PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019181

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019181

Sodium Cyanide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

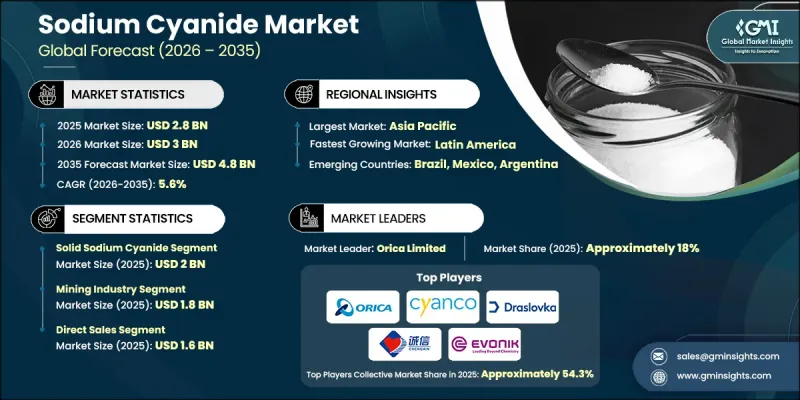

The Global Sodium Cyanide Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 4.8 billion by 2035.

The market expansion is fueled by rising gold and silver mining activities, where sodium cyanide is extensively used for the extraction of precious metals. Demand is particularly strong across Asia Pacific, Africa, and Latin America as ongoing exploration projects and new mining sites are developed. Mining companies are increasing production to meet global metal requirements, which directly boosts sodium cyanide consumption. Market dynamics are influenced by fluctuations in gold prices and growing investment in precious metals. Higher gold valuations encourage mining companies to resume previously paused operations, driving further demand. Additionally, advancements in cyanidation and mineral processing technologies are enhancing extraction efficiency, increasing recovery rates, and enabling lower-grade ores to be processed effectively, contributing to overall market growth. These factors collectively position sodium cyanide as a critical input for global mining operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 5.6% |

The solid sodium cyanide segment accounted for USD 2 billion in 2025, reflecting its dominant role in industrial and mining applications. Demand varies according to the specific needs of processing operations and the preferred form for efficiency, transport, storage, and handling. Mining companies select product types based on safety considerations, operational costs, and compatibility with existing processing systems. These evaluations ensure that sodium cyanide can be used effectively across diverse mining sites and chemical processing applications, supporting consistent supply and operational reliability.

The direct sales channels generated USD 1.6 billion in 2025, serving as the primary conduit for industrial and mining customers. Efficient distribution relies on procurement volumes, safety compliance, and handling requirements for hazardous materials. Large-scale buyers often rely on structured supply agreements and coordinated delivery systems to ensure consistent availability, minimizing operational disruptions and maintaining production schedules.

North America Sodium Cyanide Market accounted for USD 532 million in 2025. The regional market benefits from ongoing gold and silver mining activities, where sodium cyanide is used for heap leaching and other mineral processing methods. The United States maintains the largest share due to significant mining operations, while Canada contributes through established mining industries, particularly in regions with high mineral potential. Increasing mining production in these countries drives continuous demand for sodium cyanide.

Key players in the Global Sodium Cyanide Market include Orica Limited, Draslovka Holdings a.s., Australian Gold Reagents Pty Ltd, CSBP Limited, Cyanco International LLC, Evonik Industries AG, Gujarat Alkalies and Chemicals Limited, Hindusthan Chemicals Company, Kanto Chemical Co., Inc, Shaanxi United Chemical Co., Ltd., Taekwang Industrial Co., Ltd, Tongsuh Petrochemical Corporation, Hebei Chengxin Co., Ltd., and Kishida Chemical Co., Ltd. Companies in the Global Sodium Cyanide Market are focusing on expanding production capacity, establishing strategic supply agreements, and diversifying regional presence to strengthen market foothold. They invest in technology to enhance production efficiency, improve safety standards, and optimize handling procedures. Strategic partnerships with mining operators and industrial consumers are used to secure long-term contracts and ensure consistent demand. Companies also emphasize regulatory compliance, quality assurance, and sustainable chemical management practices. Leveraging advanced logistics, warehousing solutions, and direct sales channels helps to improve delivery efficiency, reduce operational risk, and maintain a competitive advantage across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in gold & silver mining activities

- 3.2.1.2 Rising gold prices & investment demand

- 3.2.1.3 Technological advancements in cyanidation processes.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns & catastrophic spill incidents

- 3.2.2.2 Stringent regulatory constraints & compliance costs.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing mining activities in emerging economies

- 3.2.3.2 Advancements in safer cyanide handling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022 - 2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Solid sodium cyanide

- 5.2.1 Briquettes

- 5.2.2 Pellets

- 5.3 Liquid sodium cyanide

- 5.4 Powder

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Mining industry

- 6.3 Chemical manufacturing

- 6.4 Jewelry manufacturing

- 6.5 Pharmaceuticals

- 6.6 Agriculture

- 6.7 Textiles

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Distributors & wholesalers

- 7.4 Online sales

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Australian Gold Reagents Pty Ltd

- 9.2 CSBP Limited

- 9.3 Cyanco International LLC

- 9.4 Draslovka Holdings a.s.

- 9.5 Evonik Industries AG

- 9.6 Gujarat Alkalies and Chemicals Limited

- 9.7 Hebei Chengxin Co., Ltd

- 9.8 Hindusthan Chemicals Company

- 9.9 Kanto Chemical Co., Inc

- 9.10 Kishida Chemical Co., Ltd.

- 9.11 Orica Limited

- 9.12 Shaanxi United Chemical Co., Ltd.

- 9.13 Taekwang Industrial Co., Ltd

- 9.14 Tongsuh Petrochemical Corporation