PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019055

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019055

Aluminum Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

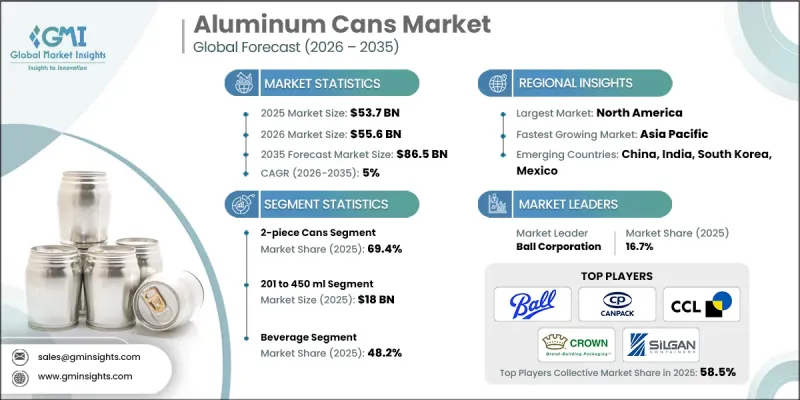

The Global Aluminum Cans Market was valued at USD 53.7 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 86.5 billion in 2035.

The market's growth is driven by increasing demand from carbonated soft drinks and beer, a growing consumer preference for highly recyclable beverage packaging, and the superior recycling efficiency of aluminum within circular packaging systems. The expansion of ready-to-drink and functional beverages fuels demand, alongside beverage companies' focus on lightweight, sustainable, and eco-friendly metal packaging solutions. As beverage consumption rises globally, manufacturers are prioritizing aluminum cans for their ability to preserve carbonation, maintain product quality, and support efficient distribution. The market benefits from both environmental advantages and cost-effectiveness, as recycling aluminum consumes significantly less energy than primary production. Rising sustainability awareness and regulatory support for recyclable packaging further strengthen market adoption across key regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.7 Billion |

| Forecast Value | $86.5 Billion |

| CAGR | 5% |

The 2-piece cans segment held a 69.4% share in 2025, due to their seamless structure, high strength, and efficient production process. These cans are widely adopted for carbonated soft drinks, beer, and ready-to-drink beverages, offering material efficiency and cost advantages for large-scale producers.

The paints & lubricants segment is projected to grow at a CAGR of 8% through 2035. Aluminum cans provide corrosion resistance and safe containment for industrial fluids, including specialty coatings and lubricants, meeting growing industrial production and automotive maintenance needs.

North America Aluminum Cans Market accounted for 34.1% share in 2025. Growth in the region is supported by high demand for canned beverages, including carbonated drinks, beer, and ready-to-drink products. Beverage producers in the U.S., Canada, and Mexico are increasingly favoring aluminum cans for their recyclability and lower environmental impact. Investments in new production facilities and capacity expansions are further enabling manufacturers to meet growing retail and foodservice demand.

Key players operating in the Global Aluminum Cans Market include Ball Corporation, Crown Holdings, CANPACK, Baixicans, Ajanta Bottle, Ceylon Beverage Can, Albott Containers, GZI Industries, Envases Group, Nampak, Orora Packaging, CCL Industries, Shiba Containers, Silgan Containers, Swan Industries, Scan Holdings, Thai Beverage Can, and Toyo Seikan. Companies in the Global Aluminum Cans Market are strengthening their presence through strategic investments in advanced production facilities and capacity expansions to meet rising demand for beverages. Firms are focusing on lightweight, sustainable, and high-recycling-efficiency packaging solutions to appeal to environmentally conscious consumers. Strategic partnerships with beverage brands and e-commerce distributors are enhancing market penetration and product visibility. Companies are also investing in R&D to innovate 2-piece and specialty cans for functional beverages, while leveraging digital printing and customizable packaging for brand differentiation. Expansion into emerging markets and collaborations with industrial and commercial fluid manufacturers further solidify their competitive positioning, ensuring operational efficiency and long-term market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Capacity trends

- 2.2.3 End-user trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strong demand from carbonated soft drinks and beer segments

- 3.2.1.2 Rising consumer preference for recyclable beverage packaging

- 3.2.1.3 High recycling efficiency of aluminum can materials

- 3.2.1.4 Lightweight packaging reducing beverage transportation costs

- 3.2.1.5 Rapid urbanization increasing packaged beverage consumption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Aluminum price volatility affecting can manufacturing costs

- 3.2.2.2 High electricity consumption in aluminum smelting processes

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of energy drink and functional beverage packaging

- 3.2.3.2 Increasing recycled aluminum content in can manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 1-piece cans

- 5.3 2-piece cans

- 5.4 3-piece cans

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Up to 200 ml

- 6.3 201 to 450 ml

- 6.4 451 to 700 ml

- 6.5 701 to 1000 ml

- 6.6 More than 1000 ml

Chapter 7 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Food

- 7.3 Beverage

- 7.4 Personal Care & Cosmetic

- 7.5 Pharmaceutical

- 7.6 Paints & Lubricants

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Ball Corporation

- 9.1.2 Crown Holdings

- 9.1.3 CANPACK

- 9.1.4 Toyo Seikan

- 9.1.5 Envases Group

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Silgan Containers

- 9.2.1.2 CCL Industries

- 9.2.1.3 Orora Packaging

- 9.2.2 Asia Pacific

- 9.2.2.1 Thai Beverage Can

- 9.2.2.2 Ceylon Beverage Can

- 9.2.2.3 Shiba Containers

- 9.2.3 Europe

- 9.2.3.1 Baixicans

- 9.2.3.2 Scan Holdings

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Ajanta Bottle

- 9.3.2 Albott Containers

- 9.3.3 GZI Industries

- 9.3.4 Nampak

- 9.3.5 Swan Industries