PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027523

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027523

Automotive Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

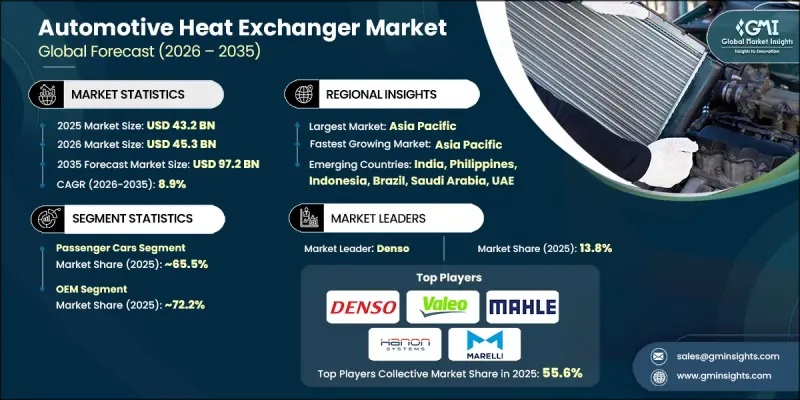

The Global Automotive Heat Exchanger Market was valued at USD 43.2 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 97.2 billion by 2035.

The market is undergoing significant transformation due to the rapid electrification of vehicles, stricter emission standards, and the growing need for improved energy efficiency. Heat exchangers, once primarily used for engine cooling and basic HVAC in internal combustion engine vehicles, are now crucial for managing complex thermal loads in modern vehicles. In electric and hybrid vehicles, they regulate battery temperature, cool power electronics, and maintain cabin comfort, directly impacting vehicle safety, performance, and driving range. Rising consumer demand for comfort and premium in-vehicle experiences is driving the adoption of advanced thermal systems. Compact, efficient heat exchangers are being integrated into automatic climate control, multi-zone HVAC, and heated or cooled seating systems. Manufacturers are increasingly using lightweight, high-performance materials like aluminum and composites to enhance heat transfer while reducing vehicle weight. The expansion of electric vehicles and tightening fuel efficiency regulations is pushing OEMs to adopt integrated thermal architectures that combine multiple heat exchange functions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $43.2 Billion |

| Forecast Value | $97.2 Billion |

| CAGR | 8.9% |

The passenger cars segment held a 65.5% share in 2025 and is projected to grow at a CAGR of 8.7% through 2035. Passenger vehicles dominate due to rising global personal mobility, widespread adoption of hybrid and electric vehicles, and consumer demand for comfort, safety, and energy efficiency. These vehicles require efficient thermal management for engine cooling, battery performance, and HVAC systems to ensure optimal driving range and cabin comfort. Innovations in microchannel heat exchangers, integrated thermal management systems, and lightweight designs further drive growth in this segment.

The OEM segment accounted for 72.2% share in 2025 and is expected to grow at a CAGR of 8.3% from 2026 to 2035. OEMs lead the market as heat exchangers are integrated during vehicle design and assembly, ensuring optimal engine cooling, battery management, and HVAC performance. OEMs focus on high-quality, durable heat exchangers to meet emission and efficiency standards. Early integration reduces aftermarket dependency, ensures regulatory compliance, and enhances overall vehicle performance, making OEMs the primary revenue contributors in the automotive heat exchanger market.

China Automotive Heat Exchanger Market held a 64.2% share, generating USD 11 billion in 2025. The country's robust growth stems from its global vehicle production leadership and rapid electrification in both passenger and commercial segments. Government incentives, emission regulations, and EV mandates are boosting demand for advanced thermal solutions. China's extensive manufacturing ecosystem, domestic OEM presence, and leadership in battery and electric vehicle supply chains are driving the need for specialized thermal management solutions such as battery cooling systems and heat pump-based HVAC technologies.

