PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019087

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019087

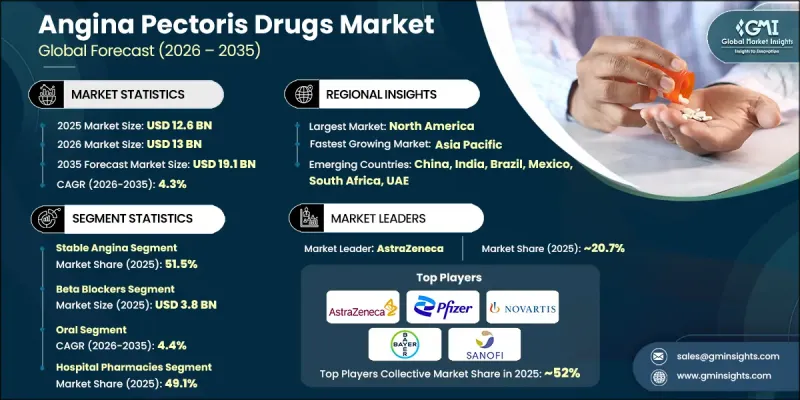

Angina Pectoris Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Angina Pectoris Drugs Market was valued at USD 12.6 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 19.1 billion by 2035.

The angina pectoris drugs market is driven by the increasing prevalence of lifestyle-related risk factors, including poor dietary habits, physical inactivity, and rising stress levels, which are contributing to a higher incidence of cardiovascular conditions. These factors are leading to a growing number of patients affected by conditions associated with angina, thereby increasing the demand for effective treatment options. The angina pectoris drugs market is also supported by advancements in healthcare infrastructure and improved access to medical therapies. In addition, rising awareness regarding heart health and early diagnosis is encouraging timely treatment, further strengthening market growth. As healthcare systems continue to focus on managing chronic conditions and improving patient outcomes, the angina pectoris drugs market is expected to expand steadily across both developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.6 Billion |

| Forecast Value | $19.1 Billion |

| CAGR | 4.3% |

The angina pectoris drugs market encompasses a range of therapeutic options designed to manage chest pain and improve cardiac function by enhancing blood flow or reducing the heart's oxygen demand. Treatment approaches include multiple drug categories that help control symptoms, prevent recurring episodes, and lower the risk of complications. The angina pectoris drugs market is also benefiting from the growing availability of generic medications, which have improved affordability and expanded patient access, particularly in cost-sensitive regions. At the same time, continuous innovation in drug formulations and delivery mechanisms is improving treatment adherence, minimizing side effects, and enhancing overall therapeutic outcomes, supporting ongoing market development.

The stable angina segment accounted for 51.5% share in 2025, reflecting its widespread occurrence among patients with cardiovascular conditions. This segment is driven by the consistent need for long-term management therapies that effectively control symptoms. The angina pectoris drugs market benefits from established treatment approaches that support reliable disease management. Increasing awareness and improved diagnostic capabilities are also contributing to higher detection rates, further supporting the growth of this segment.

The beta blockers segment was valued at USD 3.8 billion in 2025 and continues to play a central role in the angina pectoris drugs market. These medications are widely used due to their ability to regulate heart function and improve patient outcomes. The angina pectoris drugs market is supported by the broad clinical application of beta blockers, particularly in managing cardiovascular conditions. The rising prevalence of associated health conditions is further driving demand for these therapies, reinforcing segment growth.

North America Angina Pectoris Drugs Market accounted for 41.2% share in 2025 and is expected to grow at a CAGR of 4.2% during 2026-2035. The angina pectoris drugs market in the region is supported by advanced healthcare infrastructure, high awareness levels, and strong adoption of medical treatments. Continued investment in healthcare systems and ongoing research initiatives are contributing to sustained demand, while supportive reimbursement frameworks are further enhancing access to treatment.

Key companies operating in the Global Angina Pectoris Drugs Market include Pfizer, Novartis, AstraZeneca, Bayer, Sanofi, Merck, Eli Lilly and Company, Amgen, GlaxoSmithKline, Boehringer Ingelheim International, Gilead Sciences, Otsuka Pharmaceutical, Cadila Pharmaceuticals, and AdvaCare Pharma. Companies in the Angina Pectoris Drugs Market are focusing on strengthening their position through continuous research and development and strategic collaborations. Many players are investing in the development of advanced drug formulations to improve efficacy and patient compliance. Expansion of generic drug portfolios is helping companies reach a broader patient base and enhance affordability. Strategic partnerships and licensing agreements enable access to new markets and technologies. Companies are also increasing their presence in emerging economies to capture untapped opportunities. In addition, efforts to streamline supply chains and improve manufacturing efficiency are supporting cost optimization. Emphasis on innovation, regulatory approvals, and patient-centric solutions continues to drive competitive advantage in the angina pectoris drugs market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases

- 3.2.1.2 Advancements in drug development

- 3.2.1.3 Increasing lifestyle-related risk factors

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Side effects associated with the drugs

- 3.2.2.2 Growing adoption of minimally invasive surgeries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of biosimilar and generic offerings

- 3.2.3.2 Rising development of novel delivery systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.6 Pipeline analysis

- 3.7 Impact of AI and generative AI on the market

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Stable angina

- 5.3 Unstable angina

- 5.4 Microvascular angina

- 5.5 Prinzmetal angina

Chapter 6 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Beta blockers

- 6.3 Nitrates

- 6.4 Anti-platelets

- 6.5 Calcium channel blockers

- 6.6 Anticoagulants

- 6.7 ACE inhibitors

- 6.8 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AdvaCare Pharma

- 10.2 Amgen

- 10.3 AstraZeneca

- 10.4 Bayer

- 10.5 Boehringer Ingelheim International

- 10.6 Cadila Pharmaceuticals

- 10.7 Eli Lilly and Company

- 10.8 Gilead Sciences

- 10.9 GlaxoSmithKline

- 10.10 Merck

- 10.11 Novartis

- 10.12 Otsuka Pharmaceutical

- 10.13 Pfizer

- 10.14 Sanofi