PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027534

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027534

Cell Culture Media Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

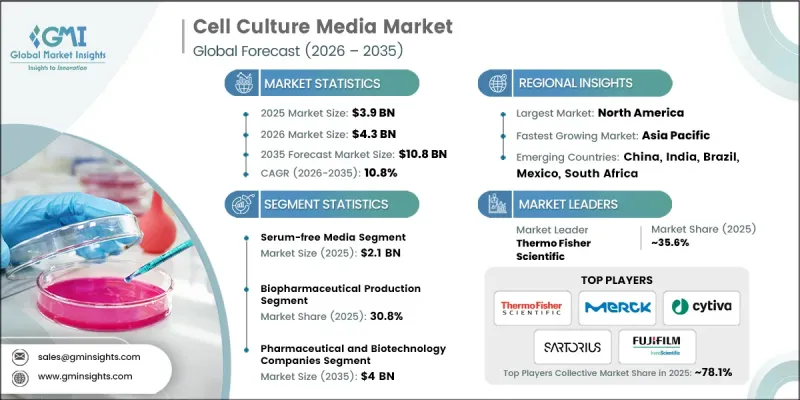

The Global Cell Culture Media Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 10.8 billion by 2035.

Market expansion is driven by the rising prevalence of chronic diseases, including cancer, diabetes, and autoimmune disorders, which increase the demand for cell-based research and therapeutic applications. Technological advancements in cell culture, such as the development of serum-free and chemically defined media, have enhanced scalability, reproducibility, and efficiency in laboratories. Cell culture media, designed to provide essential nutrients for cellular growth, maintenance, and differentiation, are increasingly replacing serum-based formulations due to regulatory compliance requirements and reduced contamination risks. Biopharmaceutical manufacturers are adopting defined media to ensure consistent batch quality, particularly in biologics and vaccine production, while the shift toward cell-based therapies and monoclonal antibodies is further fueling demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 10.8% |

The serum-free media segment generated USD 2.1 billion in 2025. This segment includes CHO media, HEK 293 media, BHK media, VERO cell media, insect cell media, immune cell media, and other serum-free formulations. Its dominance is attributed to enhanced safety, regulatory compliance, and reproducibility compared to traditional serum-based media. Serum-free media eliminate variability from animal-derived components, ensuring consistent cell growth and improved product quality, which is crucial for biologics, vaccines, and advanced therapies. The increasing adoption of cell-based therapies and monoclonal antibodies has also contributed to the widespread use of serum-free formulations.

The biopharmaceutical production segment accounted for a 30.8% share in 2025. Growth in this segment is fueled by the expansion of the biopharmaceutical industry and the increasing adoption of biologics, including vaccines, recombinant proteins, gene therapies, and cell therapies. Rising chronic disease incidence and demand for targeted treatments have driven the development and commercialization of these therapies, supporting the global cell culture media market.

North America Cell Culture Media Market held a 39% share in 2025. The region's biotechnology and pharmaceutical sectors benefit from advanced research infrastructure, substantial life sciences investments, and strong government support. Funding from institutions such as the National Institutes of Health (NIH) and growing demand for personalized therapies have further accelerated the adoption of specialized cell culture media. The U.S. continues to drive regional growth through investments in innovative biopharmaceutical research and development, which underpins the rising need for high-quality, reproducible cell culture solutions.

Key players operating in the Cell Culture Media Market include Merck, FUJIFILM Irvine Scientific, Thermo Fisher Scientific, Lonza, Sartorius, Cytiva, ACROBiosystems, Miltenyi Biotec, PromoCell, Biowest, JSBio, Shanghai Mediumbank Biotechnology, ProBio, Quacell Biotechnology, Elabscience, Cellplus Bio, Shanghai BioEngine, Eminence Scientific, Corning, Shanghai Basal Media, Sino Biological, and OPM Biosciences. Key strategies employed by companies in the Cell Culture Media Market include expanding their portfolio of serum-free and chemically defined media to meet regulatory standards and minimize contamination risks. Manufacturers are focusing on R&D to develop specialized media for biopharmaceutical and cell therapy applications. Strategic partnerships with research institutions and biopharmaceutical companies enhance distribution channels and market reach. Companies are investing in scalable production facilities to meet growing global demand, while also leveraging technology to improve product quality and consistency. Targeted marketing campaigns, regulatory compliance certifications, and collaborations with healthcare and life sciences organizations further strengthen market presence and reinforce brand credibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases

- 3.2.1.2 Advancements in cell culture and media technology

- 3.2.1.3 Increasing demand for serum and animal component-free media

- 3.2.1.4 Growing demand for regenerative medicine

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of cell biology products

- 3.2.2.2 Stringent regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for advanced therapy medicinal products (ATMPs)

- 3.2.3.2 Rising contract manufacturing and CDMO partnerships

- 3.2.3.3 Technological advancements in custom media formulation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Cell culture media production analysis, 2025

- 3.6.1 Production capacity

- 3.6.2 Capacity utilization rate

- 3.6.3 Final/actual manufactured volume

- 3.6.4 Production trends

- 3.7 Pricing analysis, 2025 (Driven by Primary Research)

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Gap analysis

- 3.10 Future market trends

- 3.11 Impact of AI and Gen AI on the market

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Cell culture media industry chain analysis

- 3.14.1 Upstream process analysis

- 3.14.1.1 Raw material sourcing

- 3.14.1.2 Formulation development

- 3.14.1.3 Manufacturing and quality control

- 3.14.1.4 Supply chain and logistics

- 3.14.2 Downstream segments

- 3.14.2.1 End user

- 3.14.2.2 Application

- 3.14.2.3 Distribution channels

- 3.14.1 Upstream process analysis

- 3.15 Supply chain analysis

- 3.16 Customer profile analysis for major companies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Serum-free media

- 5.2.1 CHO media

- 5.2.2 HEK 293 media

- 5.2.3 BHK media

- 5.2.4 VERO cell media

- 5.2.5 Insect cell media

- 5.2.6 Immune cell media

- 5.2.7 Other serum-free media

- 5.3 Specialty media

- 5.4 Chemically defined media

- 5.5 Stem cell culture media

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Biopharmaceutical production

- 6.2.1 Monoclonal antibodies

- 6.2.2 Vaccine production

- 6.2.3 Other biopharmaceutical productions

- 6.3 Diagnostics

- 6.4 Drug screening and development

- 6.5 Tissue engineering and regenerative medicine

- 6.6 Research purpose

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical and biotechnology companies

- 7.3 Hospital and diagnostic laboratories

- 7.4 Research and academic institutes

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ACROBiosystems

- 9.2 Biowest

- 9.3 Cellplus Bio

- 9.4 Corning

- 9.5 Cytiva

- 9.6 Elabscience

- 9.7 Eminence Scientific

- 9.8 FUJIFILM Irvine Scientific

- 9.9 JSBio

- 9.10 Lonza

- 9.11 Shanghai Mediumbank Biotechnology

- 9.12 Merck

- 9.13 Miltenyi Biotec

- 9.14 OPM Biosciences

- 9.15 ProBio

- 9.16 PromoCell

- 9.17 Quacell Biotechnology

- 9.18 Sartorius

- 9.19 Shanghai BioEngine

- 9.20 Shanghai Basal Media

- 9.21 Sino Biological

- 9.22 Suzhou Womei

- 9.23 Thermo Fisher Scientific