PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019120

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019120

Ground Support Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

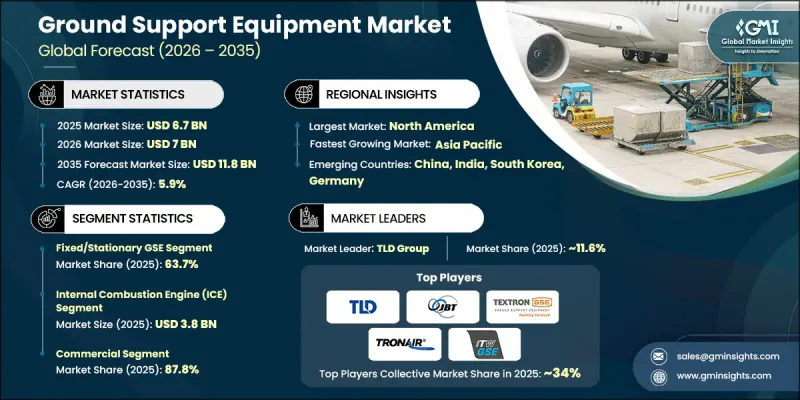

The Global Ground Support Equipment Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 11.8 billion by 2035.

The ground support equipment market is witnessing consistent expansion, driven by the increasing number of commercial aircraft worldwide and the growing need to improve airport turnaround efficiency. Airlines and airport operators are placing greater emphasis on reducing ground time while enhancing operational performance, which is accelerating demand for advanced and reliable equipment. Ongoing investments in airport infrastructure development and modernization are further supporting market growth. In addition, the rising presence of low-cost carriers and their focus on cost optimization is encouraging the use of standardized and technology-driven solutions across airports. The integration of advanced systems that enhance operational visibility and efficiency is also contributing to the evolution of ground handling processes, strengthening long-term growth prospects across the global aviation ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 5.9% |

The ground support equipment market is further supported by the continuous expansion of the global aircraft fleet and increasing investments in airport upgrades aimed at improving airside operations. Growing adoption of connected and digitally enabled equipment is transforming maintenance and utilization practices. Real-time monitoring capabilities, predictive maintenance, and improved fleet management are enabling operators to reduce downtime and enhance efficiency. The increasing shift toward digital airport ecosystems is expected to drive the adoption of advanced ground support technologies over the coming years.

The fixed or stationary ground support equipment segment accounted for 63.7% share in 2025, supported by its essential role in high-traffic airport operations. These systems are integrated into airport infrastructure and contribute to improved operational efficiency, reduced emissions, and enhanced reliability in aircraft servicing processes.

The electric ground support equipment segment is anticipated to grow at a CAGR of 6.3% during 2026 to 2035. Rising focus on sustainability and emission reduction is encouraging airports and airlines to adopt electric alternatives. These solutions offer lower operating costs, reduced noise levels, and improved environmental performance, while advancements in battery technologies are supporting their widespread deployment.

North America Ground Support Equipment Market held a 41.1% share in 2025, driven by increasing air passenger traffic, airport expansion projects, and growing adoption of electric airside vehicles. The region continues to invest in sustainable infrastructure and advanced technologies, supporting the transition toward more efficient and environmentally friendly ground operations. Ongoing modernization initiatives and increasing adoption of automation are further strengthening market growth across the region.

Key players operating in the Global Ground Support Equipment Market include JBT Corporation, Rheinmetall AG, Textron Ground Support Equipment Inc., TLD Group, ITW GSE, Cobus Industries, Charlatte Manutention, Tronair Inc., Weihai Guangtai Airport Equipment, AERO Specialties, Air+MAK Industries Inc., ATEC Inc., Eagle Tugs, Unitron, LP, and Sinfonia Technology Co. Ltd. Companies in the Global Ground Support Equipment Market are adopting strategic initiatives to strengthen their competitive position and expand their global footprint. Investments in research and development are enabling the introduction of advanced, energy-efficient, and digitally connected equipment. Market participants are focusing on electrification and sustainable product development to align with environmental regulations and industry goals. Strategic partnerships, mergers, and acquisitions are being pursued to enhance technological capabilities and broaden market reach. Additionally, companies are expanding their distribution networks and service offerings to improve customer engagement. Continuous innovation, along with a focus on automation and smart technologies, is helping companies maintain a strong presence and drive long-term growth in the ground support equipment industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Power source trends

