PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019213

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019213

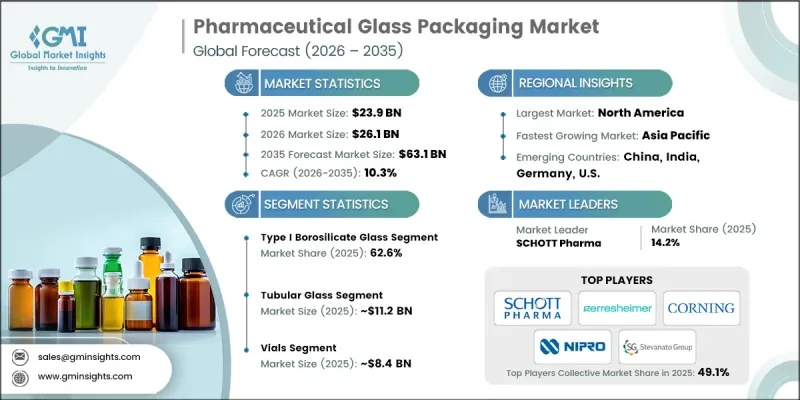

Pharmaceutical Glass Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Pharmaceutical Glass Packaging Market was valued at USD 23.9 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 63.1 billion by 2035.

The pharmaceutical glass packaging market is being driven by the rising need for high-quality packaging that ensures product integrity and stability. Increasing demand for pharmaceutical products, supported by demographic shifts and a growing burden of long-term health conditions, is accelerating industry expansion. Glass remains a preferred material due to its superior chemical resistance and ability to maintain drug efficacy over time. Manufacturers are focusing on developing advanced packaging solutions that combine durability with improved performance. Continuous innovation in lightweight, break-resistant, and environmentally sustainable glass materials is enhancing safety standards while meeting regulatory expectations. These developments are strengthening the role of glass packaging as a critical component in pharmaceutical supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.9 Billion |

| Forecast Value | $63.1 Billion |

| CAGR | 10.3% |

The pharmaceutical glass packaging market is also influenced by strict regulatory requirements focused on ensuring drug safety and preventing contamination. Global health authorities are enforcing comprehensive standards that require packaging materials to maintain product stability under various conditions. This has encouraged a shift toward higher-grade materials, particularly those offering enhanced chemical resistance and thermal stability. As a result, manufacturers are increasingly adopting advanced glass compositions to meet compliance standards and improve overall packaging reliability.

In 2025, the Type I borosilicate glass segment held a 62.6% share. This segment is gaining strong traction due to its superior resistance to chemical interactions and its ability to maintain stability under varying temperature conditions. The growing demand for sensitive pharmaceutical formulations is further supporting the adoption of this material. Regulatory requirements emphasizing the use of high-performance packaging materials are also contributing to the increased utilization of Type I borosilicate glass across the industry.

The tubular glass segment reached USD 11.2 billion in 2025. This segment is widely recognized for its precision, durability, and compatibility with advanced pharmaceutical applications. Its consistent structural properties and high resistance to chemical reactions make it suitable for critical packaging needs. Additionally, its compatibility with automated production systems has increased its adoption, allowing manufacturers to achieve greater efficiency and maintain product quality across large-scale operations.

North America Pharmaceutical Glass Packaging Market accounted for 35.3% share in 2025. The region is characterized by a strong focus on quality standards, regulatory compliance, and sustainable manufacturing practices. Increasing demand for advanced pharmaceutical packaging solutions is encouraging the adoption of high-purity glass materials and innovative coating technologies. The growing emphasis on product safety and contamination prevention is further supporting the use of high-performance glass packaging solutions. Additionally, government initiatives promoting sustainable materials are reinforcing the shift toward advanced glass packaging across the region.

Key companies operating in the Global Pharmaceutical Glass Packaging Market include Ardagh Group S.A., Beatson Clark Ltd., Bormioli Pharma S.p.A., Corning Incorporated, DWK Life Sciences GmbH, Gerresheimer AG, Hindustan National Glass & Industries Ltd., Nipro Corporation, Owens Illinois, Inc., Piramal Glass Limited, Schott AG, SGD Pharma (SGD S.A.), Shandong Pharmaceutical Glass Co., Ltd., Stevanato Group S.p.A., and Stolzle Glass Group. Companies in the Global Pharmaceutical Glass Packaging Market are strengthening their market position through continuous innovation, strategic collaborations, and capacity expansion. They are investing in research and development to create advanced glass formulations with improved chemical resistance and durability. Partnerships with pharmaceutical manufacturers are enabling better alignment with evolving packaging requirements. Companies are also expanding production capabilities to meet rising global demand and ensure a consistent supply. Sustainability initiatives, including the development of lightweight and recyclable glass solutions, are becoming a key focus area.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Manufacturing process trends

- 2.2.3 Product type trends

- 2.2.4 Drug delivery route trends

- 2.2.5 End user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent Regulations on Drug Safety

- 3.2.1.2 Aging Population and Chronic Disease

- 3.2.1.3 Rising Global Pharmaceutical Demand

- 3.2.1.4 Technological Advancement in Glass Packaging

- 3.2.1.5 Preference for Ready to Use Packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fragility and Breakage Risks

- 3.2.2.2 High Cost of Glass Packaging

- 3.2.3 Market opportunities

- 3.2.3. 1 Adoption of Sustainable and Eco-Friendly Glass Packaging Solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Billion & Million Units)

- 5.1 Key trends

- 5.2 Type I Borosilicate Glass

- 5.3 Type II Treated Soda Lime Glass

- 5.4 Type III Regular Soda Lime Glass

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Billion & Million Units)

- 6.1 Key trends

- 6.2 Tubular Glass

- 6.3 Molded Glass

Chapter 7 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion & Million Units)

- 7.1 Key trends

- 7.2 Vials

- 7.3 Bottles

- 7.4 Ampoules

- 7.5 Cartridges & Syringes

Chapter 8 Market Estimates and Forecast, By Drug Delivery Route, 2022 - 2035 (USD Billion & Million Units)

- 8.1 Key trends

- 8.2 Injectable Drugs

- 8.3 Oral Drugs

- 8.4 Ophthalmic Drugs

- 8.5 Topical Drugs

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion & Million Units)

- 9.1 Key trends

- 9.2 Pharmaceutical Companies

- 9.3 Contract Manufacturing Organizations

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players:

- 11.1.1 Ardagh Group S.A.

- 11.1.2 Bormioli Pharma S.p.A.

- 11.1.3 Corning Incorporated

- 11.1.4 Gerresheimer AG

- 11.1.5 Nipro Corporation

- 11.1.6 Owens-Illinois, Inc.

- 11.1.7 SCHOTT AG

- 11.1.8 SGD Pharma (SGD S.A.)

- 11.1.9 Stevanato Group S.p.A.

- 11.1.10 Stolzle Glass Group

- 11.2 Regional Players:

- 11.2.1 Beatson Clark Ltd.

- 11.2.2 DWK Life Sciences / DWK Life Sciences GmbH

- 11.2.3 Shandong Pharmaceutical Glass Co., Ltd.

- 11.3 Local Players:

- 11.3.1 Hindustan National Glass & Industries Ltd.

- 11.3.2 Piramal Glass Limited