PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027483

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027483

Europe Forklift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

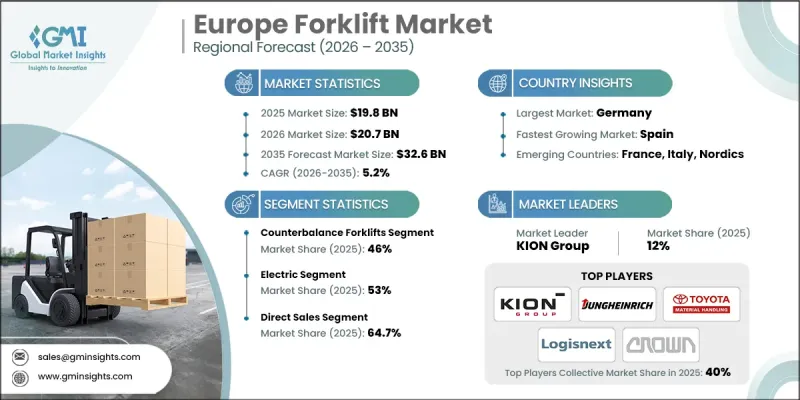

Europe Forklift Market was valued at USD 19.8 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 32.6 billion by 2035.

Continuous upgrades in logistics networks, manufacturing facilities, and warehouse operations drive the growth. Forklifts are becoming essential to improve operational efficiency, workplace safety, and overall productivity. As businesses optimize workflows, material handling equipment plays a central role in enabling smoother and more efficient processes. Environmental considerations are also influencing purchasing decisions, with organizations prioritizing cleaner and quieter equipment to align with sustainability goals. At the same time, the integration of digital technologies is transforming forklift operations, allowing for enhanced tracking, improved safety, and better fleet management. The rapid expansion of order fulfillment requirements is further supporting demand, as companies seek faster and more efficient ways to manage goods movement across complex supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.8 Billion |

| Forecast Value | $32.6 Billion |

| CAGR | 5.2% |

Shifting regulatory requirements and environmental priorities are reshaping the Europe forklift market, leading to a strong transition toward electric-powered equipment. Businesses are increasingly adopting advanced solutions that incorporate automation and smart technologies to enhance operational performance. The use of digital systems is enabling improved monitoring, reduced downtime, and optimized resource utilization. As operational efficiency becomes a key focus, companies are leveraging integrated technologies to streamline processes and achieve higher productivity levels across their facilities.

The counterbalance forklift segment accounted for 46% share in 2025, generating USD 9.1 billion. This segment continues to lead due to its versatility, ease of use, and ability to handle a wide range of material handling tasks. Its straightforward design allows it to operate efficiently across different environments, making it suitable for diverse industrial applications. The ability to manage varying load sizes and perform effectively in open workspaces further strengthens its position as a reliable and widely adopted solution.

The electric segment held a 53% share in 2025, generating USD 10.5 billion. Growth in this segment is being driven by increasing emphasis on sustainability, energy efficiency, and workplace safety. Electric forklifts are gaining preference due to their lower emissions, quieter operation, and reduced maintenance requirements. Their suitability for indoor environments and long-term cost advantages are encouraging widespread adoption among businesses seeking to optimize operational efficiency while meeting regulatory standards.

Germany Forklift Market held a 24% share, generating around USD 4.7 billion in 2025. The country's leadership is supported by its advanced industrial ecosystem, extensive manufacturing capabilities, and well-developed logistics infrastructure. High levels of industrial activity continue to drive consistent demand for material handling equipment. Ongoing investments in modern logistics systems and production efficiency are further reinforcing Germany's dominant position within the regional market.

