PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019247

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019247

Cardiovascular Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

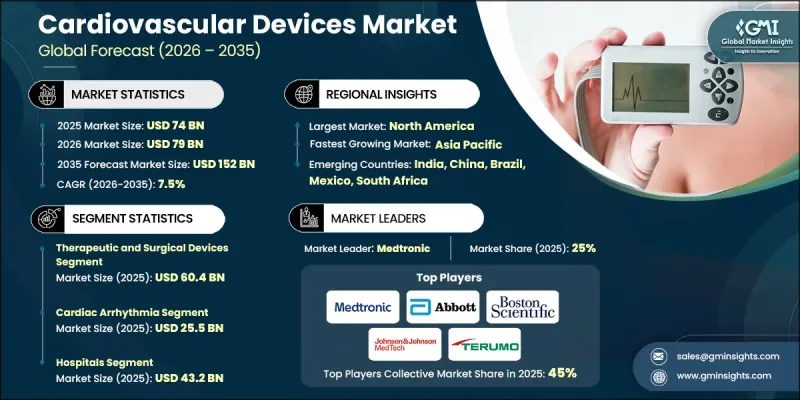

The Global Cardiovascular Devices Market was valued at USD 74 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 152 billion by 2035.

The expansion is fueled by the rising prevalence of cardiovascular diseases, an aging global population, increased government healthcare initiatives, and growing demand for minimally invasive interventions. Cardiovascular devices include implantable, external, and diagnostic systems that monitor, support, or restore heart and vascular function. They help detect irregularities, improve circulation, regulate heart rhythms, enhance blood flow, and assist in long-term disease management. Advancements in device technology, miniaturization, innovative materials, and digital integration have improved clinical precision, safety, and usability. Innovations like advanced stents, electrophysiology solutions, and imaging tools enable earlier detection and more effective treatment, encouraging physician adoption. Minimally invasive procedures, including transcatheter heart valves and robotic-assisted systems, reduce surgical trauma, shorten hospital stays, and lower treatment costs, prompting hospitals and cardiology centers to prioritize cutting-edge, precision-guided devices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $74 Billion |

| Forecast Value | $152 Billion |

| CAGR | 7.5% |

The therapeutic and surgical devices segment reached USD 60.4 billion in 2025. This segment encompasses essential cardiovascular tools such as catheters, coronary intervention devices, cardiac rhythm management systems, structural heart devices, and surgical instruments. These devices play a critical role in restoring or replacing heart function and are central to interventional cardiology and cardiac surgery. The segment dominates due to its provision of definitive treatments, often necessary for urgent or life-threatening cardiac conditions. Continuous product innovations, including minimally invasive catheters, next-generation stents, smarter rhythm management devices, and durable heart valves, enhance procedural outcomes, reduce hospital stays, and expand eligibility for high-risk patients.

The cardiac arrhythmia segment generated USD 25.5 billion in 2025. Arrhythmia-focused devices hold a major share because of the increasing prevalence of irregular heart rhythms such as atrial fibrillation, tachycardia, and bradycardia. Aging populations, lifestyle-related risk factors like obesity, hypertension, and diabetes, and the rising need for continuous monitoring drive sustained demand. Technological progress in arrhythmia detection and therapy, including advanced monitoring systems and implantable devices, strengthens the segment's market position and supports long-term growth.

North America Cardiovascular Devices Market accounted for 41.8% share in 2025. The region's high disease burden, driven by sedentary lifestyles, obesity, and hypertension, fuels strong demand for advanced diagnostic and therapeutic solutions. Hospitals and specialty centers increasingly adopt minimally invasive cardiac devices, such as stents, pacemakers, defibrillators, and monitoring systems, to treat a growing patient population. Rising CVD-related hospitalizations accelerate the adoption of innovative interventional devices, while continuous improvements in cardiology equipment align with the region's healthcare needs and regulatory standards.

