PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019207

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019207

Hematocrit Test Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

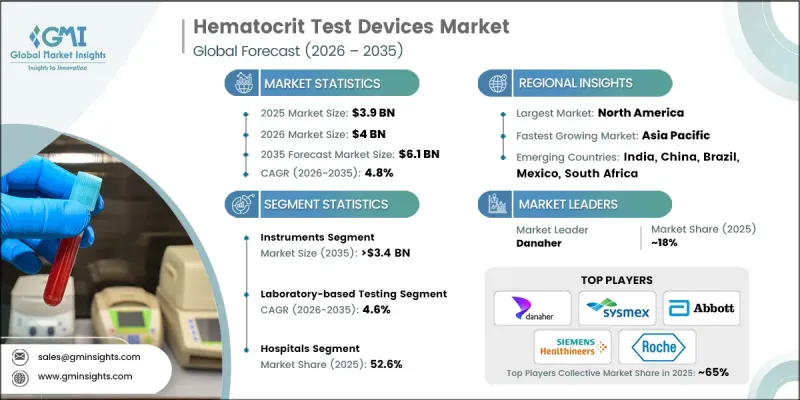

The Global Hematocrit Test Devices Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 6.1 billion by 2035.

Market growth is driven by the rising prevalence of blood disorders, an aging global population, and continuous advancements in point-of-care testing technologies. Hematocrit test devices measure the proportion of red blood cells in a patient's blood, expressed as a percentage of total blood volume, and are widely used in hospitals, diagnostic labs, and point-of-care facilities to monitor conditions such as anemia, dehydration, and other hematological disorders. Modern devices integrate compact designs, digital interfaces, and automated sample processing, improving testing speed, accuracy, and operational efficiency. The adoption of portable and handheld hematocrit analyzers is rapidly increasing, enabling healthcare professionals to perform bedside testing in clinics, emergency care, and ambulatory services. Rapid results enhance clinical decision-making, support trauma management, and improve patient outcomes while reducing reliance on centralized laboratories. The market is further supported by innovations in microfluidics, automated hematology platforms, and continuous improvements in diagnostic accuracy.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 4.8% |

The reagents and consumables segment generated USD 1.6 billion in 2025 and is projected to grow at a CAGR of 5.4% through 2035. The demand for reagents, microcapillary tubes, and cartridges is driven by the high frequency of hematocrit testing and expanding patient screening programs across hospitals and diagnostic laboratories, ensuring recurring revenue for suppliers.

The laboratory-based testing devices segment accounted for USD 2.6 billion in 2025 and is expected to grow at a CAGR of 4.6% through 2035. Laboratory systems are favored for their high precision and reliability, offering accurate hematocrit results necessary for diagnosing conditions such as anemia and polycythemia. The increasing complexity of patient cases and demand for detailed diagnostics continue to reinforce laboratory-based testing as the benchmark standard.

U.S. Hematocrit Test Devices Market was valued at USD 1.45 billion in 2025, with a projected CAGR of 4.3% through 2035. The country benefits from a sophisticated healthcare infrastructure comprising advanced hospitals, diagnostic laboratories, and research institutions capable of high-volume, precise testing. The emphasis on early detection, continuous patient monitoring, and the adoption of cutting-edge hematology analyzers further support market growth in the region.

Key players operating in the Global Hematocrit Test Devices Market include Roche, Abbott, Danaher, Siemens Healthineers, Nova Biomedical, EKF Diagnostics, NIHON KOHDEN, Boule, Mindray, Diatron, HORIBA Medical, A. Menarini, BIO-RAD, SENSA CORE, and Sysmex. Companies in the Global Hematocrit Test Devices Market strengthen their presence by investing heavily in research and development to enhance device accuracy, processing speed, and usability. They are expanding their product portfolios to include portable, point-of-care, and automated systems tailored to hospital, laboratory, and emergency settings. Strategic partnerships with healthcare providers, distributors, and diagnostic laboratories help improve market access and reach. Firms focus on expanding geographic coverage, entering emerging markets, and offering training and after-sales support to build customer loyalty. Product differentiation through compact design, digital integration, and workflow optimization ensures sustained adoption, while ongoing technological innovation and marketing initiatives maintain competitive positioning and long-term growth.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Modality trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of anemia and other blood disorders

- 3.2.1.2 Growing demand for point-of-care (POC) diagnostic testing

- 3.2.1.3 Technological advancements in hematology analyzers and diagnostic devices

- 3.2.1.4 Expansion of healthcare infrastructure and diagnostic laboratories

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced hematocrit testing devices

- 3.2.2.2 Risk of inaccurate results due to improper usage or environmental factors

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of hematocrit testing in emerging markets with high anemia burden

- 3.2.3.2 Growing adoption of portable and handheld hematocrit testing devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by primary research)

- 3.6 Future market trends (Driven by primary research)

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Customer insights (Driven by primary research)

- 3.10 Start-up scenarios (Driven by primary research)

- 3.11 Investment landscape (Driven by primary research)

- 3.12 Impact of AI and its future assessment

- 3.13 Value chain analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.2.1 Hematocrit test analyzer

- 5.2.2 Hematocrit test meter

- 5.3 Reagents and consumables

Chapter 6 Market Estimates and Forecast, By Modality, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Laboratory-based testing

- 6.3 Point-of-care (POC) testing

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Anemia

- 7.3 Congenital heart diseases

- 7.4 Polycythemia vera

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 A. Menarini

- 10.2 Abbott

- 10.3 BIO-RAD

- 10.4 Boule

- 10.5 Danaher

- 10.6 Diatron

- 10.7 EKF Diagnostics

- 10.8 HORIBA Medical

- 10.9 Mindray

- 10.10 NIHON KOHDEN

- 10.11 Nova Biomedical

- 10.12 Roche

- 10.13 SENSA CORE

- 10.14 Siemens Healthineers

- 10.15 Sysmex