PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027452

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027452

North America Electric Tractor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

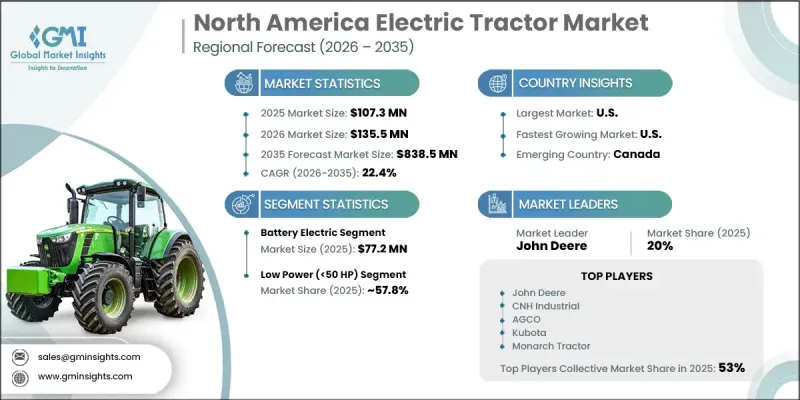

North America Electric Tractor Market was valued at USD 107.3 million in 2025 and is estimated to grow at a CAGR of 22.4% to reach USD 838.5 million by 2035.

The industry is steadily transitioning from a niche innovation space into a practical and commercially relevant solution across agricultural and utility sectors. Market momentum is being driven by increasing pressure to meet environmental standards, the rising cost burden associated with diesel-powered equipment, and ongoing advancements in electric propulsion systems. Although adoption levels remain relatively low compared to conventional tractors, demand is steadily increasing among smaller farming operations, specialized agricultural producers, and public-sector users. This evolving landscape signals a long-term structural move toward cleaner mechanization, supported by favorable policy frameworks and improving cost dynamics at the operational level.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $107.3 Million |

| Forecast Value | $838.5 Million |

| CAGR | 22.4% |

Tightening emission standards and environmentally focused agricultural regulations are significantly influencing adoption trends across North America. Government initiatives at both the federal and state levels are actively encouraging emission reductions in traditionally diesel-intensive sectors. Electric tractors provide a viable solution by removing direct emissions and lowering operational noise, making them increasingly suitable for areas with stricter environmental considerations. As sustainability metrics gain importance throughout agricultural supply chains, purchasing decisions are increasingly shaped by environmental performance alongside efficiency.

The battery electric tractors segment generated USD 77.2 million in 2025. Their leading position is attributed to their relatively advanced development stage and stronger commercial readiness. These models offer streamlined mechanical design, reduced servicing needs, and improved energy efficiency compared to hybrid or alternative fuel technologies. Their capabilities align well with operational environments that benefit from consistent usage patterns and accessible charging solutions.

The segment below 50 HP accounted for 57.8% share in 2025, making it the leading category by power output. This trend highlights the compatibility between current electric tractor capabilities and the performance needs of lower-intensity operations. Equipment in this category is widely utilized for lighter workloads, where battery efficiency and manageable energy requirements support effective performance.

United States Electric Tractor Market held a 76% share, generating USD 81.3 million in 2025. This dominance is supported by well-established agricultural systems, a higher rate of technology integration, and strong alignment with sustainability-driven policies. The presence of large-scale farming enterprises and institutional buyers with greater investment capacity further accelerates adoption. Additionally, a robust ecosystem that includes established distribution channels, financing structures, and service networks continues to facilitate market growth.

Key companies shaping the competitive landscape include AGCO, Autonomous Tractor Corporation, Bobcat, CLAAS, CNH Industrial, Electric Tractor Corporation, John Deere, Kubota, Mahindra & Mahindra, Monarch Tractor, NAIO Technologies, Sabanto, Solectrac, Tilmor, and Yanmar. Companies operating in the North America Electric Tractor Market are focusing on innovation, strategic partnerships, and product diversification to strengthen their market position. Many players are investing heavily in research and development to enhance battery performance, extend operating hours, and improve overall efficiency. Collaborations with technology providers are helping to integrate automation and smart farming capabilities into electric models. Firms are also expanding their distribution networks and after-sales services to improve customer accessibility and retention. Additionally, companies are targeting niche applications and smaller farm segments to accelerate adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion type

