PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038427

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038427

Automotive Tuner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

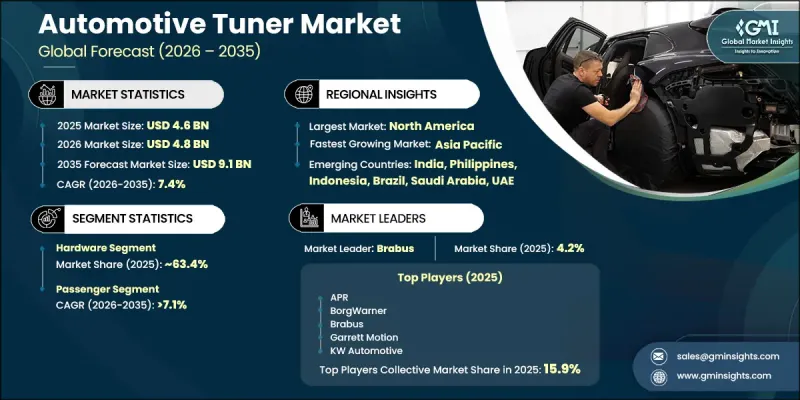

The Global Automotive Tuner Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 9.1 billion in 2035.

The market growth is fueled by the expansion of the automotive aftermarket ecosystem and increasing consumer preference for vehicle personalization and enhanced performance. Rising disposable income, particularly among younger vehicle owners, is also contributing to the stronger adoption of tuning solutions. The growing influence of motorsport culture and performance-driven driving habits is further accelerating demand. The industry has evolved from traditional mechanical upgrades to advanced electronic and software-based tuning systems, including ECU recalibration, performance enhancement modules, and integrated control solutions that improve engine output, torque delivery, and fuel efficiency. Increasing digitalization in automotive systems is also supporting the transition toward intelligent tuning solutions that offer precise performance optimization.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 7.4% |

Stringent emission regulations and evolving compliance requirements are reshaping the automotive tuner landscape. While regulatory frameworks have restricted certain modification practices, they have also driven innovation in compliant tuning technologies that improve engine efficiency within approved emission limits. Modern tuning solutions are increasingly designed to balance performance enhancement with fuel economy and environmental standards. Growing consumer demand for customized driving experiences is further supporting market expansion, with vehicle owners seeking tailored performance adjustments for different use cases such as off-road driving, competitive racing, and long-distance efficiency. The increasing availability of advanced tuning software and connected vehicle platforms is also enhancing accessibility and precision in performance modification, strengthening overall market adoption.

The hardware segment accounted for 63.4% share in 2025 and is expected to grow at a CAGR of 7.7% through 2035. This segment leads the automotive tuner market due to its strong reliance on physical performance enhancement components such as turbocharging systems, exhaust upgrades, air intake assemblies, suspension modifications, and cooling systems. These upgrades deliver immediate improvements in power output, torque, and handling dynamics, making them highly preferred among automotive enthusiasts. Hardware-based tuning continues to play a key role in motorsports and high-performance applications where mechanical enhancements are essential for achieving superior vehicle performance beyond software adjustments.

The passenger vehicle segment held a 66.6% share in 2025 and is projected to grow at a CAGR of 7.1% from 2026 to 2035. This dominance is driven by the large global passenger vehicle base and strong consumer interest in personalization and performance upgrades. Individual vehicle owners increasingly invest in enhancements such as engine tuning, exhaust modifications, and suspension improvements to achieve better driving dynamics and aesthetic appeal. The availability of cost-effective and easy-to-install tuning solutions has further broadened consumer access, supporting sustained growth in this segment.

U.S. Automotive Tuner Market accounted for 83.6% share in 2025 and generated USD 1.4 billion. Market expansion in the country is supported by strong demand for high-performance vehicle modifications and personalization among automotive enthusiasts. A well-established aftermarket ecosystem, high disposable income levels, and a large base of performance-oriented vehicles continue to drive adoption. Technological advancements in ECU tuning, cloud-enabled performance systems, and AI-based optimization tools are further accelerating market development and strengthening the tuning industry landscape.

