PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019235

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019235

Automotive Fuel Feed Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

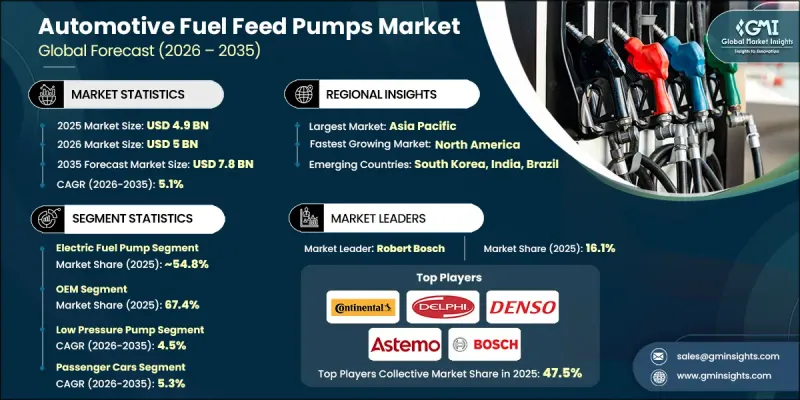

The Global Automotive Fuel Feed Pumps Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 7.8 billion by 2035.

Market growth remains closely tied to the continued production and demand for internal combustion engine vehicles, as fuel feed pumps play a critical role in ensuring precise fuel delivery in both gasoline and diesel systems. Rising urbanization and the expansion of middle-income populations across developing regions are contributing to increased vehicle ownership, particularly in cost-sensitive markets where conventional fuel-powered vehicles remain more accessible than alternative technologies. The automotive manufacturing sector continues to expand across emerging economies, creating sustained demand for essential engine components. While advancements in mobility solutions are gradually reshaping the industry, traditional powertrain systems continue to hold a strong presence due to infrastructure limitations and cost considerations. As a result, fuel feed pumps remain a vital component within the automotive value chain, supporting efficiency, performance, and operational reliability across a wide range of vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 5.1% |

Diesel-powered engines continue to play a significant role in global transportation, particularly within commercial vehicle segments. Despite gradual shifts in regulatory frameworks, internal combustion engine vehicles are expected to maintain relevance in several regions where emission regulations are less restrictive. Many developing economies continue to depend heavily on gasoline and diesel vehicles due to affordability and infrastructure readiness. Although certain regions are accelerating the transition toward cleaner mobility solutions, broader adoption of alternative technologies is still evolving, allowing conventional vehicle systems to sustain demand over the forecast period.

The electric fuel pump segment held a 54.8% share in 2025, generating USD 2.7 billion. These pumps are widely preferred due to their ability to maintain consistent fuel pressure and optimize delivery performance, which is essential for modern engine systems utilizing electronic fuel injection. Unlike mechanical variants, electric pumps operate independently of engine speed, contributing to improved efficiency, enhanced engine performance, and better alignment with emission requirements. These advantages have positioned electric fuel pumps as a preferred choice among manufacturers.

The OEM segment held a 67.4% share in 2025, generating USD 3.3 billion. Growth in vehicle production continues to strengthen this segment, as original equipment manufacturers supply fuel feed pumps directly for new vehicle assembly. Increasing reliance on advanced fuel delivery systems has led manufacturers to prioritize sourcing components from approved suppliers, ensuring quality and performance standards. This trend supports the expansion of OEM-driven sales channels, which continue to outperform aftermarket demand due to consistent integration in new vehicle production.

United States Automotive Fuel Feed Pumps Market reached USD 820.7 million in 2025 and is projected to grow at a CAGR of 6.1% from 2026 to 2035. Market performance in the region remains closely aligned with the production and sales of internal combustion engine vehicles. Although the adoption of alternative propulsion technologies is gradually increasing, conventional vehicles continue to represent a significant share of the overall fleet. This sustained presence supports ongoing demand for fuel feed pumps across both gasoline and diesel applications. North America remains a key regional market, with the United States contributing a substantial portion of overall demand.

