PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027447

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027447

Asia-Pacific Tea Processing Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

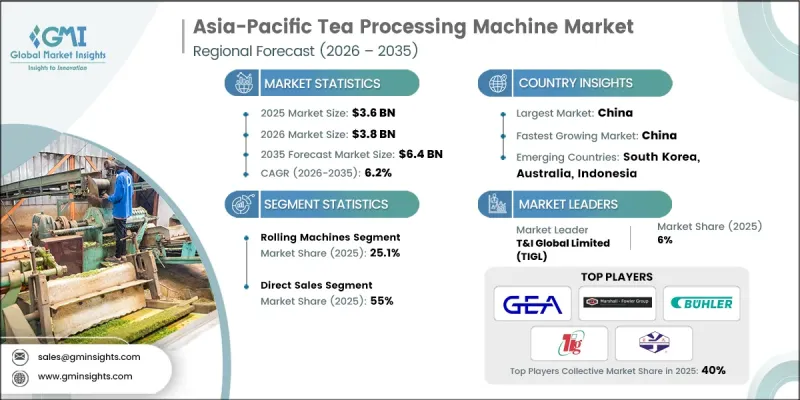

Asia Pacific Tea Processing Machine Market was valued at USD 3.6 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 6.4 billion by 2035.

The expansion is driven by rising tea consumption across the region, particularly for specialty and organic varieties, coupled with the modernization of production processes. Automation, robotics, and artificial intelligence are transforming manufacturing, reducing labor costs, and improving product quality. The market is further supported by the introduction of advanced machinery, including smart rolling equipment, continuous dryers, and AI-powered sorting systems. Despite challenges such as supply chain disruptions, geopolitical tensions in tea-producing regions, and climate-related risks, the adoption of energy-efficient machinery and IoT-enabled solutions is creating significant opportunities. Manufacturers in China, India, and Sri Lanka are at the forefront of launching innovative solutions, which are shaping the competitive landscape and driving steady market growth across the Asia Pacific region.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 6.2% |

The rolling machines segment accounted for 25.1% share in 2025 and continues to lead due to their ability to process a wide variety of teas, including green, black, and specialty blends. These machines are preferred for their ability to preserve aroma and flavor while maximizing production efficiency. Their strong performance and reliability have made them a cornerstone in professional tea production, driving consistent demand and maintaining a substantial market share.

In 2025, the direct sales segment held 55% share, highlighting the preference of large estates and manufacturing plants for high-value, custom-engineered solutions. Direct channels provide end-users with personalized machine specifications, factory warranties, and complex system installations, ensuring seamless integration into production processes. Distribution networks and dealer partnerships further enhance accessibility, offering technical support, after-sales services, and local expertise, which strengthens customer satisfaction and loyalty.

China Tea Processing Machine Market reached USD 3.6 billion in 2025 with a projected CAGR of 6.2% through 2035. Growth is driven by the modernization of traditional tea estates, infrastructure improvements in key tea-producing regions, and increasing investments in advanced processing techniques such as CTC and orthodox methods. Automation and AI-driven sorting technologies are being adopted to reduce labor costs, enhance leaf grading, and improve overall operational efficiency, positioning China as a key hub for both production and consumption.

Major players in the Asia Pacific Tea Processing Machine Market include Buhler Group, T&I Global Limited (TIGL), GEA Group, Marshall Fowler Engineers India (P) Ltd., Esal Tea Machinery, G.K. Tea Industries (KETCO), Hangzhou Chama Machinery Co., Ltd., Jiangsu Hongda Powder Equipment Co., Ltd., Quanzhou Deli Agroforestrial Machinery Co., Ltd., Stesalit Automation, Surya Industries, Tailift Group, Tea Engineering Works (TEW), Thyssenkrupp Industrial Solutions, and Zenith Forgings. Companies in the Asia Pacific Tea Processing Machine Market are strengthening their presence by prioritizing product innovation, technological upgrades, and operational efficiency. Firms are investing heavily in AI-enabled, energy-efficient, and IoT-integrated machinery to meet evolving industry requirements. Expansion of distribution networks and dealer partnerships allows wider market access and localized technical support. Strategic collaborations, mergers, and acquisitions enhance global reach, while customized solutions and precision-engineered equipment cater to high-value clients. Additionally, companies are adopting sustainable production practices, improving reliability, and offering comprehensive after-sales services to build long-term customer loyalty and maintain a competitive advantage in the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Machine Type

