PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998845

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998845

Nasal Spray Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

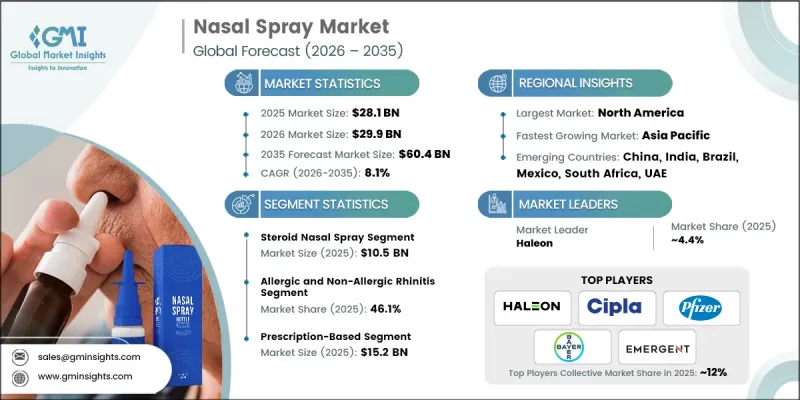

The Global Nasal Spray Market was valued at USD 28.1 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 60.4 billion by 2035.

Market growth is driven by the rising prevalence of chronic respiratory diseases, increasing incidence of allergic and non-allergic rhinitis, and growing demand for non-invasive drug delivery methods. Nasal sprays offer a rapid onset of action, localized drug delivery, and improved patient compliance compared to oral formulations, making them a preferred option for managing sinusitis, allergies, and nasal congestion. The growing shift toward self-care, supported by wider availability of over-the-counter (OTC) products and expanding retail and online pharmacy networks, is further accelerating market growth. Technological advancements such as preservative-free formulations, metered-dose spray devices, and combination therapies are enhancing treatment efficacy and safety, strengthening adoption across both developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $28.1 Billion |

| Forecast Value | $60.4 Billion |

| CAGR | 8.1% |

By product type, the steroid nasal spray segment generated USD 10.5 billion in 2025. Steroid nasal sprays are widely prescribed as first-line therapy for allergic rhinitis and chronic rhinosinusitis due to their strong anti-inflammatory action, long-term safety profile, and low systemic absorption. Products containing fluticasone, mometasone, budesonide, and ciclesonide continue to dominate prescriptions and OTC sales, supported by strong clinical guidelines and physician preference. Ongoing innovation in delivery mechanisms, including improved spray deposition and patient-friendly designs, is further reinforcing the dominance of this segment.

In terms of application, the allergic and non-allergic rhinitis segment held 46.1% share in 2025. The high burden of seasonal and perennial allergies, driven by urbanization, air pollution, and climate-related changes in allergen exposure, continues to fuel demand for effective intranasal therapies. Both prescription and OTC nasal sprays are extensively used for symptom control, including nasal congestion, sneezing, and rhinorrhea. The growing awareness of early treatment and the increasing use of nasal sprays across adult and pediatric populations are expected to sustain strong growth in this segment over the forecast period.

North America Nasal Spray Market held 35% share in 2025. The region's leadership is supported by a high prevalence of allergic rhinitis and chronic sinusitis, a well-established healthcare infrastructure, and strong regulatory frameworks that encourage innovation and generic product approvals. Extensive retail pharmacy networks, rising e-commerce penetration, and increasing adoption of OTC nasal sprays for self-management further strengthen regional demand. Continued product launches, including advanced formulations and expanded therapeutic applications, are expected to maintain North America's leading position through 2034.

Key players operating in the Global Nasal Spray Market include Haleon, Bayer, GlaxoSmithKline, Pfizer, Sanofi, Cipla, Dr. Reddy's Laboratories, Teva Pharmaceutical, Viatris, AstraZeneca, ARS Pharmaceuticals, Emergent BioSolutions, Church & Dwight, and Sun Pharmaceutical, among others. These companies compete through strong brand portfolios, extensive distribution networks, and continuous product innovation across prescription and OTC segments. Companies in the Nasal Spray Market are strengthening their market foothold through a combination of product innovation, portfolio expansion, and strategic collaborations. Leading players are investing heavily in R&D to develop preservative-free formulations, combination therapies, and advanced delivery devices that enhance efficacy and patient adherence. Expansion of OTC product lines and brand repositioning toward self-care solutions are helping companies capture a broader consumer base. Strategic partnerships, licensing agreements, and acquisitions are being used to expand geographic reach and accelerate regulatory approvals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Regional trends

- 2.2.3 Product type trends

- 2.2.4 Application trends

- 2.2.5 Patient type trends

- 2.2.6 Type trends

- 2.2.7 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in prevalence of chronic respiratory diseases and nasal disorders

- 3.2.1.2 Rising demand for non-invasive drug delivery methods

- 3.2.1.3 Shift toward over the counter (OTC) products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of overuse leading to rebound congestion

- 3.2.2.2 Side effects and contraindications with prolonged use

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of nasal delivery for systemic and CNS therapies

- 3.2.3.2 Rising focus on non-invasive pediatric drug delivery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by primary research)

- 3.7 Pipeline and clinical trials landscape

- 3.8 Patent analysis

- 3.9 Future market trends

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Steroid nasal spray

- 5.3 Antihistamine nasal spray

- 5.4 Decongestion nasal spray

- 5.5 Saline nasal spray

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Sinusitis

- 6.3 Allergic and non-allergic rhinitis

- 6.4 Nasal polyps

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Patient Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Adults

- 7.3 Pediatrics

- 7.4 Infants

Chapter 8 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn and Units)

- 8.1 Key trends

- 8.2 Prescription-based

- 8.3 Over-the-counter (OTC)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Retail pharmacies

- 9.3 Hospital pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ARS Pharmaceuticals

- 11.2 AstraZeneca

- 11.3 Aurena Laboratories

- 11.4 Bayer

- 11.5 Church & Dwight

- 11.6 Cipla

- 11.7 COSWELL

- 11.8 Dr. Reddy’s Laboratories

- 11.9 EMERGENT

- 11.10 Haleon

- 11.11 J Pharmaceuticals

- 11.12 Leeford Healthcare

- 11.13 Pfizer

- 11.14 Sanofi

- 11.15 Sun Pharmaceutical

- 11.16 Teva Pharmaceutical

- 11.17 Viatris