Key companies operating in the Global Automotive Fuel Feed Pumps Market include Aisin, Carter Fuel Systems, Continental, Delphi, Denso, Hitachi Astemo, Magneti Marelli, Robert Bosch, TI Automotive (AVIC), and Walbro. Companies in the Automotive Fuel Feed Pumps Market are strengthening their competitive position through continuous product innovation, strategic collaborations, and expansion into high-growth regions. A key focus is being placed on developing advanced fuel delivery systems that enhance efficiency and meet evolving emission standards. Manufacturers are investing in research and development to improve durability, precision, and integration with modern engine technologies. Partnerships with automotive manufacturers are helping secure long-term supply agreements and strengthen distribution networks. Additionally, companies are optimizing production capabilities and supply chain operations to remain cost-competitive. Expanding product portfolios and targeting emerging markets are also critical strategies being adopted to capture new growth opportunities and reinforce market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Pump

- 2.2.3 Pressure

- 2.2.4 Vehicle

- 2.2.5 Fuel

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production & sales

- 3.2.1.2 Stringent emission norms driving fuel injection technology adoption

- 3.2.1.3 Growing aftermarket demand due to aging vehicle fleet

- 3.2.1.4 Technological advancements in electric fuel pump systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid electrification of automotive industry

- 3.2.2.2 High cost of advanced high-pressure fuel pumps

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing vehicle ownership

- 3.2.3.2 Development of multi-fuel compatible pump systems

- 3.2.3.3 Aftermarket growth in developed markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - U.S. Environmental Protection Agency (EPA)

- 3.4.1.2 U.S. - California Air Resources Board (CARB)

- 3.4.1.3 Canada - Transport Canada

- 3.4.2 Europe

- 3.4.2.1 Germany - Kraftfahrt-Bundesamt (KBA)

- 3.4.2.2 UK - Vehicle Certification Agency (VCA)

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Ministry of Industry and Information Technology (MIIT)

- 3.4.3.2 India - Automotive Research Association of India (ARAI)

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Instituto Brasileiro do Meio Ambiente e dos Recursos Naturais Renovaveis (IBAMA)

- 3.4.4.2 Mexico - Secretaria de Medio Ambiente y Recursos Naturales (SEMARNAT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Saudi Arabia - Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.2 South Africa - South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Electric In-Tank Fuel Pumps

- 3.8.1.2 Mechanical Fuel Pumps

- 3.8.1.3 Variable Speed Fuel Pumps

- 3.8.2 Emerging technologies

- 3.8.2.1 Brushless Electric Fuel Pumps

- 3.8.2.2 Smart Fuel Pumps with Electronic Control

- 3.8.2.3 Multi-Fuel Compatible Pump Systems

- 3.8.1 Current technologies

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Cost breakdown analysis

- 3.15 Product lifecycle & upgrade cycles

- 3.15.1 Replacement Cycle Analysis by Vehicle Age & Region

- 3.15.2 Part Compatibility and Customization

- 3.16 Impact of electrification on fuel feed pumps

- 3.16.1 reduction in internal combustion engine (ICE) vehicle demand

- 3.16.2 Evolving fuel system technology for hybrid vehicles

- 3.16.3 Declining replacement frequency for EV components

- 3.17 Case studies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Pump, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical fuel pump

- 5.3 Electric fuel pump

- 5.3.1 In-tank electric pumps

- 5.3.2 In-line electric pumps

- 5.4 Turbo pump

Chapter 6 Market Estimates & Forecast, By Pressure, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Low pressure pump

- 6.3 High-pressure pump

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Gasoline/Petrol

- 8.3 Diesel

- 8.4 Alternative fuels

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.3.8 Norway

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Robert Bosch

- 11.1.2 Denso

- 11.1.3 Continental

- 11.1.4 Delphi

- 11.1.5 Walbro

- 11.1.6 HELLA

- 11.1.7 AC Delco (GM)

- 11.1.8 TI Automotive

- 11.1.9 Valeo

- 11.2 Regional players

- 11.2.1 Mikuni

- 11.2.2 Aisin

- 11.2.3 Magneti Marelli

- 11.2.4 GMB

- 11.2.5 Hitachi Astemo

- 11.2.6 Carter Fuel Systems

- 11.3 Emerging players

- 11.3.1 EKU

- 11.3.2 Spectra Premium

- 11.3.3 Holley

- 11.3.4 Fuelab

- 11.3.5 SHW