- 2.2.3 Automation Level

- 2.2.4 Tea Type

- 2.2.5 End User

- 2.2.6 Functionality

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for specialty & premium teas

- 3.2.1.2 Modernization of traditional tea estates

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Vulnerability to climate & supply fluctuations

- 3.2.3 Opportunities

- 3.2.3.1 Smart technology & IoT integration

- 3.2.3.2 Energy-efficient drying & heating solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (APAC Markets) (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (2022-2024) by Country (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Chinese Value Players vs. Japanese Premium) (Driven by Primary Research)

- 3.6.3 Price Variation by Machine Type & Automation Level

- 3.6.4 Country-Level Price Benchmarking (India, China, Sri Lanka, Vietnam)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis (2019-2024) (Driven by Primary Research)

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.8.3 Price Variation by Machine Type & Automation Level

- 3.8.4 Regional Price Benchmarking

- 3.8.5 Impact of Raw Material Costs on Equipment Pricing

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis (Driven by Primary Research)

- 3.11.1 Trade Data Analysis (Intra-APAC & APAC Trade Flows) (Driven by Primary Research)

- 3.11.2 Import/Export Volume & Value Trends (2022-2024) (Driven by Primary Research)

- 3.11.3 Key Trade Corridors (China-India, China-Vietnam, etc.) (Driven by Primary Research)

- 3.11.4 Top Exporting Countries (China, Japan, South Korea)

- 3.11.5 Top Importing Countries (India, Vietnam, Indonesia, Sri Lanka)

- 3.12 Impact of AI & Generative AI on the APAC Tea Processing Market

- 3.12.1 AI-Driven Disruption of Traditional Processing Methods

- 3.12.2 GenAI Use Cases in Equipment Design & Predictive Maintenance

- 3.12.3 AI-Enabled Quality Control & Optimization

- 3.12.4 Adoption Roadmap by End-User Segment

- 3.12.5 Risks, Limitations & Regulatory Considerations

- 3.13 Capacity & Production Landscape (APAC) (Driven by Primary Research)

- 3.13.1 Installed Manufacturing Capacity by Country & Key Producer (Driven by Primary Research)

- 3.13.1.1 China

- 3.13.1.2 India

- 3.13.1.3 Japan

- 3.13.1.4 South Korea

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

- 3.13.3 Tea Processing Infrastructure Modernization Initiatives by Country

- 3.13.4 Local vs. Multinational Manufacturing Footprint

- 3.13.1 Installed Manufacturing Capacity by Country & Key Producer (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Rolling machines

- 5.3 CTC (Crush, Tear, Curl) machines

- 5.4 Drying machines

- 5.5 Sorting and grading machines

- 5.6 Blending machines

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Automation Level, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual machines

- 6.3 Semi-automatic machines

- 6.4 Fully automatic machines

Chapter 7 Market Estimates & Forecast, By Tea Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Black tea processing

- 7.3 Green tea processing

- 7.4 Oolong tea processing

- 7.5 Herbal and specialty tea processing

Chapter 8 Market Estimates & Forecast, By End User, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Tea plantations

- 8.3 Tea processing factories

- 8.4 Tea packaging companies

- 8.5 Tea exporters

Chapter 9 Market Estimates & Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 China

- 11.3 Japan

- 11.4 India

- 11.5 Australia

- 11.6 South Korea

- 11.7 Taiwan

- 11.8 Malaysia

- 11.9 Indonesia

Chapter 12 Company Profiles

- 12.1 Buhler Group

- 12.2 T&I Global Limited (TIGL)

- 12.3 GEA Group

- 12.4 Marshall Fowler Engineers India (P) Ltd.

- 12.5 Esal Tea Machinery

- 12.6 G.K. Tea Industries (KETCO)

- 12.7 Hangzhou Chama Machinery Co., Ltd.

- 12.8 Jiangsu Hongda Powder Equipment Co., Ltd.

- 12.9 Quanzhou Deli Agroforestry Machinery Co., Ltd.

- 12.10 Stesalit Automation

- 12.11 Surya Industries

- 12.12 Tailift Group

- 12.13 Tea Engineering Works (TEW)

- 12.14 Thyssenkrupp Industrial Solutions

- 12.15 Zenith Forgings