PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019089

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019089

Thermal Spray Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2034

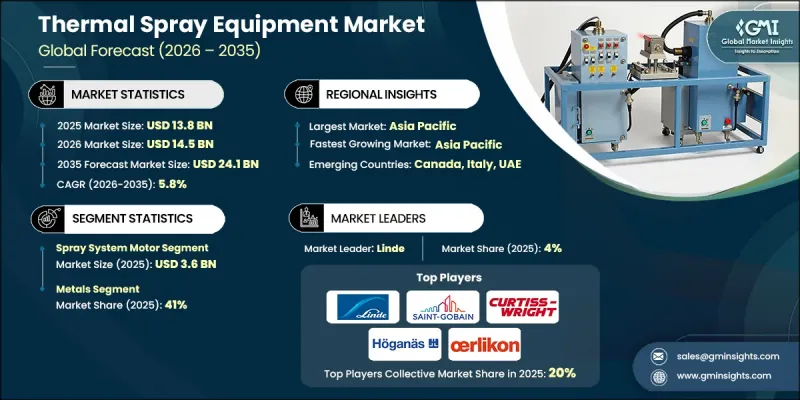

The Global Thermal Spray Equipment Market was valued at USD 13.8 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 24.1 billion by 2035.

The market's expansion is fueled by industries seeking advanced solutions to enhance component durability and operational efficiency. Thermal spray technology is increasingly adopted across aerospace, automotive, energy, heavy engineering, and manufacturing sectors to protect surfaces exposed to extreme temperatures, corrosive environments, and high-friction conditions. The growing reliance on high-performance coatings is driven by the need to extend equipment life, reduce maintenance costs, and improve product performance. Material science advancements and innovative spray techniques have opened new applications in electronics, biomedical devices, and renewable energy, providing additional protective and functional benefits. Manufacturers are now leveraging automation, robotic spray systems, and precise control technologies to achieve consistent coating quality and maximize adhesion, density, and resistance. These developments enable industries to improve sustainability, reduce material waste, and maintain compliance with environmental regulations, supporting steady market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.8 Billion |

| Forecast Value | $24.1 Billion |

| CAGR | 5.8% |

In 2025, the spray system motor segment reached USD 3.6 billion. Spray systems consist of four core components: the spray gun, feedstock delivery unit, energy supply, and control systems. They operate using combustion, plasma, or electrical energy to create high-velocity, heated material streams that produce tightly bonded coatings. These systems enhance the wear, corrosion, and temperature resistance of industrial components, ensuring longer operational life and improved performance across sectors.

The metals segment accounted for 41% share in 2025, making it the dominant coating material category. Metallic coatings, including alloys, aluminum, nickel, and stainless steel, provide superior strength, durability, and corrosion resistance. These coatings are widely applied across industries to enhance the reliability and efficiency of components subjected to mechanical stress, chemical exposure, and thermal extremes. Their versatility and performance benefits make metal coatings essential for high-demand industrial applications.

North America Thermal Spray Equipment Market held 89% share, generating USD 3.3 billion in 2025. Market growth in the U.S. is supported by advanced aerospace, defense, automotive, and energy sectors that demand high-performance coatings to maintain component efficiency. The country's established manufacturing ecosystem enables rapid adoption of robotic spray systems, digital monitoring, and advanced material integration. Focus on sustainability, regulatory compliance, and maintenance optimization further boosts demand for sophisticated thermal spray equipment in North America.

Major players in the Global Thermal Spray Equipment Industry include Oerlikon, Hannecard Roller Coatings, Alloy Metal Surface Technologies, Lincoln Electric, Saint Gobain, Curtiss-Wright, Brycoat, Bodycote, Kennametal, Linde, Wall Colmonoy, Aimtek, Ador Fontech, and A&A Thermal Spray Coatings. Companies in the Thermal Spray Equipment Market pursue strategies such as technological innovation, strategic partnerships, and service differentiation to strengthen their market foothold. Firms invest heavily in R&D to improve robotic systems, plasma and combustion spray technologies, and real-time digital monitoring capabilities. Strategic alliances with industrial manufacturers and material suppliers allow companies to expand applications across diverse sectors. Emphasis on maintenance services, training programs, and turnkey solutions enhances customer loyalty. Geographic expansion into emerging markets, product portfolio diversification, and sustainability-focused innovations support long-term growth. Competitive differentiation is achieved through high-precision coating solutions, durability improvements, and advanced energy-efficient systems that meet industry-specific operational requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Surface type

- 2.2.4 Operation

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing industrial application

- 3.2.1.2 Growing demand for surface protection

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment

- 3.2.2.2 Skilled labor shortages

- 3.2.3 Opportunities

- 3.2.3.1 Automation & robotics

- 3.2.3.2 Growth in high-performance coating materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Spray system

- 5.2.1 Plasma

- 5.2.2 Twin arc

- 5.2.3 Flame spray

- 5.2.4 HVOF

- 5.2.5 Powder flame spray

- 5.2.6 Others (vacuum, etc.)

- 5.3 Booths

- 5.4 Dust collection systems

- 5.5 Chillers

- 5.6 Spray guns and nozzles

- 5.7 Feeder systems

- 5.8 Gas systems

- 5.9 Others (gas detection systems, etc.)

Chapter 6 Market Estimates and Forecast, By Surface Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Metals

- 6.3 Ceramics

- 6.4 Polymers

- 6.5 Composites

- 6.6 Others (e.g., carbides, oxides)

Chapter 7 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

- 7.4 Manual

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Aerospace

- 8.3 Automotive

- 8.4 Electronics

- 8.5 Biomedical

- 8.6 Manufacturing

- 8.7 Oil and gas

- 8.8 Energy and power

- 8.9 Others (medical devices, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 A&A Thermal Spray Coatings

- 11.2 Ador Fontech

- 11.3 Aimtek

- 11.4 Alloy Metal Surface Technologies

- 11.5 Bodycote

- 11.6 Brycoat

- 11.7 Curtiss-Wright

- 11.8 Hannecard Roller Coatings

- 11.9 Hoganas

- 11.10 Kennametal

- 11.11 Lincoln Electric

- 11.12 Linde

- 11.13 Oerlikon

- 11.14 Saint Gobain

- 11.15 Wall Colmonoy