PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998849

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998849

Tackifier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

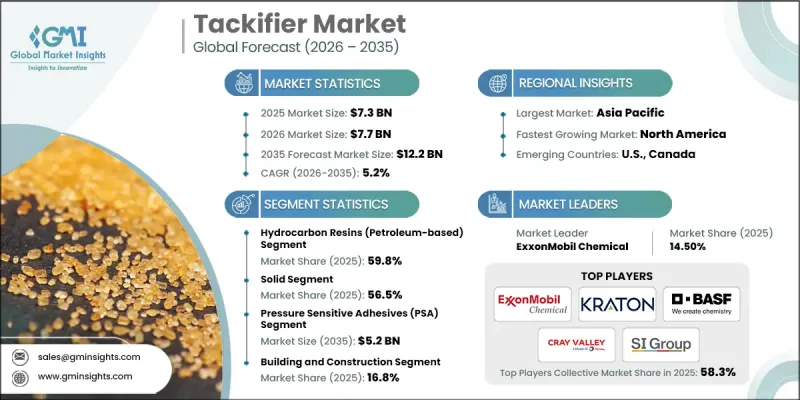

The Global Tackifier Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 12.2 billion by 2035.

Growth in the tackifier market is driven by rising demand from multiple industrial sectors that rely on adhesive technologies to enhance product performance and durability. Tackifiers play an important role in improving adhesion strength, flexibility, and long-term stability within various adhesive formulations used across manufacturing environments. Among end-use sectors, packaging represents the largest share of consumption, followed by building and construction, automotive production, non-woven materials, and woodworking or furniture manufacturing. Increasing focus on environmental sustainability and regulatory compliance is encouraging manufacturers to develop resins with reduced emissions and improved ecological profiles. As environmental regulations become stricter, industries are increasingly adopting low-VOC and bio-based tackifying materials to meet evolving standards. Regionally, Asia Pacific generates the largest share of global revenue due to its extensive manufacturing infrastructure, strong industrial production capacity, and continuous investment in research and development activities. Meanwhile, the European tackifier market is advancing through the development of environmentally responsible high-performance resin technologies. North America is witnessing the fastest growth, supported by expanding industrial activities, increasing urban development, and rising consumption of adhesive products used in packaging and non-woven materials. Although Latin America and the Middle East & Africa represent comparatively smaller portions of the global market, both regions are anticipated to demonstrate consistent and gradual growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.2% |

The rosin resins segment generated USD 2.7 billion in 2025 and remains one of the most important natural resin categories used in adhesive formulations. Rosin-based materials are widely utilized due to their effective bonding properties and adaptability in numerous industrial applications. Several processing techniques are applied to improve the performance characteristics of these materials, including chemical modifications that enhance stability and resistance to oxidation. In addition, various derivative formulations are developed to improve compatibility with different polymer systems and adhesive compositions, allowing manufacturers to achieve improved bonding performance and formulation flexibility across multiple industries.

The solid tackifier segment accounted for 56.5% share in 2025 and is projected to grow at a CAGR of 4.9% between 2026 and 2035. Solid-form tackifiers remain widely preferred because they offer greater stability during storage and handling while maintaining consistent performance during adhesive production. Their physical properties allow manufacturers to control viscosity levels and softening characteristics more effectively during thermal processing. As a result, these materials are commonly incorporated into hot-melt adhesive systems that require dependable bonding strength and predictable processing behavior. Their durability and compatibility with industrial production methods continue to support widespread adoption across multiple manufacturing sectors.

North America Tackifier Market generated USD 1.8 billion in 2025. Strong industrial infrastructure and consistent investment in research and development by major chemical manufacturers support ongoing innovation within the region. Companies are increasingly focusing on developing specialized resin technologies, including hydrogenated and advanced performance formulations designed to improve product stability and durability. However, the regional market remains sensitive to fluctuations in raw material pricing, particularly those associated with petroleum-derived inputs used in resin production. Variability in feedstock costs can influence manufacturing expenses and ultimately affect market dynamics across the region.

Major companies operating in the Global Tackifier Market include BASF SE, Eastman Chemical Company, ExxonMobil Chemical, Kraton Corporation, SI Group Inc., Kolon Industries Inc., ZEON Corporation, Arakawa Chemical Industries Ltd., Yasuhara Chemical Co. Ltd., Lawter Inc., Neville Chemical Company, DRT (Derives Resiniques et Terpeniques), Cray Valley, Foreverest Resources Ltd., and Resin Solutions LLC. Companies competing in the Tackifier Market are strengthening their market presence through continuous innovation, strategic partnerships, and capacity expansion initiatives. Many manufacturers are investing in research and development to create advanced tackifying resins that offer improved bonding performance while meeting evolving environmental standards. The development of bio-based and low-VOC resin technologies has become a key strategic priority as industries shift toward sustainable production practices. Firms are also expanding production facilities and strengthening supply chain networks to support growing global demand for adhesive materials. Strategic collaborations with adhesive manufacturers enable companies to develop customized resin solutions tailored to specific industrial applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Chemistry Type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End User

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Pressure Sensitive Adhesives (PSA)

- 3.2.1.2 Growth in Packaging & E-commerce Industries

- 3.2.1.3 Expansion of Construction & Automotive Sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in Crude Oil & Raw Material Prices

- 3.2.2.2 Stringent Environmental & VOC Regulations

- 3.2.2.3 Availability of Alternative Adhesive Technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing Demand for Bio-Based & Sustainable Resins

- 3.2.3.2 Rapid Industrialization in Asia Pacific

- 3.2.3.3 Advancements in Hydrogenated & Specialty Resins

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By chemistry type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Chemistry Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hydrocarbon Resins (Petroleum-Based)

- 5.2.1 C5 Aliphatic Resins

- 5.2.2 C9 Aromatic Resins

- 5.2.3 C5/C9 Mixed Aliphatic/Aromatic Resins

- 5.2.4 DCPD (Dicyclopentadiene) Resins

- 5.2.5 Hydrogenated Hydrocarbon Resins

- 5.3 Rosin Resins (Natural)

- 5.3.1 Rosin Acids

- 5.3.2 Rosin Esters

- 5.4 Terpene Resins

- 5.4.1 Polyterpene Resins

- 5.4.2 Hydrogenated Terpene Resins

- 5.4.3 Styrenated Terpene Resins

- 5.4.4 Terpene Phenolic Resins

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.3 Liquid

- 6.4 Resin Dispersion

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Pressure Sensitive Adhesives (PSA)

- 7.3 Hot Melt Adhesives (HMA)

- 7.4 Assembly Adhesives

- 7.5 Bookbinding Adhesives

- 7.6 Footwear, Leather & Rubber Adhesives

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Packaging

- 8.3 Building & Construction

- 8.4 Automotive

- 8.5 Non-Wovens

- 8.6 Woodworking & Furniture

- 8.7 Footwear

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arakawa Chemical Industries Ltd.

- 10.2 BASF SE

- 10.3 Cray Valley

- 10.4 DRT (Derives Resiniques et Terpeniques)

- 10.5 Eastman Chemical Company

- 10.6 ExxonMobil Chemical

- 10.7 Foreverest Resources Ltd.

- 10.8 Kolon Industries Inc.

- 10.9 Kraton Corporation

- 10.10 Lawter Inc.

- 10.11 Neville Chemical Company

- 10.12 Resin Solutions LLC

- 10.13 SI Group Inc.

- 10.14 Yasuhara Chemical Co. Ltd.

- 10.15 ZEON Corporation