PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027548

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027548

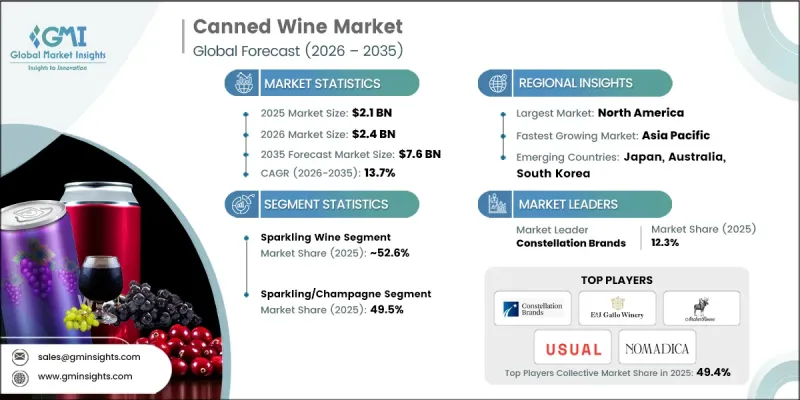

Canned Wine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Canned Wine Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 13.7% to reach USD 7.6 billion by 2035.

Canned wine has gained traction as a convenient and portable packaging solution, especially for outdoor and social events. Consumers attending picnics, festivals, camping trips, and sports events increasingly prefer cans for their lightweight design, ease of transport, and simple disposal. Unlike fragile glass bottles, cans provide durability without sacrificing convenience, while single-serving portions allow consumers to sample wines without committing to a full bottle. Sustainability also plays a role, as aluminum cans achieve approximately a 50% recycling rate according to the U.S. Environmental Protection Agency, making them a more environmentally friendly option. The market has expanded rapidly with consumer acceptance, offering products that include sparkling wines, rose, red, white wines, and wine cocktails, enabling companies to cater to diverse tastes and event requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 13.7% |

The sparkling wine segment held 52.6% share in 2025 and is expected to grow at a CAGR of 14.1% through 2035. While red and white still wines are growing in popularity due to portability, sparkling varieties such as prosecco and champagne dominate celebrations. These products are increasingly favored because innovative packaging allows them to be more accessible for both formal and casual occasions.

In 2025, the sparkling/champagne segment accounted for 49.5% share. Red and white wines continue to be major contributors to canned wine sales, while rose is gaining traction among younger consumers who see it as a stylish and refreshing option. The versatility of sparkling wines for celebratory and informal settings strengthens their dominance in the market.

North America Canned Wine Market was valued at USD 1.1 billion in 2025 and is expected to grow at a CAGR of 12.2% from 2026 to 2035. Urban consumers increasingly prefer canned wine for outdoor activities, while eco-conscious buyers seek sustainable and convenient options. Demand for premium flavors and innovative taste experiences supports market expansion, with existing brands consolidating their positions. Both the U.S. and Canada are experiencing growth driven by the preference for portable, environmentally responsible packaging solutions.

Key players in the Global Canned Wine Market include Usual Wines, SANS Wine Co, House Wine, Nomadica, Villa Maria, Concha y Toro, Giesen, Maker Wine, Off Track Wines, Bodega Santa Julia, Rosadito, Archer Roose, Marisco, E. & J. Gallo, and Constellation Brands. Global Canned Wine Market are focusing on strategies such as expanding product portfolios to include sparkling, rose, and wine cocktail options to appeal to a broader consumer base. Firms are investing in innovative packaging designs that improve portability, sustainability, and consumer convenience. Strategic partnerships with distributors, retailers, and event organizers enable wider market reach. Marketing efforts emphasize eco-friendly credentials and premium flavor experiences, creating brand differentiation. Companies are also adopting direct-to-consumer models, digital promotion, and limited-edition releases to enhance engagement, boost sales, and strengthen market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Wine color

- 2.2.4 Alcohol content

- 2.2.5 Packaging

- 2.2.6 Production type

- 2.2.7 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenient & portable wine packaging

- 3.2.1.2 Growing outdoor recreation & event culture

- 3.2.1.3 Sustainability preferences favoring aluminum over glass

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Premium wine perception barriers for canned format

- 3.2.2.2 Limited shelf life compared to bottled wine

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with growing wine culture

- 3.2.3.2 Premiumization of canned wine portfolio

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Million Litres)

- 5.1 Key trends

- 5.2 Still wine

- 5.2.1 Red wine

- 5.2.2 White wine

- 5.2.3 Rose wine

- 5.3 Sparkling wine

- 5.3.1 Champagne

- 5.3.2 Prosecco

- 5.3.3 Others

- 5.4 Fortified wine

- 5.4.1 Sherry

- 5.4.2 Port

- 5.4.3 Vermouth

- 5.4.4 Others

Chapter 6 Market Estimates and Forecast, By Wine Color, 2022-2035 (USD Billion) (Million Litres)

- 6.1 Key trends

- 6.2 Red wine

- 6.3 White wine

- 6.4 Rose wine

- 6.5 Sparkling/champagne

Chapter 7 Market Estimates and Forecast, By Alcohol Content, 2022-2035 (USD Billion) (Million Litres)

- 7.1 Key trends

- 7.2 Low alcohol (< 10% ABV)

- 7.3 Medium alcohol (10-14% ABV)

- 7.4 High alcohol (>14% ABV)

Chapter 8 Market Estimates and Forecast, By Packaging, 2022-2035 (USD Billion) (Million Litres)

- 8.1 Key trends

- 8.2 Single-serve cans

- 8.3 Multi-serve cans

Chapter 9 Market Estimates and Forecast, By Production Type 2022-2035 (USD Billion) (Million Litres)

- 9.1 Key trends

- 9.2 Conventional

- 9.3 Organic

Chapter 10 Market Estimates and Forecast, By Distribution Channel 2022-2035 (USD Billion) (Million Litres)

- 10.1 Key trends

- 10.2 On-Trade

- 10.3 Off-Trade

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Million Litres)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Concha y Toro

- 12.2 Bodega Santa Julia

- 12.3 Usual Wines

- 12.4 House Wine

- 12.5 Nomadica

- 12.6 Maker Wine

- 12.7 SANS Wine Co

- 12.8 Off Track Wines

- 12.9 Marisco

- 12.10 Villa Maria

- 12.11 Giesen

- 12.12 Rosadito

- 12.13 Archer Roose

- 12.14 Constellation Brands

- 12.15 E. & J. Gallo