- 2.2.3 Battery

- 2.2.4 Power

- 2.2.5 Application

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory pressure and environmental compliance

- 3.2.1.2 Rising fuel and maintenance cost economics

- 3.2.1.3 Technological advancements and product commercialization

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital cost

- 3.2.2.2 Limited operational range and charging infrastructure

- 3.2.3 Opportunities

- 3.2.3.1 Integration with renewable energy systems

- 3.2.3.2 Expansion in specialty and urban agriculture

- 3.2.4 Growth potential analysis

- 3.2.5 Future market trends

- 3.2.6 Technology and innovation landscape

- 3.2.6.1 Current technological trends

- 3.2.6.2 Emerging technologies

- 3.2.7 Pricing Analysis (driven by primary research)

- 3.2.7.1 Historical price trend analysis

- 3.2.7.2 Regional price variations

- 3.2.7.3 Price Comparison: electric vs diesel tractors

- 3.2.7.4 Price elasticity & consumer sensitivity

- 3.2.8 Regulatory Framework

- 3.2.8.1 Emission standards & agricultural equipment regulations

- 3.2.8.2 Government subsidies & incentive programs

- 3.2.8.3 Safety & certification requirements

- 3.2.8.4 Import/export regulations & trade policies

- 3.2.8.5 Rural electrification policies

- 3.2.8.6 Carbon credit & sustainability mandates

- 3.2.9 Porter's five forces analysis

- 3.2.10 PESTEL analysis

- 3.2.11 Consumer behavior analysis

- 3.2.11.1 Purchasing patterns

- 3.2.11.2 Preference analysis

- 3.2.11.3 Regional variations in consumer behavior

- 3.2.11.4 Impact of e-commerce on buying decisions

- 3.2.12 Trade data analysis - HS Code: 8701.24 (new) (driven by paid database)

- 3.2.12.1 Import/export volume & value trends

- 3.2.12.2 Key trade corridors & tariff impact

- 3.2.12.3 Trade flow analysis

- 3.2.13 Impact of AI & generative AI on the market

- 3.2.13.1 AI-driven disruption of existing business models

- 3.2.13.2 GenAI use cases & adoption roadmap by segment

- 3.2.13.3 Precision agriculture integration (AI-enabled field optimization)

- 3.2.13.4 Predictive maintenance & fleet management applications

- 3.2.13.5 Risks, limitations & regulatory considerations

- 3.2.1 Growth drivers

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Battery electric

- 5.3 Hybrid electric

- 5.4 Fuel cell electric

Chapter 6 Market Estimates and Forecast, By Battery, 2022 - 2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Lithium-ion

- 6.3 Lead-Acid

- 6.4 Others (solid-state, sodium-ion, etc.)

Chapter 7 Market Estimates and Forecast, By Power, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Low power (<50 HP)

- 7.3 Medium power (50-100 HP)

- 7.4 High power (>100 HP)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Agriculture

- 8.2.1 Field operations

- 8.2.2 Orchard & vineyard operations

- 8.2.3 Livestock & dairy farm applications

- 8.2.4 Others

- 8.3 Utility

- 8.3.1 Landscaping & grounds maintenance

- 8.3.2 Golf courses & sports fields

- 8.3.3 Municipal & public spaces

- 8.4 Industrial

- 8.4.1 Construction site operations

- 8.4.2 Material handling & logistics

- 8.4.3 Municipal services & waste management

- 8.4.4 Airport & port operations

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 U.S.

- 10.3 Canada

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Autonomous Tractor Corporation

- 11.3 Bobcat

- 11.4 CLAAS

- 11.5 CNH Industrial

- 11.6 Electric Tractor Corporation

- 11.7 John Deere

- 11.8 Kubota

- 11.9 Mahindra & Mahindra

- 11.10 Monarch Tractor

- 11.11 NAIO Technologies

- 11.12 Sabanto

- 11.13 Solectrac

- 11.14 Tilmor

- 11.15 Yanmar