PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019135

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019135

North America Flue Gas Desulfurization System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

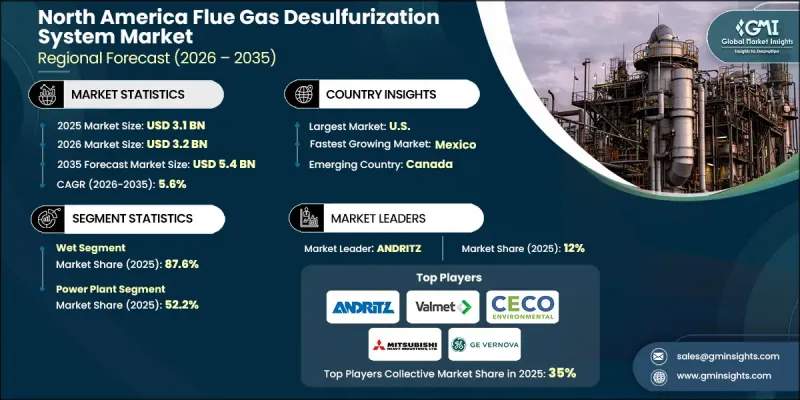

North America Flue Gas Desulfurization System Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 5.4 billion by 2035.

The market expansion is driven by tightening air quality regulations that redefine SO2 compliance standards across multiple industries. These evolving requirements compel facilities to upgrade outdated scrubbers, enhance reagent systems, or implement wet limestone FGD systems where semi-dry technologies fall short. Regulatory shifts also influence permitting, as projects seeking modifications must demonstrate compliance with revised modeling and emission limits. This increases demand for absorbers, reaction tanks, mist eliminators, and gypsum handling systems across not only utility boilers but also industrial plants. Standardized regulatory pathways reduce administrative burdens, accelerate permitting, and encourage earlier retrofits, component replacements, and fuel conversions. Faster project timelines ultimately support quicker SO2 reduction implementation, reinforcing the demand for wet FGD systems that offer high capture efficiency, predictable operations, and reliable byproduct management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 5.6% |

The dry FGD segment is expected to grow at a CAGR of 3.5% by 2035, offering roughly 80% sulfur removal, primarily suitable for low-sulfur fuel applications. Technological advancements in sorbent chemistry, reagent handling, and flow control are improving removal efficiency to 90-95%, narrowing the gap with wet systems and enhancing adoption across select industrial processes.

The cement sector is projected to grow at a CAGR of 7.3% through 2035, driven by NESHAP enforcement and rising demand for infrastructure development. Cement plants are increasingly implementing FGD solutions to manage sulfur content in fuels and raw materials, often integrating desulfurization with particulate and mercury control technologies to meet compliance standards and optimize operational efficiency.

U.S. Flue Gas Desulfurization System Market held a 67.6% share in 2025, valued at USD 2.1 billion. Stricter effluent and discharge regulations are driving system deployment across the country. The evolving regulatory environment, including amendments to the Clean Air Act and Clean Water Act, is shaping plant-level FGD modernization. Integrated scrubbers increasingly feature blowdown recycling, chemical dosing for metal removal, and on-site treatment upgrades. Industrial plants are adopting retrofit and modernized FGD systems to maintain compliance without exceeding discharge limits, which sustains strong demand for high-efficiency desulfurization technologies.

Key players operating in the North America Flue Gas Desulfurization System Market include AirPol, Andritz, Augusta Fiberglass, Babcock & Wilcox, Branch Environmental Corp, Carmeuse Americas, CECO Environmental, Ducon Infratechnologies, EnviroEnergy Solutions, FLSmidth, GEA Group, General Electric, Hitachi Zosen Inova, KC Cottrell, Marsulex Environmental Technologies (MET), Mitsubishi Heavy Industries, Suez, Thermax, and Valmet. Companies in the North America Flue Gas Desulfurization System Market are consolidating their positions through strategies centered on technological innovation, regulatory alignment, and strategic partnerships. Firms are investing in R&D to develop higher-efficiency scrubbers, advanced reagent handling, and integrated emission control solutions. Mergers and collaborations with EPC contractors and industrial operators expand geographic reach and project access. Companies focus on offering turnkey solutions that combine desulfurization with particulate, mercury, and effluent management, enhancing value for industrial clients. Adoption of digital monitoring and predictive maintenance technologies improves system reliability and operational efficiency, strengthening customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by country

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Application trends

- 2.1.4 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Advancements in automation and smart technologies

- 3.3.1.2 Focus on sustainability and energy efficiency

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High energy consumption

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Wet

- 5.3 Dry

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Power plants

- 6.3 Chemical & petrochemical

- 6.4 Cement

- 6.5 Metal processing & mining

- 6.6 Manufacturing

- 6.7 Others

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 U.S.

- 7.3 Canada

- 7.4 Mexico

Chapter 8 Company Profiles

- 8.1 AirPol

- 8.2 Andritz

- 8.3 Augusta Fiberglass

- 8.4 Babcock & Wilcox

- 8.5 Branch Environmental Corp

- 8.6 Carmeuse Americas

- 8.7 CECO Environmental

- 8.8 Ducon Infratechnologies

- 8.9 EnviroEnergy Solutions

- 8.10 FLSmidth

- 8.11 GEA Group

- 8.12 General Electric

- 8.13 Hitachi Zosen Inova

- 8.14 KC Cottrell

- 8.15 Marsulex Environmental Technologies (MET)

- 8.16 Mitsubishi Heavy Industries

- 8.17 Suez

- 8.18 Thermax

- 8.19 Valmet