PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027540

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027540

Pet Allergy Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

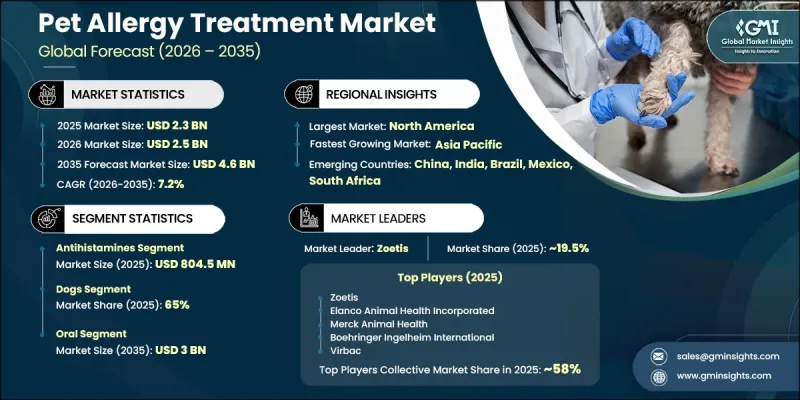

The Global Pet Allergy Treatment Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 4.6 billion by 2035.

Market expansion is supported by increasing awareness among pet owners regarding early detection and timely treatment, along with improved access to veterinary care. Advancements in veterinary science, particularly in treatment innovation and diagnostic accuracy, continue to enhance therapeutic outcomes and drive adoption. Pet allergy treatments are designed to manage and control a broad range of allergic conditions affecting animals. These solutions include various pharmaceutical and therapeutic approaches aimed at improving pet health and quality of life. Growing understanding among pet owners about the long-term health implications of untreated allergies has significantly increased demand for effective treatment options. The market is also witnessing a shift toward long-term care solutions, with innovative therapies gaining traction. Preventive healthcare awareness continues to rise, further strengthening product acceptance and supporting sustained market growth. Increasing investments in veterinary healthcare infrastructure and product development are also contributing to the overall expansion of the pet allergy treatment market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 7.2% |

The antihistamines segment captured USD 804.5 million in 2025. This dominance is driven by their widespread adoption as a primary treatment option for allergic conditions in animals. These medications are frequently recommended due to their effectiveness in providing quick symptom relief and their favorable safety profile. Their versatility in administration and accessibility across various formats further supports strong market demand. The ability of these treatments to address mild to moderate allergic responses contributes significantly to their continued usage and commercial success.

The dogs segment held a 65% share in 2025. Growth in this segment is fueled by the increasing preference for dogs as companion animals and rising spending on their healthcare. Higher pet ownership rates, combined with greater awareness of animal health, are key contributors to this trend. The growing incidence of allergic conditions among dogs further accelerates demand for specialized treatments. Additionally, improving economic conditions and the availability of advanced, targeted products continue to support segment expansion over the forecast period.

North America Pet Allergy Treatment Market represents 41.8% share in 2025 and is expected to grow at a CAGR of 6.8% through 2035. The region maintains a strong position due to high levels of pet ownership and increasing emphasis on pet well-being. Significant expenditure on veterinary healthcare and the presence of leading industry participants contribute to market dominance. Early adoption of advanced treatment solutions and strong awareness regarding pet health conditions further drive regional growth. A well-developed veterinary ecosystem, along with widespread acceptance of pet healthcare services, continues to reinforce North America's leadership in the market.

Key companies operating in the Pet Allergy Treatment Market include Antech Diagnostics, Boehringer Ingelheim International, Ceva Sante Animale, Dechra, Elanco, IDEXX Laboratories, Merck Animal Health, Neogen Corporation, Nextmune, PetIQ, Provetica, Vetoquinol, Virbac, and Zoetis. Companies in the Pet Allergy Treatment Market are actively enhancing their market position through continuous innovation and strategic expansion initiatives. They focus on developing advanced therapeutic solutions that improve treatment effectiveness and long-term outcomes. Investment in research and development remains a priority to introduce novel products and improve diagnostic capabilities. Strategic collaborations and partnerships enable companies to broaden their geographic presence and strengthen distribution networks. Businesses are also emphasizing digital integration and data-driven veterinary solutions to enhance service delivery. Expansion of production capabilities and localized manufacturing helps improve supply efficiency. Additionally, companies are focusing on customer engagement, education, and preventive care awareness to build brand loyalty and sustain long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Pet type trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of pet allergies

- 3.2.1.2 Availability of over-the-counter (OTC) medications

- 3.2.1.3 Increasing pet ownership and rising veterinary expenditures

- 3.2.1.4 Advancements in veterinary dermatology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects of medications

- 3.2.2.2 Increasing adoption of natural or home-based remedies

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Development of personalized treatments

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.1.1 U.S.

- 3.3.1.2 Canada

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.1 North America

- 3.4 Technology/innovation landscape

- 3.4.1 Current technologies

- 3.4.2 Emerging technologies

- 3.5 Pipeline analysis (Driven by Primary Research)

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Future market trends

- 3.8 Impact of AI & generative AI on the market

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Antihistamines

- 5.3 Corticosteroids

- 5.4 Immunotherapy

- 5.5 Other drug classes

Chapter 6 Market Estimates and Forecast, By Pet Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Rabbits

- 6.5 Other pet types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Antech Diagnostics

- 10.2 Boehringer Ingelheim International

- 10.3 Ceva Sante Animale

- 10.4 Dechra

- 10.5 Elanco

- 10.6 IDEXX Laboratories

- 10.7 Merck Animal Health

- 10.8 Neogen Corporation

- 10.9 Nextmune

- 10.10 PetIQ

- 10.11 Provetica

- 10.12 Vetoquinol

- 10.13 Virbac

- 10.14 Zoetis