- 2.2.3 Equipment type trends

- 2.2.4 Automation level trends

- 2.2.5 Application trends

- 2.2.6 Ownership trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global commercial aircraft fleet expansion

- 3.2.1.2 Stringent airport turnaround time requirements

- 3.2.1.3 Rising airport infrastructure modernization projects

- 3.2.1.4 Growth in low-cost carrier operations

- 3.2.1.5 Airline focus on operational efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex regulatory compliance across regions

- 3.2.2.2 Limited charging infrastructure at regional airports

- 3.2.3 Market opportunities

- 3.2.3.1 Smart GSE integration with airport automation systems

- 3.2.3.2 Aftermarket services and fleet retrofitting demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Mobile GSE

- 5.2.1 Self-propelled equipment

- 5.2.2 Towable equipment

- 5.3 Fixed/stationary GSE

- 5.3.1 Passenger boarding bridges

- 5.3.2 Fixed ground power units

- 5.3.3 Fixed pre-conditioned air systems

Chapter 6 Market Estimates and Forecast, By Power Source, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Electric

- 6.2.1 Battery-electric systems (lithium-ion)

- 6.2.2 Battery-electric systems (lead-acid)

- 6.2.3 Grid-powered systems

- 6.3 Internal combustion engine (ICE)

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Aircraft movement & positioning equipment

- 7.2.1 Pushback tractors

- 7.2.2 Luggage tugs

- 7.2.3 Chocks & wheel restraints

- 7.2.4 Others

- 7.3 Cargo & baggage handling equipment

- 7.3.1 Belt loaders

- 7.3.2 Container & pallet loaders

- 7.3.3 Cargo dollies & baggage carts

- 7.3.4 Conveyor systems

- 7.3.5 Others

- 7.4 Passenger handling equipment

- 7.4.1 Passenger boarding bridges (PBBs)

- 7.4.2 Passenger stairs

- 7.4.3 Apron buses

- 7.4.4 Others

- 7.5 Aircraft servicing equipment

- 7.5.1 Ground power units (GPUs)

- 7.5.2 Pre-conditioned air units (PCAs/ACUs)

- 7.5.3 Fuel trucks & refueling systems

- 7.5.4 Others

- 7.6 Aircraft safety & maintenance equipment

- 7.6.1 Air start units (ASUs)

- 7.6.2 Deicing & anti-icing equipment

- 7.6.3 Maintenance stands & platforms

- 7.6.4 Others

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Automation Level, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Conventional/manual-operated GSE

- 8.3 Semi-automated GSE (Telematics & IoT-Enabled)

- 8.4 Autonomous GSE (AGVS)

- 8.4.1 Autonomous tugs & tractors

- 8.4.2 Autonomous baggage vehicles

- 8.4.3 Autonomous maintenance equipment

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial aviation

- 9.2.1 Passenger airlines

- 9.2.2 Cargo airlines

- 9.2.3 Business aviation

- 9.3 Military & defense aviation

Chapter 10 Market Estimates and Forecast, By Ownership, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Airport-owned GSE

- 10.3 Airline-owned GSE

- 10.4 Ground handling service provider-owned GSE

- 10.5 Leased GSE

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 TLD Group

- 12.1.2 JBT Corporation

- 12.1.3 Textron Ground Support Equipment Inc.

- 12.1.4 Weihai Guangtai Airport Equipment

- 12.1.5 ITW GSE

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 AERO Specialties

- 12.2.1.2 Tronair Inc.

- 12.2.1.3 Eagle Tugs

- 12.2.1.4 Unitron, LP

- 12.2.2 Asia Pacific

- 12.2.2.1 Sinfonia Technology Co. Ltd.

- 12.2.2.2 Japanese GSE manufacturers

- 12.2.2.3 Air+MAK Industries Inc.

- 12.2.3 Europe

- 12.2.3.1 Charlatte Manutention

- 12.2.3.2 Cobus Industries

- 12.2.3.3 Rheinmetall AG

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 ATEC Inc.