PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019216

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019216

Industrial Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

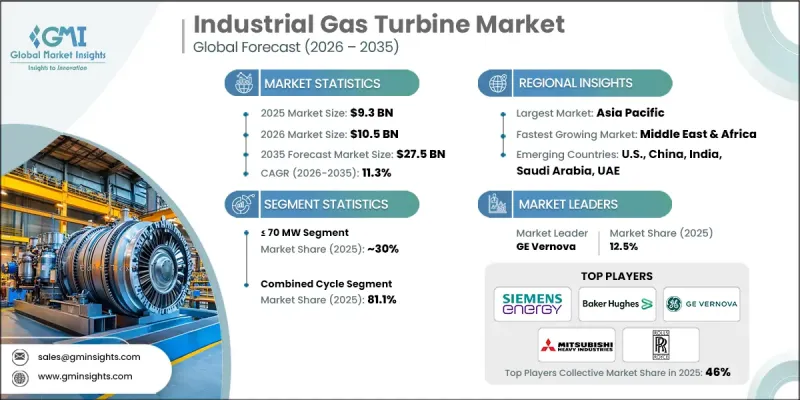

The Global Industrial Gas Turbine Market was valued at USD 9.3 billion in 2025 and is estimated to grow at a CAGR of 11.3% to reach USD 27.5 billion by 2035.

The market growth is fueled by stricter environmental regulations and the increasing adoption of low-emission technologies. The integration of digital monitoring solutions and predictive maintenance is enhancing system reliability, driving further industry expansion. Industrial gas turbines are high-power generation systems widely utilized in industries to deliver either mechanical or electrical output. Operating on the Brayton cycle, these turbines mix compressed air and fuel to produce efficient rotational energy. The adoption of combined cycle power plants is growing due to rising energy-efficiency requirements and sustainability initiatives. Gas turbines are favored for their fuel flexibility, advanced control systems, low emissions, and operational reliability. Rising renewable energy penetration is creating demand for reliable, dispatchable power to complement variable solar and wind generation, while coal plant retirements and brownfield grid connections are strengthening market prospects.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.3 Billion |

| Forecast Value | $27.5 Billion |

| CAGR | 11.3% |

The >70 MW - 300 MW segment accounted for USD 3.4 billion in 2025, primarily driven by medium-sized utilities that operate between large baseload plants and smaller distributed generation systems. These turbines are highly valued for their ability to provide flexible grid support, maintain stability during peak load periods, and enable efficient management of intermediate energy demands. Their adaptability makes them ideal for industrial operations and utility grids requiring rapid ramp-up and ramp-down capabilities to respond to fluctuations in energy demand. Additionally, the segment benefits from growing adoption in regions transitioning to cleaner energy sources, where these turbines can complement renewable power and ensure uninterrupted electricity supply. The segment's growth is also propelled by increasing investments in retrofitting and modernizing existing power infrastructure to improve energy efficiency and emissions performance, further reinforcing its market relevance.

The open cycle technology segment is projected to grow at a CAGR of 11.5% by 2035, supported by the rising need for distributed power solutions and enhanced grid stability in industrial and commercial operations. Open cycle turbines are gaining traction due to their fast start-up times, operational simplicity, and cost-effectiveness compared to combined cycle systems, making them suitable for peak load management and emergency backup applications. Continuous engineering innovations, including advanced turbine blade design, enhanced combustion techniques, and integration with digital monitoring systems, are improving fuel efficiency and lowering emissions. Compliance with stricter environmental regulations and the push for low-carbon energy generation further drives adoption of open cycle solutions. The growing industrial demand for modular, scalable power generation units ensures long-term expansion potential for this segment across both developed and emerging markets.

U.S. Industrial Gas Turbine Market accounted for 70% share, generating USD 1,383.7 million in 2025. Utilities across the U.S. increasingly depend on these turbines for rapid-response power to balance intermittent renewable energy sources such as solar and wind, ensuring consistent grid stability. The high penetration of renewable energy and ongoing modernization of the national grid has made flexible gas turbines critical for peak shaving, load balancing, and emergency backup. Moreover, U.S. industrial and commercial sectors are investing in high-efficiency turbines capable of reducing emissions while maintaining reliable power output. The market is also supported by government incentives for low-emission technologies, the retirement of older fossil fuel plants, and rising industrial energy demand, positioning the U.S. as a leading hub for industrial gas turbine deployment.

Major players in the Global Industrial Gas Turbine Market include Destinus Energy, Rolls Royce, Mitsubishi Heavy Industries, IHI Corporation, Solar Turbines, GE Vernova, Auxitrol Weston, Wartsila, Baker Hughes, Doncasters Group, Ansaldo Energia, Flex Energy Solutions, FUJI INDUSTRIES, Siemens Energy, VERICOR, Bharat Heavy Electricals, Doosan Enerbility, Everllence, Kawasaki Heavy Industries, and MTU Aero Engines. Companies in the Industrial Gas Turbine Market are strengthening their presence by investing in R&D to improve turbine efficiency, emissions control, and fuel flexibility. They are forming strategic partnerships with utilities, EPC contractors, and renewable energy providers to expand market reach. Manufacturers are also focusing on digitalization, including predictive maintenance and remote monitoring, to enhance reliability and customer support. Product customization, after-sales service, and long-term maintenance contracts are being leveraged to retain clients and secure recurring revenue streams. Geographic expansion, especially in emerging markets with rising energy demand, and participation in government clean energy programs are additional strategies used to solidify market foothold and capture long-term growth opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Capacity trends

- 2.1.3 Product trends

- 2.1.4 Technology trends

- 2.1.5 Application trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/MW)

- 3.5.1 By region

- 3.5.2 By capacity

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of industrial gas turbines

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 70 MW

- 5.3 > 70 MW - 300 MW

- 5.4 > 300 MW

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Aero-derivative

- 6.3 Heavy duty

Chapter 7 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Open cycle

- 7.3 Combined cycle

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 Power generation

- 8.3 Oil & gas

- 8.4 Other manufacturing

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Russia

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 Japan

- 9.4.4 India

- 9.4.5 South Korea

- 9.4.6 Indonesia

- 9.4.7 Thailand

- 9.4.8 Malaysia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Kuwait

- 9.5.5 Oman

- 9.5.6 Egypt

- 9.5.7 Turkey

- 9.5.8 Bahrain

- 9.5.9 Iraq

- 9.5.10 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Peru

- 9.6.4 Chile

Chapter 10 Company Profiles

- 10.1 Ansaldo Energia

- 10.2 Auxitrol Weston

- 10.3 Baker Hughes

- 10.4 Bharat Heavy Electricals

- 10.5 Destinus Energy

- 10.6 Doncasters Group

- 10.7 Doosan Enerbility

- 10.8 Everllence

- 10.9 Flex Energy Solutions

- 10.10 FUJI INDUSTRIES

- 10.11 GE Vernova

- 10.12 IHI Corporation

- 10.13 Kawasaki Heavy Industries

- 10.14 Mitsubishi Heavy Industries

- 10.15 MTU Aero Engines

- 10.16 Rolls Royce

- 10.17 Siemens Energy

- 10.18 Solar Turbines

- 10.19 VERICOR

- 10.20 Wartsila