PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019182

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019182

Intelligent All-Wheel Drive System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

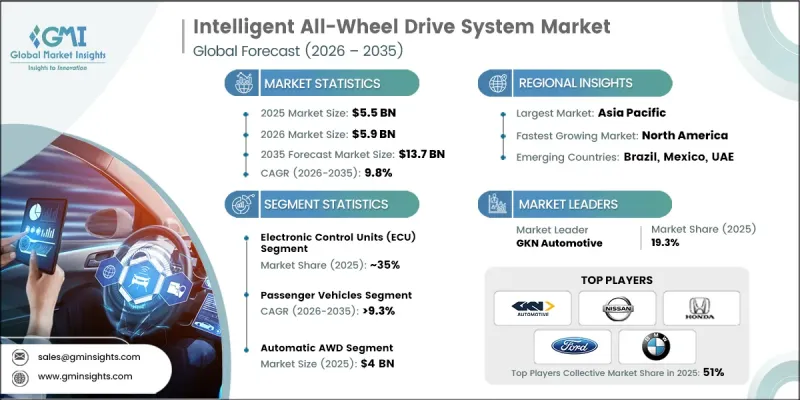

The Global Intelligent All-Wheel Drive System Market was valued at USD 5.5 billion in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 13.7 billion by 2035.

The intelligent all-wheel drive system market is driven by rising demand for improved traction, stability, and safety, along with the growing popularity of premium vehicles. Expanding production of sport utility vehicles, crossovers, and electrified vehicles is further accelerating adoption. The intelligent all-wheel drive system market is also benefiting from increasing pressure on automakers and suppliers to differentiate vehicle performance, enhance handling, and meet evolving regulatory standards. In addition, continuous advancements in drivetrain engineering are enabling improved fuel efficiency and optimized power distribution. As vehicle architecture becomes more sophisticated, the intelligent all-wheel drive system market is positioned for sustained growth, supported by innovation, electrification trends, and the integration of advanced control technologies across global automotive platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.5 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 9.8% |

The intelligent all-wheel drive system market is evolving rapidly with the introduction of advanced drivetrain technologies that enhance system efficiency and responsiveness. Innovations in torque management, automated control systems, and electronic integration are redefining how power is distributed across vehicles. The intelligent all-wheel drive system market benefits from the growing adoption of electrification and connected vehicle technologies, which are influencing drivetrain design priorities. Manufacturers are focusing on scalable platforms, optimized system architectures, and cost-efficient components to enable broader adoption across different vehicle segments. These developments are improving performance, energy efficiency, and system reliability while supporting long-term market expansion.

The electronic control unit segment accounted for 35% share in 2025 and is expected to grow at a CAGR of 8.7% from 2026 to 2035. This segment plays a central role in managing torque distribution and coordinating drivetrain operations, making it a critical component in modern systems. The intelligent all-wheel drive system market is supported by increasing integration of advanced control technologies, which enhance vehicle stability, efficiency, and safety. Strong adoption across new vehicle production and service applications continues to reinforce demand for electronic control units.

The passenger vehicles segment held 76% share in 2025 and is projected to grow at a CAGR of 9.3% through 2035. This dominance is driven by high global production volumes and increasing consumer preference for improved vehicle performance and all-weather capability. The intelligent all-wheel drive system market is further supported by the widespread integration of electronically controlled drivetrain systems across various vehicle categories, strengthening the segment's leadership position.

China Intelligent All-Wheel Drive System Market held a 51% share in 2025, generating USD 1 billion. The intelligent all-wheel drive system market in China is expanding due to strong automotive production capacity and rising demand for advanced vehicle technologies. Increasing focus on performance, safety, and efficiency is encouraging the adoption of advanced drivetrain systems. Continuous collaboration between manufacturers and suppliers is further supporting innovation and system optimization, driving sustained growth in the regional market.

