PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019057

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019057

Europe Car Audio Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

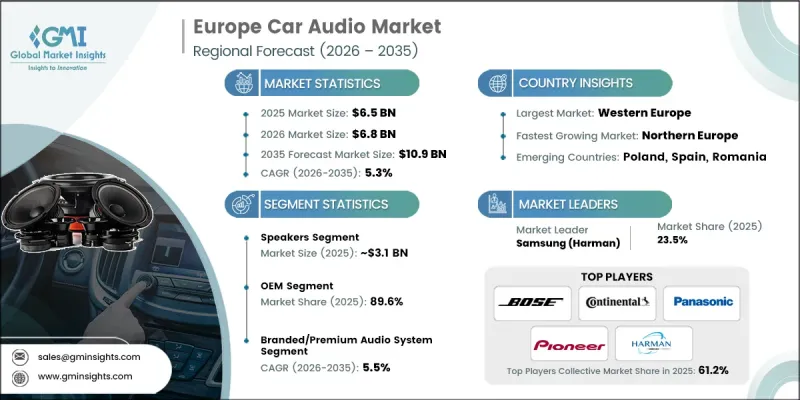

Europe Car Audio Market was valued at USD 6.5 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 10.9 billion by 2035.

Growth in the Europe car audio industry is shaped by the increasing focus of automotive manufacturers on enhancing in-vehicle entertainment as a key differentiator. Automakers are strengthening collaborations with audio technology providers to deliver advanced sound systems that align with evolving consumer expectations. Changing vehicle preferences, particularly the rising inclination toward mid-sized and larger passenger vehicles, are also influencing demand for enhanced audio systems. These vehicle categories account for a substantial portion of new registrations in the region, supporting higher integration of sophisticated audio components. Technological innovation is further transforming the in-car audio experience, with intelligent systems capable of adapting to user behavior and environmental conditions. Features powered by artificial intelligence are enabling personalized sound settings, improving comfort and usability. As consumer demand shifts toward immersive and high-quality audio experiences, the Europe car audio market is expected to witness sustained growth, supported by continuous advancements in automotive technology and evolving mobility trends.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 5.3% |

The speakers segment held a 48% share, generating USD 3.1 billion in 2025. Speakers play a central role in delivering sound output within vehicles, making them a critical component of any audio system. Their importance is underscored by their function as the final output device, directly influencing overall sound quality. With increasing demand for enhanced audio performance, manufacturers are focusing on improving speaker design and acoustic efficiency, which continues to drive strong demand across vehicle categories.

The branded and premium audio system segment held a 61.1% share in 2025 and is expected to grow at the fastest CAGR of 5.5% from 2026 to 2035. This growth is driven by evolving consumer preferences, particularly among younger and technology-oriented buyers who prioritize superior sound quality and immersive experiences. Automotive manufacturers are increasingly integrating high-end audio systems as part of their standard or optional offerings, further supporting segment expansion. Continuous innovation in sound engineering and advanced audio features is reinforcing the segment's leading position in the market.

Germany Car Audio Market captured USD 1.2 billion in 2025 and is expected to grow at a CAGR of 4% between 2026 and 2035. The country's strong automotive manufacturing base and its leadership in vehicle production contribute substantially to overall regional demand. A well-established presence in the premium vehicle segment and the ongoing transition toward electrified mobility are further strengthening the adoption of advanced car audio systems.

Key players operating in the Europe Car Audio Market include Alpine, Bang & Olufsen, Blaupunkt, Bose, Continental, Focal, Panasonic, Pioneer, Samsung (Harman), and Sony. Companies in the Europe Car Audio Market are focusing on strengthening partnerships with automotive manufacturers to integrate advanced audio technologies directly into vehicles. They are investing heavily in research and development to enhance sound quality, connectivity, and intelligent audio features. Expanding product portfolios with premium and customized solutions is a key strategy to attract diverse consumer segments. Firms are also leveraging digital technologies and software integration to deliver personalized in-car audio experiences. Geographic expansion and brand positioning in the premium segment are helping companies increase market visibility, while continuous innovation and competitive pricing strategies are enabling them to maintain a strong foothold in a highly competitive environment.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Make

- 2.2.5 Vehicle

- 2.2.6 Vehicle Class

- 2.2.7 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for premium in-car entertainment

- 3.2.1.2 Growth of connected car technologies and smartphone integration

- 3.2.1.3 Increasing vehicle production and sales across Europe

- 3.2.1.4 Expansion of electric vehicle market driving audio innovation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of premium branded audio systems