Prominent players operating in the Global Automotive Tuner Industry include BorgWarner, Garrett Motion, KW Automotive, HKS, HP Tuners, COBB Tuning, Revo Technik, Brabus, Turbosmart, and APR. Key strategies adopted by companies in the automotive tuner market focus on expanding product portfolios with advanced ECU tuning solutions and high-performance hardware components. Firms are investing in digital tuning platforms, cloud-based calibration tools, and AI-enabled performance optimization technologies to improve precision and user experience. Strategic partnerships with automotive OEMs and aftermarket distributors are strengthening market reach. Companies are also emphasizing regulatory-compliant tuning solutions that balance performance and emission standards. Expansion into connected vehicle ecosystems and subscription-based tuning services is enhancing recurring revenue streams. Additionally, firms are increasing R&D investment, focusing on motorsport collaborations, and targeting emerging enthusiast communities to strengthen brand presence and competitive positioning.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in demand for vehicle personalization and performance enhancement

- 3.2.1.2 Rise in adoption of advanced ECU remapping and software-based tuning solutions

- 3.2.1.3 Increase in global automotive enthusiast culture and motorsports influence

- 3.2.1.4 Growth in overall vehicle ownership and expanding automotive parc

- 3.2.1.5 Rise in demand for electric and hybrid vehicle performance optimization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent emission regulations limiting performance modification scope

- 3.2.2.2 Growing concerns over vehicle warranty loss due to tuning activities

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in demand for cloud-based and remote automotive tuning solutions

- 3.2.3.2 Increase in penetration of electric vehicles creating new tuning avenues

- 3.2.3.3 Growth in automotive customization trends across emerging economies

- 3.2.3.4 Surge in partnerships between OEMs and tuning solution providers

- 3.2.3.5 Advancement in AI-driven and data-based vehicle performance optimization technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory guideline

- 3.6.1 North America

- 3.6.1.1 U.S.: Clean Air Act (CAA)

- 3.6.1.2 Canada: Canadian Environmental Protection Act (CEPA)

- 3.6.2 Europe

- 3.6.2.1 Germany: Euro 6/Euro 7 Standards (EU Type Approval Framework)

- 3.6.2.2 UK: Road Vehicles (Construction and Use) Regulations 1986

- 3.6.2.3 France: Code de la Route

- 3.6.2.4 Italy: Codice della Strada

- 3.6.3 Asia Pacific

- 3.6.3.1 China: China VI Emission Standards

- 3.6.3.2 India: Central Motor Vehicles Rules (CMVR) / Bharat Stage VI

- 3.6.3.3 Japan: Road Vehicles Act

- 3.6.3.4 Australia: Australian Design Rules (ADR)

- 3.6.4 Latin America

- 3.6.4.1 Brazil: PROCONVE

- 3.6.4.2 Mexico: NOM-042-SEMARNAT

- 3.6.4.3 Argentina: National Emissions Framework

- 3.6.5 MEA

- 3.6.5.1 UAE: ESMA Vehicle Regulations

- 3.6.5.2 Saudi Arabia: SASO Vehicle Standards

- 3.6.5.3 South Africa: National Environmental Management: Air Quality Act (NEM:AQA)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent Landscape (Driven by Primary Research)

- 3.10 Trade Data Analysis (Based on Paid Database)

- 3.10.1 Import/Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Production Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.14.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Electric

- 7.4.1 PHEV

- 7.4.2 HEV

- 7.4.3 FCEV

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 AEM Performance Electronics

- 10.1.2 Akrapovi d.d.

- 10.1.3 BorgWarner.

- 10.1.4 Borla Performance Industries

- 10.1.5 COBB Tuning

- 10.1.6 Garrett Motion Inc.

- 10.1.7 HKS Co., Ltd.

- 10.1.8 HP Tuners

- 10.1.9 K&N Engineering

- 10.1.10 MagnaFlow

- 10.2 Regional Players

- 10.2.1 APR

- 10.2.2 Banks Power

- 10.2.3 Dinan Engineering

- 10.2.4 Flowmaster

- 10.2.5 Hennessey Performance Engineering

- 10.2.6 Milltek Sport Limited

- 10.2.7 Revo Technik

- 10.2.8 SCT Performance

- 10.2.9 Superchips LIMITED

- 10.2.10 Turbosmart

- 10.3 Emerging Players

- 10.3.1 AWE Tuning

- 10.3.2 Edge Vehicles LLC

- 10.3.3 EFI Live Limited

- 10.3.4 Integrated Engineering

- 10.3.5 Unitronic Corporation