PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019078

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019078

Vortex Heat Meters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

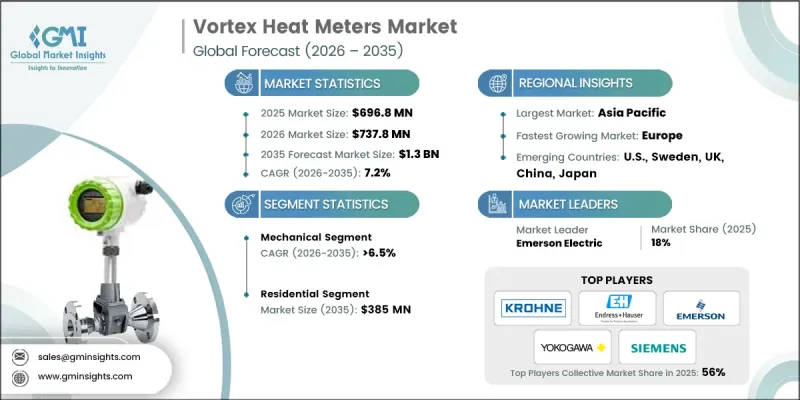

The Global Vortex Heat Meters Market was valued at USD 696.8 million in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 1.3 billion by 2035.

Growth is driven by the rising need for advanced flow measurement technologies capable of delivering precise and consistent performance. These meters operate based on vortex flow principles, enabling reliable monitoring of thermal energy consumption in various systems. Increasing demand for energy-efficient solutions, along with the expansion of modern heating networks in urban environments, is significantly shaping market dynamics. Integration with smart metering platforms and building management systems is further enhancing their functionality and adoption. Continuous improvements in sensor design, material quality, and digital integration are supporting higher accuracy and long-term reliability. Additionally, regulatory focus on energy efficiency and transparent billing practices is encouraging wider deployment, reinforcing the importance of vortex heat meters in modern energy management systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $696.8 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 7.2% |

Rising investments in infrastructure development and the growing adoption of sustainable heating technologies are further accelerating market demand. The increasing emphasis on precise energy monitoring and efficient heat utilization is influencing purchasing decisions across industries. As organizations adopt advanced energy management strategies, the need for accurate and durable metering solutions continues to grow. Technological advancements are enabling better performance under varying operational conditions, while the shift toward environmentally responsible systems is strengthening overall market potential. These factors collectively contribute to the steady expansion of the vortex heat meters industry.

The mechanical segment is expected to grow at a CAGR of 6.5% through 2035, supported by its straightforward design and minimal maintenance requirements. These systems are widely preferred for their cost-effectiveness and dependable operation, making them suitable for a variety of applications. Ongoing enhancements in calibration methods and sensing technologies are improving measurement accuracy and reliability. Their compatibility with existing metering infrastructure also supports continued adoption, while efforts to optimize manufacturing processes are helping reduce overall costs, further strengthening segment growth.

The residential segment is projected to reach USD 385 million by 2035, driven by increasing adoption of energy-efficient solutions in modern housing developments. Homeowners and developers are placing greater emphasis on sustainable construction practices and advanced energy monitoring systems. The integration of smart technologies, including IoT-enabled devices, is enabling real-time tracking and improved control over energy consumption. Enhanced system designs that combine functionality with user-friendly features are also contributing to increased adoption. As consumer awareness around energy efficiency continues to rise, the residential segment is expected to experience sustained growth.

U.S. Vortex Heat Meters Market is anticipated to reach USD 130 million by 2035, supported by rising energy costs and a growing focus on efficient energy utilization. Increased adoption of automation and compliance with stringent energy regulations are key factors influencing market expansion. These meters offer advantages such as durability, low maintenance, and reliable performance under demanding conditions, making them well-suited for a wide range of applications. The push toward energy optimization and environmentally conscious practices is further driving adoption, alongside continued investments in modern infrastructure and sustainable building initiatives.

Major companies operating in the Global Vortex Heat Meters Market include Siemens, ABB, Honeywell International, Schneider Electric, Emerson Electric, Endress+Hauser, Yokogawa Electric Corporation, KROHNE, Badger Meter, Spirax Sarco, TLV, KOBOLD Instruments, Apure, Sino-Inst, Grainger, Arrow Electronics, and WPG Holdings. Companies in the Global Vortex Heat Meters Market are focusing on strengthening their market position through innovation, strategic partnerships, and expanded product offerings. Investments in advanced sensor technologies and digital integration are enabling the development of more accurate and efficient metering solutions. Many players are enhancing their portfolios with smart and connected devices that support real-time monitoring and data analytics. Collaborations with infrastructure developers and energy service providers are helping companies expand their reach and secure long-term contracts. Additionally, firms are prioritizing compliance with global energy efficiency standards while optimizing production processes to reduce costs. Expanding distribution networks and improving after-sales services further support customer retention and long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & Confidence Scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By Application

- 3.8.2 By Region

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Static

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 College/University

- 6.3.2 Office Building

- 6.3.3 Government Building

- 6.3.4 Others

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Poland

- 7.3.3 Sweden

- 7.3.4 Denmark

- 7.3.5 Finland

- 7.3.6 Italy

- 7.3.7 UK

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Apure

- 8.3 Arrow Electronics

- 8.4 Badger Meter

- 8.5 Emerson Electric

- 8.6 Endress+Hauser

- 8.7 Grainger

- 8.8 Honeywell International

- 8.9 KROHNE

- 8.10 KOBOLD Instruments, Inc.

- 8.11 Schneider Electric

- 8.12 Siemens

- 8.13 Spirax Sarco

- 8.14 Sino-Inst

- 8.15 TLV Co., Ltd.

- 8.16 WPG Holdings

- 8.17 Yokogawa Electric Corporation