PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940641

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940641

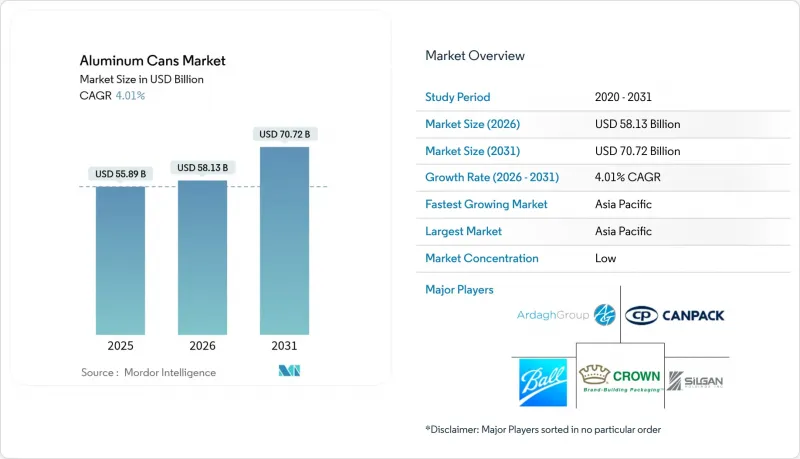

Aluminum Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The global aluminum cans market size in 2026 is estimated at USD 58.13 billion, growing from 2025 value of USD 55.89 billion with 2031 projections showing USD 70.72 billion, growing at 4.01% CAGR over 2026-2031.

Sustained policy pressure favoring circular packaging, rapid adoption by beverage producers shifting away from PET and glass, and capacity additions in high-growth regions collectively underpin this steady expansion. Deposit return systems that guarantee 90% collection by 2029 across the European Union sharply improve recycling economics, prompting brand owners and converters to accelerate investments in closed-loop can manufacturing. Asia Pacific retains its leadership position thanks to rising urban disposable incomes, while North America and Europe leverage premiumization and evolving sustainability mandates to support value growth. Capacity bottlenecks persist, yet recent acquisitions and greenfield builds point to a gradually improving supply balance. At the same time, premium beverage launches, wine-in-can initiatives, and e-commerce demand for dent-resistant formats create additional tailwinds that lift the aluminum cans market well beyond traditional carbonated soft drink applications.

Global Aluminum Cans Market Trends and Insights

High Recyclability and Closed-Loop Recovery Systems

Aluminum retains its metallurgical properties indefinitely, enabling genuine material circularity that plastic and glass cannot match. The Can Manufacturers Institute notes that 75% of all aluminum ever produced remains in active use today, and remelting secondary aluminum consumes 95% less energy than primary smelting. European smelters Constellium, Elval, Novelis, and Speira harmonized alloy specifications in April 2024 to allow beverage cans with up to 100% recycled content, cutting carbon emissions by 2.6 tons of CO2 per ton of metal and lowering operating costs for fillers committed to science-based climate targets. U.S. recycling rates slipped to 43% in 2023, but industry-backed investments aim to lift recovery to 70% by 2030 and 90% by 2050, ensuring long-term feedstock security for can plants. Deposit return programs covering more than 40 billion containers annually in Europe, Canada, and select U.S. states materially raise collection volumes, translating into lower scrap premiums and stronger margins for integrated can makers. These structural advantages collectively add 1.2 percentage points to forecast CAGR, cementing aluminum's reputation as the definitive circular beverage package.

Shift from PET/Glass to Aluminum Amid EPR and Plastics-Tax Mandates

Extended Producer Responsibility schemes fundamentally reshape material cost hierarchies. The United Kingdom's 2025 base EPR fee is set at GBP 266 per tonne for aluminum, far below levies applied to PET, multilayer pouches, or difficult-to-recycle flexibles. California expanded its Container Redemption Value program to wine and spirits in January 2024, immediately widening the addressable beverage can universe by 400 million units a year. Meanwhile, EU rules compel 90% collection of single-use beverage containers by 2029, a benchmark that heavily favors aluminum due to its high post-consumer scrap value. Australia will require 80% recycled content in food-grade aluminum by 2040, again reinforcing demand visibility along the entire Pacific Rim. These converging policies collectively boost aluminum's attractiveness and inject an additional 1.5 percentage point lift into medium-term growth forecasts.

Competition from Flexible PET and Carton Formats

Multilayer cartons and lightweight PET bottles continue to dominate price-sensitive segments, especially for private-label juices, dairy drinks, and shelf-stable water, where brand owners prioritize unit cost over recyclability. New glycol-modification techniques have extended PET shelf life for carbonation and sensitive nutrient blends, narrowing aluminum's functional advantage. In developing economies, consumer willingness to pay sustainability premiums remains low, restraining penetration in commoditized categories. However, upcoming bans on non-recyclable plastic formats across the EU and Canada, alongside hard-to-reach EPR thresholds, will gradually erode the competitive edge of flexibles. Net effect is a temporary 0.8% drag on the aluminum cans market CAGR from 2025-2027.