Key players operating in the Global Automotive Heat Exchanger Market include Denso, BorgWarner, Valeo, Sanden, Mahle, Dana, T.RAD, Marelli, Hanon Systems, and Spectra Premium. Companies in the Automotive Heat Exchanger Market are strengthening their position by investing in research and development to improve efficiency, reduce weight, and enhance durability. They are expanding product portfolios to include integrated thermal management solutions for ICE, hybrid, and electric vehicles. Strategic collaborations with OEMs ensure early integration and regulatory compliance. Firms focus on lightweight and high-performance materials, microchannel designs, and advanced manufacturing processes to optimize heat transfer. Additionally, companies are expanding into emerging markets, offering cost-efficient and high-performance solutions to meet the growing global demand for EVs, battery cooling systems, and compact HVAC applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Design

- 2.2.5 Vehicle

- 2.2.6 Propulsion

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of electric and hybrid vehicles

- 3.2.1.2 Stringent emissions and fuel efficiency regulations

- 3.2.1.3 Advancements in heat exchanger material

- 3.2.1.4 Increasing vehicle production and demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High material and manufacturing costs

- 3.2.2.2 Complexity of thermal management systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric vehicle thermal management systems

- 3.2.3.2 Adoption of advanced heat pump-based HVAC systems

- 3.2.3.3 Integration of smart and connected thermal systems

- 3.2.3.4 Growth in emerging markets and vehicle production

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory guideline

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA Vehicle Emission & Fuel Efficiency Standards

- 3.4.1.2 Canada: Transport Canada Safety & Thermal Performance Standards

- 3.4.2 Europe

- 3.4.2.1 Germany: End-of-Life Vehicle (ELV) Directive

- 3.4.2.2 UK: Zero Emission Vehicle (ZEV) Mandate

- 3.4.2.3 France: Energy Transition Law

- 3.4.2.4 Italy: National Energy & Climate Plan (PNIEC) Alignment

- 3.4.3 Asia Pacific

- 3.4.3.1 China: NEV Mandate & Dual Credit Policy

- 3.4.3.2 India: FAME II & PLI Scheme for Auto Components

- 3.4.3.3 Japan: Green Growth Strategy & JEVS Standards

- 3.4.3.4 Australia: National Electric Vehicle Strategy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: Rota 2030 Program

- 3.4.4.2 Mexico: USMCA Localization Requirements

- 3.4.4.3 Argentina: National Sustainable Mobility Policies

- 3.4.5 MEA

- 3.4.5.1 UAE: Net Zero 2050 Strategy & EV Infrastructure Expansion

- 3.4.5.2 Saudi Arabia: Vision 2030 & EV Localization Strategy

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (driven by primary research)

- 3.9 Pricing Analysis (driven by primary research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Capacity & production landscape (driven by primary research)

- 3.11.1 Installed capacity by region & key producer

- 3.11.2 Capacity utilization rates & expansion pipelines

- 3.12 Cost breakdown analysis

- 3.13 Sustainability and environmental impact analysis

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Future outlook & opportunities

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-Driven Disruption of Existing Business Models

- 3.15.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.15.2.1 Predictive Thermal Modeling & Temperature Profile Optimization

- 3.15.2.2 AI-Enabled Fast Charging Thermal Management

- 3.15.2.3 Real-Time Adaptive Cooling Strategies for Battery Longevity

- 3.15.2.4 Autonomous Vehicle Thermal Load Prediction

- 3.15.3 Risks, Limitations & Regulatory Considerations

- 3.16 Forecast assumptions & scenario analysis (driven by primary research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light-duty

- 5.3.2 Medium-duty

- 5.3.3 Heavy-duty

- 5.4 Off highway vehicle

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Radiators

- 8.3 Intercoolers

- 8.4 Oil coolers

- 8.5 Exhaust gas recirculation (EGR)

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Aluminum

- 9.3 Copper

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Design, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Plate Bar

- 10.3 Tube Fin

- 10.4 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Belgium

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Borgwarner

- 12.1.2 Dana

- 12.1.3 Denso

- 12.1.4 Hanon systems

- 12.1.5 Hitachi Astemo

- 12.1.6 Mahle

- 12.1.7 Marelli

- 12.1.8 Sanden

- 12.1.9 Valeo

- 12.1.10 Webasto

- 12.2 Regional Players

- 12.2.1 Eberspacher

- 12.2.2 Koyorad

- 12.2.3 Modine manufacturing company

- 12.2.4 Nissens

- 12.2.5 Pwr

- 12.2.6 Samvardhana motherson (SMRC)

- 12.2.7 Sogefi

- 12.2.8 T.rad co

- 12.3 Emerging Players

- 12.3.1 Dana tm4

- 12.3.2 Gentherm

- 12.3.3 Sanhua automotive components

- 12.3.4 Yinlun machinery