounted for USD 33.8 billion in 2025. Conventional bedside monitoring devices are stationary units that track core physiological parameters such as heart rate, blood pressure, oxygen saturation, and temperature. These devices are standard in hospitals for continuous monitoring in ICUs, general wards, and operating rooms, offering reliable and basic vital sign assessment.

U.S. Patient Monitoring Devices Market reached USD 20.2 billion in 2025, driven by the rising prevalence of chronic illnesses, including cardiovascular and respiratory diseases, which necessitate ongoing monitoring. The country's advanced healthcare infrastructure, high surgical volumes, and investment in digital health solutions support the transition from conventional monitors to integrated, wireless systems with centralized monitoring and EHR compatibility, further accelerating market growth.

Key players in the Global Patient Monitoring Devices Market include Medtronic, Koninklijke Philips, GE Healthcare, Fukuda Denshi, Becton Dickinson and Company, Nihon Kohden Corporation, HILLROM & WELCH ALLYN, OSI Systems, Shenzhen Mindray Bio-Medical Electronics, Skanray Technologies, Medion, EPSIMED, Natus Medical, and Cerba Healthcare. Companies in the Global Patient Monitoring Devices Market are focusing on several strategies to strengthen their market presence. They are investing in AI, IoT, and wireless technologies to develop advanced, real-time monitoring solutions. Partnerships with hospitals, healthcare providers, and research institutions help in co-developing devices that meet clinical needs. Expanding distribution networks, enhancing after-sales services, and offering cloud-based data management platforms ensure customer retention. Firms are also focusing on modular, portable, and cost-effective solutions for homecare and remote monitoring. Continuous innovation in multiparameter and wearable devices, along with compliance with regulatory standards, helps maintain competitive advantage and expand global market share.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.2 Research transparency addendum

- 1.7.3 Source attribution framework

- 1.7.4 Quality assurance metrics

- 1.7.1 Quantified market impact analysis

- 1.8 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing disposable income and healthcare expenditure in emerging countries

- 3.2.1.3 Technological advancement in patient monitoring devices

- 3.2.1.4 Growing geriatric population base

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption for AI-powered predictive monitoring tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiac monitoring devices

- 5.2.1 ECG devices

- 5.2.2 Implantable loop recorders

- 5.2.3 Mobile cardiac telemetry monitors

- 5.2.4 Smart wearable ECG patches

- 5.3 Neuromonitoring devices

- 5.3.1 EEG devices

- 5.3.2 Cerebral oximeters

- 5.3.3 Intracranial pressure monitors

- 5.3.4 EMG devices

- 5.4 Respiratory monitoring devices

- 5.4.1 Pulse oximeters

- 5.4.2 Spirometers

- 5.4.3 Capnographs

- 5.4.4 Peak flow meters

- 5.5 Anesthesia monitor

- 5.6 Hemodynamic monitoring devices

- 5.7 Fetal and neonatal monitoring

- 5.8 Multiparameter devices

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Wireless

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Becton Dickinson and Company

- 9.2 Biotronik

- 9.3 EPSIMED

- 9.4 Fukuda Denshi

- 9.5 GE Healthcare

- 9.6 HILLROM & WELCH ALLYN

- 9.7 Koninklijke Philips

- 9.8 Medion

- 9.9 Medtronic

- 9.10 Natus Medical

- 9.11 Nihon Kohden Corporation

- 9.12 OMRON Corporation

- 9.13 OSI Systems

- 9.14 Shenzhen Mindray Bio-Medical Electronics

- 9.15 Skanray Technologies