PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019158

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019158

Smart Water Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

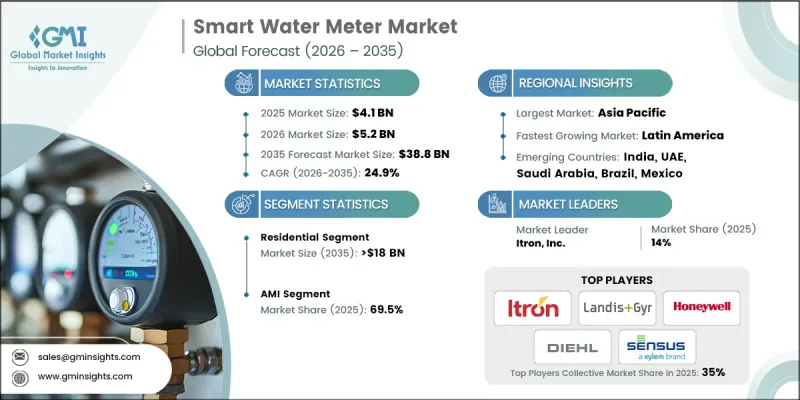

The Global Smart Water Meter Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 24.9% to reach USD 38.8 billion by 2035.

The surge is driven by rapid technological advancements, increasing water conservation initiatives, regulatory mandates, and the need for more efficient water management systems. Utilities and cities worldwide are adopting smart water meters to optimize water distribution, minimize wastage, and enhance operational efficiency. The demand for accurate, real-time monitoring of water consumption is a key growth factor, as conventional meters often rely on manual readings that are time-consuming and prone to errors. Smart meters integrated with IoT technology provide remote monitoring, automated billing, and real-time data collection, boosting efficiency and service quality. Government policies and incentive programs promoting water conservation and leakage detection, particularly in water-stressed regions, are further accelerating adoption. The market is also supported by growing digitalization efforts and sustainability goals, especially in emerging economies where water infrastructure modernization is critical.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $38.8 Billion |

| CAGR | 24.9% |

The residential segment is expected to reach USD 18 billion by 2035, driven by rising consumer adoption of smart meters to improve water and energy management, enable accurate billing, and support renewable energy integration. Smart meters in homes provide precise usage insights, empower consumers to manage consumption, and integrate seamlessly with home automation systems, contributing to market growth.

The AMI (Advanced Metering Infrastructure) segment captured 69.5% share in 2025, leading over AMR (Automatic Meter Reading) systems due to its two-way communication capabilities. AMI enables utilities to collect real-time data, remotely manage meters, detect leaks promptly, and respond faster to anomalies. Its integration with smart grids and digital water management solutions further reinforces its dominance, making it the preferred technology for efficient utility operations.

U.S. Smart Water Meter Market was valued at USD 704 million in 2025. The country faces rising water scarcity across several regions, influenced by population growth, aging infrastructure, and climate variability. Utilities in the U.S. are increasingly deploying smart meters to monitor consumption in real-time, identify leaks, and detect abnormal usage patterns, enhancing water conservation and operational efficiency.

Key players in the Global Smart Water Meter Market include Landis + Gyr, Diehl Stiftung, Itron, Inc., Honeywell International, and Xylem (Sensus). Companies in the Smart Water Meter Market are strengthening their presence through continuous innovation in IoT-enabled metering solutions and real-time analytics. They are focusing on strategic collaborations with utilities, governments, and technology providers to expand deployment and offer integrated water management systems. R&D investments drive the development of highly accurate, low-maintenance, and energy-efficient meters. Businesses are also leveraging data-driven services, remote diagnostics, and predictive maintenance to enhance customer value and operational reliability. Regional expansion, participation in government incentive programs, and sustainable product development are additional strategies to solidify their market foothold and capture a larger share of the rapidly growing smart water meter industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Price trend analysis, by region (USD/Unit)

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Utility

- 5.5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & '000 Units)

- 5.6 Key trends

- 5.7 AMI

- 5.8 AMR

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Hot water meter

- 6.3 Cold water meter

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 UAE

- 7.5.2 Saudi Arabia

- 7.5.3 South Africa

- 7.5.4 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Apator S.A.

- 8.3 Arad Group:

- 8.4 Badger Meter, Inc.

- 8.5 BMETERS S.r.l

- 8.6 Diehl Stiftung & Co. KG

- 8.7 Honeywell International Inc.

- 8.8 Itron Inc.

- 8.9 Kamstrup

- 8.10 Landis+Gyr

- 8.11 Neptune Technology Group Inc.

- 8.12 Ningbo Water Meter Co., Ltd.

- 8.13 Schneider Electric

- 8.14 Siemens

- 8.15 Sontex SA

- 8.16 Xylem (Sensus)

- 8.17 ZENNER International GmbH & Co. KG

- 8.18 Suez

- 8.19 Baylan Water Meters

- 8.20 BOVE Technology