- 3.2.2.2 Complexity of integration with advanced vehicle electronics

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for personalized and immersive audio experiences

- 3.2.3.2 Integration of voice assistants and AI-powered audio control

- 3.2.3.3 Retrofit solutions for electric and hybrid vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Western Europe

- 3.4.1.1 Germany - Federal Network Agency

- 3.4.1.2 France - Autorite de Regulation des Communications Electroniques et des Postes

- 3.4.2 Eastern Europe

- 3.4.2.1 Poland - Office of Electronic Communications

- 3.4.2.2 Czech Republic - Czech Telecommunication Office

- 3.4.3 Northern Europe

- 3.4.3.1 Sweden - Swedish Post and Telecom Authority

- 3.4.3.2 Denmark - Danish Business Authority

- 3.4.4 Southern Europe

- 3.4.4.1 Italy - Italian Communications Regulatory Authority

- 3.4.4.2 Spain - National Commission on Markets and Competition

- 3.4.1 Western Europe

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Digital signal processing (DSP)

- 3.8.1.2 Integration with smartphone platforms

- 3.8.1.3 Multi-channel surround sound systems

- 3.8.2 Emerging technologies

- 3.8.2.1 Artificial intelligence-based adaptive sound optimization

- 3.8.2.2 Voice-controlled audio systems integrated with virtual assistants

- 3.8.2.3 3D spatial and immersive audio technologies

- 3.8.1 Current technologies

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Cost breakdown analysis

- 3.15 Impact of electric & autonomous vehicles

- 3.15.1 Audio system design adaptations for electric vehicles

- 3.15.2 Noise compensation and active sound design technologies

- 3.15.3 Power efficiency and lightweight component considerations

- 3.15.4 Vehicle cabin acoustics and vibration control in EVs/AVs

- 3.16 Customer demographics & psychographics

- 3.16.1 Age-based segmentation and generational trends

- 3.16.2 Income-level segmentation and purchasing power

- 3.16.3 Lifestyle and mobility preferences affecting in-car audio adoption

- 3.16.4 Audio quality expectations and brand loyalty patterns

- 3.17 Case studies

- 3.18 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.18.1 Base Case - key macro & industry variables driving CAGR

- 3.18.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.18.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Head Units/Receivers

- 5.3 Speakers

- 5.4 Amplifiers

- 5.5 Subwoofers

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital/Smart

- 6.4 Integrated Infotainment

Chapter 7 Market Estimates & Forecast, By Make, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Branded/Premium audio system

- 7.3 Non-branded audio system

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

Chapter 9 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 Economy

- 9.3 Mid-Range

- 9.4 Premium/Luxury

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 11.1 Key trends

- 11.2 Western Europe

- 11.2.1 Germany

- 11.2.2 Austria

- 11.2.3 France

- 11.2.4 Switzerland

- 11.2.5 Belgium

- 11.2.6 Luxembourg

- 11.2.7 Netherlands

- 11.2.8 Portugal

- 11.3 Eastern Europe

- 11.3.1 Poland

- 11.3.2 Romania

- 11.3.3 Czechia

- 11.3.4 Slovenia

- 11.3.5 Bulgaria

- 11.3.6 Slovakia

- 11.3.7 Hungary

- 11.4 Northern Europe

- 11.4.1 UK

- 11.4.2 Denmark

- 11.4.3 Sweden

- 11.4.4 Finland

- 11.4.5 Norway

- 11.5 Southern Europe

- 11.5.1 Italy

- 11.5.2 Spain

- 11.5.3 Greece

- 11.5.4 Albania

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Samsung (Harman)

- 12.1.2 Bose

- 12.1.3 Pioneer

- 12.1.4 Sony

- 12.1.5 Panasonic

- 12.1.6 Alpine

- 12.1.7 Bang & Olufsen

- 12.1.8 Blaupunkt

- 12.1.9 Kenwood

- 12.1.10 Continental

- 12.2 Regional players

- 12.2.1 Focal

- 12.2.2 Audison

- 12.2.3 Ground Zero

- 12.2.4 Hertz Audio

- 12.2.5 Eton

- 12.2.6 Rainbow

- 12.2.7 Zenec

- 12.3 Emerging players

- 12.3.1 Meridian Audio

- 12.3.2 Sonos

- 12.3.3 Sennheiser