Key companies operating in the Global Intelligent All-Wheel Drive System Market include BorgWarner, GKN Automotive, Delphi Technologies, Hitachi Automotive, Ford, BMW, Nissan, Honda, Acura, and Infiniti. Companies in the Global Intelligent All-Wheel Drive System Market are enhancing their market position through innovation, partnerships, and technological advancement. Leading players are investing in advanced torque management systems, electronic control technologies, and electrified drivetrain solutions to improve performance and efficiency. Strategic collaborations with automotive manufacturers are enabling seamless integration of AWD systems into modern vehicle platforms. Companies are also focusing on scalable and modular system designs to cater to a wider range of vehicle segments. Expansion into emerging markets and strengthening production capabilities are further supporting growth. In addition, continuous investment in research and development is helping companies deliver differentiated solutions and maintain a competitive edge in the evolving automotive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 System

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising EV & Hybrid Vehicle Adoption

- 3.2.1.2 Consumer Demand for Safety & Performance

- 3.2.1.3 Technological Advancements

- 3.2.1.4 Premiumization of Vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High System Cost

- 3.2.2.2 Complex Integration & Validation

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification & Multi-Motor AWD Expansion

- 3.2.3.2 Connected & Predictive AWD Solutions

- 3.2.3.3 Lightweight and Energy-Efficient Drivetrain Designs

- 3.2.3.4 Standardization and Modular AWD Platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7 Regulations

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Emission Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO Emission Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of Artificial Intelligence (AI)

- 3.12.1 Predictive maintenance of AWD systems

- 3.12.2 Optimized torque distribution & energy efficiency

- 3.12.3 Personalized driving modes

- 3.12.4 Gamification & driver engagement

- 3.12.5 Real-time traction & stability control

- 3.12.6 Automated system analytics & optimization

- 3.13 Sustainability and Environmental Aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Use case scenarios

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electronic Control Unit (ECU)

- 5.2.1 32-bit ECU

- 5.2.2 64-bit ECU

- 5.3 Sensors

- 5.3.1 Wheel Speed Sensors

- 5.3.2 Steering Angle Sensors

- 5.3.3 Yaw Rate Sensors

- 5.3.4 Accelerometers

- 5.4 Actuators

- 5.4.1 Electromagnetic Clutch Actuators

- 5.4.2 Hydraulic Actuators

- 5.4.3 Electromechanical Actuators

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.2.1 Gasoline

- 7.2.2 Diesel

- 7.3 Electric Vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Hybrid Electric Vehicles (HEV)

Chapter 8 Market Estimates & Forecast, By System, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Automatic AWD

- 8.2.1 Full-Time Automatic AWD

- 8.2.2 Part-Time Automatic AWD

- 8.3 Manual/Driver-Selectable AWD

- 8.3.1 On-Demand Manual Engagement

- 8.3.2 Lockable Differential Systems

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 On-Road

- 9.2.1 Urban Driving

- 9.2.2 Highway/Long-Distance

- 9.2.3 All-Weather Commuting

- 9.3 Off-Road

- 9.3.1 Construction Sites

- 9.3.2 Agricultural Operations

- 9.3.3 Recreational/Sports Utility

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 Acura

- 12.1.2 BMW

- 12.1.3 BorgWarner

- 12.1.4 Delphi Technologies

- 12.1.5 Ford

- 12.1.6 GKN Automotive

- 12.1.7 Hitachi Automotive

- 12.1.8 Honda

- 12.1.9 Infiniti

- 12.1.10 Nissan

- 12.2 Regional Player

- 12.2.1 Aisin Seiki

- 12.2.2 Inalfa Roof Systems

- 12.2.3 JTEKT

- 12.2.4 Magna International

- 12.2.5 Mando

- 12.2.6 Mitsubishi Motors

- 12.2.7 Toyoda Gosei

- 12.2.8 Valeo

- 12.2.9 Webasto

- 12.2.10 ZF Friedrichshafen