Key players in the Global Cardiovascular Devices Market include Abbott Laboratories, Boston Scientific, Biotronik, Johnson & Johnson MedTech, Terumo, AngioDynamics, Olympus, Medtronic, Meril Life Sciences, Penumbra, Sahajanand Medical Technologies, Koninklijke Philips, Translumina Therapeutics, Relisys Medical Devices, and MicroPort Scientific. Companies in the Global Cardiovascular Devices Market strengthen their position by prioritizing innovation and expanding their product portfolios to include advanced, minimally invasive, and digitally integrated devices. Firms invest heavily in R&D to develop next-generation stents, rhythm management systems, structural heart devices, and robotic-assisted technologies. Strategic partnerships with hospitals and research institutions accelerate clinical adoption and market penetration. Global expansion into emerging markets and targeted collaborations with distributors ensure wider geographic reach. Companies also focus on regulatory compliance, quality assurance, and physician training programs to build trust and drive adoption.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Device type trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

- 3.2.1.2 Expanding geriatric population

- 3.2.1.3 Rising government initiatives

- 3.2.1.4 Technological advancements in cardiovascular devices

- 3.2.1.5 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk associated with cardiac procedures

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing applications of AI in cardiovascular diseases

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 Advanced imaging and sensing systems for real-time cardiovascular diagnostics

- 3.5.1.2 AI-integrated cardiovascular devices for automated detection and risk stratification

- 3.5.2 Emerging technologies

- 3.5.2.1 Bioengineered and adaptive materials for next-generation cardiovascular implants and stents

- 3.5.2.2 Ultra-high-speed 3D visualization and digital twin technologies for dynamic cardiovascular assessment

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Pricing analysis, 2025

- 3.8 Impact of AI and Generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostic and monitoring devices

- 5.2.1 Electrocardiogram systems

- 5.2.2 Holter and event monitors

- 5.2.3 Remote cardiac monitoring devices

- 5.2.4 Cardiac diagnostic ultrasound

- 5.2.5 Other diagnostic and monitoring devices

- 5.3 Therapeutic and surgical devices

- 5.3.1 Catheters

- 5.3.1.1 Electrophysiology ablation catheters

- 5.3.1.2 Electrophysiology diagnostic and mapping catheters

- 5.3.1.3 Interventional catheters

- 5.3.2 Coronary intervention devices

- 5.3.2.1 Drug eluting stents

- 5.3.2.2 Bare metal stents

- 5.3.2.3 Bioresorbable scaffolds

- 5.3.2.4 PTCA balloons

- 5.3.2.5 Atherectomy devices

- 5.3.2.6 Guidewires

- 5.3.2.7 Embolic protection devices

- 5.3.2.8 Other coronary intervention devices

- 5.3.3 Cardiac rhythm management (CRM) devices

- 5.3.3.1 Pacemakers

- 5.3.3.2 Implantable cardioverter defibrillators

- 5.3.3.3 Cardiac resynchronization therapy devices

- 5.3.3.4 Implantable loop recorders

- 5.3.3.5 Other cardiac rhythm management devices

- 5.3.4 Structural heart devices

- 5.3.4.1 LAA closure devices

- 5.3.4.2 Heart valves

- 5.3.5 Cardiac surgery devices

- 5.3.5.1 Coronary artery bypass graft (CABG) surgical tools

- 5.3.5.2 Other cardiac surgical devices

- 5.3.6 Ventricular assist devices

- 5.3.1 Catheters

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease

- 6.3 Cardiac arrhythmia

- 6.4 Heart failure

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Cardiac centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AngioDynamics

- 9.3 Biotronik

- 9.4 Boston Scientific

- 9.5 Johnson & Johnson MedTech

- 9.6 Koninklijke Philips

- 9.7 Medtronic

- 9.8 Meril Life Sciences

- 9.9 MicroPort Scientific

- 9.10 Olympus

- 9.11 Penumbra

- 9.12 Relisys Medical Devices

- 9.13 Sahajanand Medical Technologies

- 9.14 Terumo

- 9.15 Translumina Therapeutics