PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019065

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019065

In-Vitro Diagnostics Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

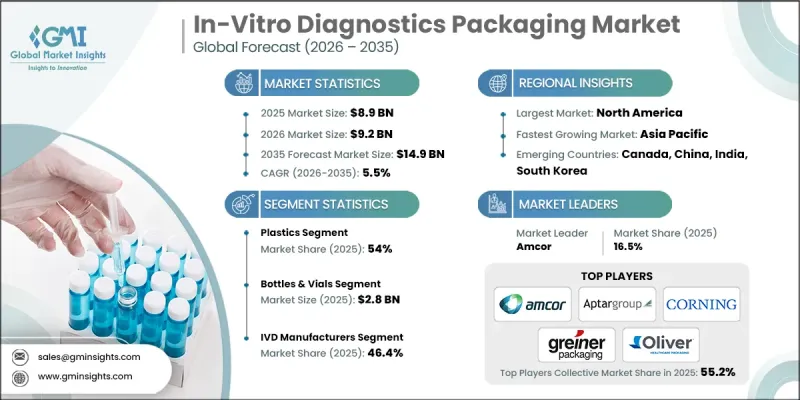

The Global In-Vitro Diagnostics Packaging Market was valued at USD 8.9 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 14.9 billion in 2035.

Rising incidences of infectious diseases, growing home-based diagnostic solutions, and stricter regulatory standards for sterile and contamination-resistant packaging are key growth drivers. The market is also fueled by the rising need for cold chain-compatible packaging to maintain the stability of sensitive biological samples. Sustainability is emerging as a major trend, with manufacturers increasingly adopting recyclable, bio-based, and single-material packaging solutions to reduce environmental impact. Automation and high-speed packaging systems are reshaping operations, improving efficiency, and reducing human error, while portable and user-friendly designs support the growing adoption of decentralized and point-of-care testing across healthcare and research sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.9 Billion |

| Forecast Value | $14.9 Billion |

| CAGR | 5.5% |

The glass packaging is expected to grow at a CAGR of 6.2% during 2026-2035, owing due to its chemical inertness, thermal stability, and high purity, making it ideal for sensitive reagents and biological materials. Glass vials, ampoules, and containers are preferred in specialized diagnostic applications requiring minimal interaction between the material and its contents, supporting precision in pharmaceutical and laboratory testing.

The bottles & vials segment reached USD 2.8 billion in 2025. These formats are widely used for storing diagnostic reagents, culture media, and biological samples. Their compatibility with sterilization processes, automated dispensing systems, and cold chain requirements makes them essential in laboratories, hospitals, and centralized testing centers. Secure sealing, consistent sizing, and high chemical resistance ensure regulatory compliance and reliable diagnostic outcomes.

North America In-Vitro Diagnostics Packaging Market held a 35.1% share in 2025. The region's growth is supported by strict regulations on sterility, contamination control, and cold chain management. Rising demand for rapid and point-of-care testing in healthcare and research sectors accelerates the adoption of advanced packaging solutions. Investments in scalable, automated, and eco-friendly packaging systems, along with smart packaging integration for temperature monitoring and supply chain traceability, reinforce North America's leadership in the market.

Leading players in the Global In-Vitro Diagnostics Packaging Market include Amcor Limited, Corning Incorporated, Aptargroup Incorporated, Greiner Holding AG, VWR International, LLC., Focus Technology Co., Ltd., YuHuan KangJia, Labtech Disposables, Peacock Industries, Oliver, Abdos Labtech Private Limited, AdvaCare Pharma, ACADEMY MEDICAL INSTRUMENTS Limited Company, Ajosha Bio Teknik Pvt. Ltd., Amrit Scientific Ind. Private Limited and Zhuhai Ideal Biotech Co., Ltd. Companies in the In-Vitro Diagnostics Packaging Market are focusing on several key strategies to strengthen their market position. They are investing in research and development to design sustainable, recyclable, and bio-based packaging materials that comply with evolving environmental regulations. Expansion of automated and high-speed packaging solutions improves production efficiency and reduces human error. Firms enhance product portfolios with portable, user-friendly formats for point-of-care and home diagnostics. Strategic partnerships with healthcare providers and diagnostic companies enable broader market reach. Adoption of smart packaging for cold chain monitoring and traceability strengthens reliability and customer trust. Companies also leverage digital marketing, supply chain integration, and global distribution networks to increase accessibility and maintain a competitive advantage in this rapidly growing market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Packaging product type trends

- 2.2.2 Material type trends

- 2.2.3 IVD product category trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infectious disease diagnostics volume globally

- 3.2.1.2 Growth in point-of-care testing kits demand

- 3.2.1.3 Cold chain logistics expansion for temperature-sensitive IVDs

- 3.2.1.4 Stringent regulatory requirements for sterile packaging

- 3.2.1.5 Increasing home-based diagnostic testing adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions in medical-grade plastics

- 3.2.2.2 Complex validation requirements for sterile packaging

- 3.2.3 Market opportunities

- 3.2.3.1 Sustainable and recyclable medical packaging innovations

- 3.2.3.2 Smart packaging integration for temperature monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Packaging Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Bottles & vials

- 5.3 Tubes & microtubes

- 5.4 Pouches & bags

- 5.5 Trays & blisters

- 5.6 Test cartridges & cassettes

- 5.7 Cartons & boxes

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Plastics

- 6.3 Glass

- 6.4 Paper & paperboard

- 6.5 Foil laminates

Chapter 7 Market Estimates and Forecast, By IVD Product Category, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Reagents & assay kits

- 7.3 Sample collection & transport Products

- 7.4 Rapid diagnostic tests (RDTs)

- 7.5 Molecular diagnostic kits

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 IVD manufacturers

- 8.3 Contract packaging organizations (CPOs)

- 8.4 Medical device OEMs

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor Limited

- 10.1.2 Aptargroup Incorporated

- 10.1.3 Corning Incorporated

- 10.1.4 Greiner Holding AG

- 10.1.5 Oliver

- 10.1.6 VWR International, LLC.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Globe Scientific Inc.

- 10.2.1.2 Peacock Industries

- 10.2.1.3 FUSION BIOTECH

- 10.2.2 Asia Pacific

- 10.2.2.1 Abdos Labtech Private Limited

- 10.2.2.2 ACADEMY MEDICAL INSTRUMENTS Limited Company

- 10.2.2.3 Amrit Scientific Ind. Private Limited

- 10.2.2.4 AdvaCare Pharma

- 10.2.2.5 Focus Technology Co., Ltd.

- 10.2.2.6 YuHuan KangJia

- 10.2.2.7 Zhuhai Ideal Biotech Co., Ltd

- 10.2.2.8 Ajosha Bio Teknik Pvt. Ltd.

- 10.2.3 Europe

- 10.2.3.1 Kindly (KDL) Group

- 10.2.3.2 Labtech Disposables

- 10.2.3.3 Narang Medical Limited

- 10.2.1 North America