Other drivers and restraints analyzed in the detailed report include:

- Boom in RTD, Craft, and Functional Beverages

- Rapid Growth of Can-Friendly Wine and Spirits Packaging

- Price and Supply Volatility of Primary Aluminum

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard 330-mL and 355-mL bodies retained 55.38% of 2025 revenue, a share underpinned by filling-line compatibility, the highest line speeds, and optimal pallet density. The segment also capitalizes on broad end-user familiarity, which reduces changeover costs for global bottlers. Nevertheless, sleek cans, typified by 250-mL and 310-mL footprints, are advancing swiftly at a 4.06% CAGR thanks to their premium visual ratio and enhanced billboard effect in crowded retail aisles. Beverage formulators serving functional, low-calorie, and alcohol-ready-to-drink segments prize the elongated profile for differentiated shelf blocking and cold-box visibility. Ball's Dynamark variable-graphics platform lets marketers design limited-run art across both standard and sleek formats without line-stopovers, trimming inventory risk and fostering campaign agility. As printing technology lowers per-unit cost, sleek cans should secure incremental penetration in higher-margin SKUs. Specialty shapes and tactile embossing remain nascent but reflect ongoing innovation that further enriches consumer experience. Altogether, the aluminum cans market expects continued coexistence of standard mass-volume formats and sleek premium variants, with the latter responsible for outsized revenue gains relative to capacity installed.

Standard bodies still benefit from superior logistics economics: a 24-count case of 355-mL cans weighs 20% less than an equivalent glass pack, cutting freight emissions and reducing shelf-stack injuries for retailers. Their thicker gauge, tooled since the 1990s, affords converters a stable margin capture even at high metal premiums. Yet brand owners are willing to absorb a slight cost uplift for sleek cans targeting lifestyle positioning where visual disruption and perceived health cues trump per-ounce value. By 2030, sleek units are likely to reach double-digit market share, adding breadth to packaging portfolios while maintaining backward compatibility with legacy line equipment. As such, type diversification reinforces the broader aluminum cans market's resilience and keeps switching costs low for bottlers contemplating entry into niche beverage sub-categories.

Beverages claimed 48.35% of global revenues in 2025, mirroring a century-long symbiosis between carbonated drinks and lightweight metal containers. Carbonated soft drinks, energy shots, and sports hydration products remain workhorse volumes that secure economies of scale for can-sheet rolling mills. Sustained double-digit launches of spiked seltzers, CBD-infused tonics, and nitro-coffee further widen beverage category breadth, allowing can lines to run at near-full utilization even during off-season contractions for mainstream sodas. Meanwhile, aerosol fillings from deodorants to cooking sprays are forecast to post a 5.21% CAGR, marking them the fastest mover within the aluminum cans market. Brand owners appreciate aluminum's corrosion resistance for formulations containing oils, propellants, or alcohols that degrade tinplate alternatives. Enhanced wall ironing processes enable pressure ratings up to 18 bar, paving the way for mousse, paint, and whipped-cream formats as well.

Pet food and human canned foods hold a smaller slice but deliver stable year-round demand anchored in inventory rotation and emergency-stock purchasing behaviors. Silgan Holdings witnessed double-digit pet food can revenue growth in 2024, illustrating premium pet nutrition's alignment with metal's oxygen-barrier features. Pharmaceutical and nutraceutical applications occupy an emerging frontier, leveraging tamper-evidence and precise metering features of small-volume aluminum vials. Collectively, end-user diversification further insulates the aluminum cans market against single-category downturns while providing multiple growth vectors that absorb manufacturing overhead and accelerate asset payback.

The Aluminum Cans Market Report is Segmented by Type (Standard, Sleek, Slim, and More), End-User Industry (Beverage [Alcoholic Beverages, and Non-Alcoholic Beverages], Food [Canned Food, and Pet Food], Aerosol, and More), Structure (2-Piece, and 3-Piece), Capacity (Up To 250 Ml, 251-500 Ml, and Above 500 Ml), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific contributes 40.74% of global sales, and its aluminum cans market size is projected to advance 5.52% annually to 2031, underwritten by rising middle-class disposable incomes, urban convenience culture, and authoritative restrictions on single-use plastics in China, India, and Japan. China retains pole position with in-house rolling capacity and a vibrant domestic beverage sector that collectively eclipses import dependence. Hindalco's USD 10 billion expansion amplifies India's domestic metal supply in anticipation of can adoption by local cola, energy drink, and alcopop producers. Japan's mature beverage environment spurs innovation in premium tea and craft coffee cans, aided by Asahi Group's net-zero pledges driving procurement switch-overs. Southeast Asia is equally dynamic; NS-Siam United Steel allocated USD 58.5 million to bolster tinplate output, yet concurrently partners with foreign can-sheet suppliers, signaling blended development paths for both ferrous and aluminum supply chains.