Key companies operating in the Europe forklift market include Toyota Material Handling, KION Group, Jungheinrich, Hyster-Yale, Crown Equipment, Mitsubishi Logisnext, Komatsu, Hangcha Group, HELI (Anhui Heli), Manitou Group, Konecranes, Doosan Bobcat, Clark Material Handling, Combilift, and Palfinger. Companies in the Europe forklift market are strengthening their market presence through innovation, strategic expansion, and technology integration. Significant investments in research and development are enabling the introduction of advanced electric and automated forklift solutions. Businesses are focusing on incorporating digital technologies such as fleet management systems and real-time monitoring tools to enhance operational efficiency. Strategic partnerships and acquisitions are helping companies expand their geographic footprint and diversify product offerings. In addition, firms are prioritizing sustainability initiatives by developing energy-efficient equipment that meets regulatory standards. Enhanced after-sales services, customized solutions, and strong distribution networks are further supporting customer retention and long-term growth in a competitive market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 key trends

- 2.3 Product type

- 2.4 Fuel type

- 2.5 Load capacity

- 2.6 End use

- 2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component suppliers

- 3.1.2 Raw material providers

- 3.1.3 Manufacturers

- 3.1.4 Fuel and energy integrators

- 3.1.5 Technology providers

- 3.1.6 Distribution channels

- 3.1.7 End users

- 3.1.8 Aftermarket service providers

- 3.2 Profit margin analysis

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.3.3 Opportunities

- 3.4 Growth potential analysis

- 3.5 Technology & innovation landscape

- 3.5.1 Electric propulsion technology evolution

- 3.5.2 Lithium-ion vs. lead-acid battery systems

- 3.5.3 Hydrogen fuel cell development

- 3.5.4 Autonomous and AGV forklift technology

- 3.5.5 Telematics and fleet management systems

- 3.5.6 Fast-charging infrastructure

- 3.6 Regulatory landscape

- 3.6.1 EU emissions regulations and forklift standards

- 3.6.2 Workplace safety directives (EU and national)

- 3.6.3 Battery recycling and extended producer responsibility

- 3.6.4 Country-specific incentives for electric forklifts

- 3.7 Pricing analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (2022-2025)

- 3.7.2 Pricing strategy by player type (premium, value, cost-plus)

- 3.7.3 Regional price variations

- 3.7.4 Electric vs. ICE price parity analysis

- 3.8 Trade data analysis (driven by paid database)

- 3.8.1 Import and export volume and value trends (2022-2024)

- 3.8.2 Key trade corridors and tariff impact

- 3.8.3 Regional trade dynamics

- 3.9 Impact of AI and generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases and adopt roadmaps by segment

- 3.9.3 Risks, limitations, and regulatory considerations

- 3.10 Capacity and production landscape (driven by primary research)

- 3.10.1 Installed capacity by region and key producer

- 3.10.2 Capacity utilization rates and expansion pipelines

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Germany

- 4.2.2 UK

- 4.2.3 France

- 4.2.4 Italy

- 4.2.5 Spain

- 4.2.6 Russia

- 4.2.7 Nordics

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plan

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Counterbalance forklifts

- 5.3 Narrow aisle forklifts

- 5.4 Hand trucks & walkie forklifts

- 5.5 Rough terrain forklifts

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Fuel Type, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Electric

- 6.3 Diesel

- 6.4 Gasoline

- 6.5 LPG/CNG

Chapter 7 Market Estimates & Forecast, By Load Capacity, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Small

- 7.3 Medium

- 7.4 Large

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Logistics & warehousing

- 8.3 Retail & e-commerce

- 8.4 Manufacturing & industrial

- 8.5 Food & beverages

- 8.6 Chemical & pharmaceutical

- 8.7 Construction & mining

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 UK

- 10.3 Germany

- 10.4 France

- 10.5 Italy

- 10.6 Spain

- 10.7 Russia

- 10.8 Nordics

- 10.9 Rest of Europe

Chapter 11 Company Profiles

- 11.1 Clark Material Handling

- 11.2 Combilift

- 11.3 Crown Equipment

- 11.4 Doosan Bobcat

- 11.5 Hangcha Group

- 11.6 HELI (Anhui Heli)

- 11.7 Hyster-Yale

- 11.8 Jungheinrich

- 11.9 KION Group

- 11.10 Komatsu

- 11.11 Konecranes

- 11.12 Manitou Group

- 11.13 Mitsubishi Logisnext

- 11.14 Palfinger

- 11.15 Toyota Material Handling