North America ranks second in absolute size, though its unit volumes plateau. Instead, the region focuses on trading up to sleek, slim, and specialty thermochromic cans that fetch higher margins. Ball shipped roughly 49 billion containers in 2023, representing 36% regional aluminum cans market share and delivering significant recycled content progress as reclamation systems scale. U.S. state-level container deposit expansions plus Canada's EPR rollouts strengthen secondary scrap supply, raising recycled content in can body sheet to record highs and lowering metal purchase costs for converters.

Europe, while mature, leans heavily on regulatory levers to accelerate modal shift from PET to aluminum. With the EU's 90% collection target looming, brand owners pre-pay for compliance by booking multi-year aluminum can supply contracts that stabilize converter order books. The United Kingdom's upcoming deposit return program will funnel 14 billion metal containers into closed-loop paths yearly, solidifying feedstock security. Germany and France aggressively promote wine-in-can pilots, expanding beyond beer's established foothold. These factors allow European producers to deploy new capacity while raising line speeds and integrating on-site renewable energy, ensuring that the aluminum cans market in the bloc grows in value even where volumes edge upward modestly.

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- Silgan Holdings Inc.

- CAN-PACK S.A.

- Novelis Inc.

- ORG Technology Co. Ltd.

- Toyo Seikan Group Holdings Ltd.

- CPMC Holdings Limited

- Baosteel Packaging Co. Ltd.

- Envases Universales

- Tecnocap Group

- CCL Container Inc.

- Massilly Holding S.A.S

- Nampak Ltd.

- Saudi Arabia Packaging Industry (SAPIN)

- Can-One Berhad

- Alltub Deutschland GmbH

- Baofeng Group Co. Ltd.

- Trivium Packaging B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High recyclability and closed-loop recovery systems

- 4.2.2 Shift from PET/glass to aluminum amid EPR and plastics-tax mandates

- 4.2.3 Boom in RTD, craft and functional beverages

- 4.2.4 Rapid growth of can-friendly wine and spirits packaging (under-reported)

- 4.2.5 E-commerce's need for dent-resistant primary packaging (under-reported)

- 4.3 Market Restraints

- 4.3.1 Competition from flexible PET and carton formats

- 4.3.2 Price and supply volatility of primary aluminum

- 4.3.3 Regional can-making capacity bottlenecks (under-reported)

- 4.3.4 Rising Scope-3 decarbonization compliance costs (under-reported)

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Standard

- 5.1.2 Sleek

- 5.1.3 Slim

- 5.1.4 Other Types

- 5.2 By End-user Industry

- 5.2.1 Beverage

- 5.2.1.1 Alcoholic Beverages

- 5.2.1.2 Non-alcoholic Beverages

- 5.2.2 Food

- 5.2.2.1 Canned Food

- 5.2.2.2 Pet Food (Wet and Treats)

- 5.2.3 Aerosol

- 5.2.4 Other End-user Industries

- 5.2.1 Beverage

- 5.3 By Structure

- 5.3.1 2-piece

- 5.3.2 3-piece

- 5.4 By Capacity

- 5.4.1 Up to 250 ml

- 5.4.2 251 - 500 ml

- 5.4.3 More than 500 ml

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ball Corporation

- 6.4.2 Crown Holdings Inc.

- 6.4.3 Ardagh Group S.A.

- 6.4.4 Silgan Holdings Inc.

- 6.4.5 CAN-PACK S.A.

- 6.4.6 Novelis Inc.

- 6.4.7 ORG Technology Co. Ltd.

- 6.4.8 Toyo Seikan Group Holdings Ltd.

- 6.4.9 CPMC Holdings Limited

- 6.4.10 Baosteel Packaging Co. Ltd.

- 6.4.11 Envases Universales

- 6.4.12 Tecnocap Group

- 6.4.13 CCL Container Inc.

- 6.4.14 Massilly Holding S.A.S

- 6.4.15 Nampak Ltd.

- 6.4.16 Saudi Arabia Packaging Industry (SAPIN)

- 6.4.17 Can-One Berhad

- 6.4.18 Alltub Deutschland GmbH

- 6.4.19 Baofeng Group Co. Ltd.

- 6.4.20 Trivium Packaging B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment