PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027570

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027570

Artisanal Ice Cream Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

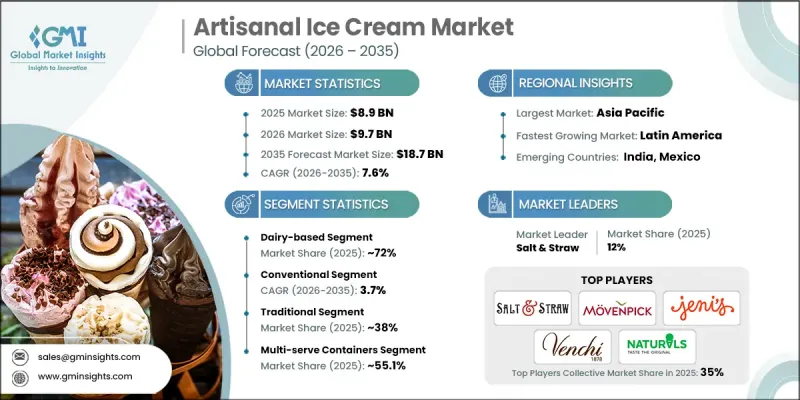

The Global Artisanal Ice Cream Market was valued at USD 8.9 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 18.7 billion by 2035.

The artisanal ice cream industry is gaining strong momentum as consumers increasingly seek premium, handcrafted products made with natural ingredients. Demand is being driven by a growing preference for authentic food experiences that emphasize freshness, quality, and transparency. Producers focus on carefully sourced ingredients while avoiding artificial additives, aligning with the expectations of health-conscious consumers who favor minimally processed options. Personalization is another key factor shaping market growth, as consumers look for tailored flavor combinations and alternative formulations that suit diverse dietary needs. This flexibility allows brands to cater to evolving consumption patterns and lifestyle preferences. However, the market faces challenges related to higher production costs, as premium ingredient sourcing and small-batch manufacturing processes increase overall expenses. Despite this, the emphasis on quality and uniqueness continues to attract a loyal customer base. As consumer interest in premium desserts and customized offerings rises, the global artisanal ice cream market is expected to maintain steady growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.9 Billion |

| Forecast Value | $18.7 Billion |

| CAGR | 7.6% |

In 2025, the dairy-based products segment accounted for 72% share and is projected to grow at a CAGR of 6.1% through 2035. This segment continues to lead due to its rich taste, smooth texture, and strong consumer familiarity. While plant-based alternatives are gaining attention, dairy-based offerings remain dominant, particularly among consumers who prefer traditional formulations and premium flavor profiles associated with classic artisanal products.

The conventional segment held a 65% share in 2025 and is expected to grow at a CAGR of 3.7% during 2026-2035. Conventional artisanal ice cream continues to generate the majority of revenue due to its established appeal and consistent demand for traditional flavors. At the same time, product diversification is expanding, with brands introducing alternative options that cater to evolving dietary preferences. This balanced approach enables companies to preserve their core identity while tapping into new consumer segments and emerging trends.

North America Artisanal Ice Cream Market accounted for 30.3% share in 2025, representing a mature and innovation-driven region. Growth is supported by strong consumer demand for premium, clean-label, and locally crafted products. The region benefits from well-developed infrastructure and a consumer base that actively explores new and unique food experiences. These factors create a favorable environment for artisanal brands to expand and strengthen their market presence.

Key companies operating in the Global Artisanal Ice Cream Market include Jeni's Splendid Ice Creams, Salt & Straw, Van Leeuwen Ice Cream, Amorino, Movenpick, Nestle, Unilever, Graeter's Ice Cream, McConnell's Fine Ice Creams, Humphry Slocombe, Coolhaus, Bi-Rite Creamery, Afters Ice Cream, Nick's Ice Cream, Morgenstern's Finest Ice Cream, Wanderlust Creamery, Blue Bell Creameries, and Natural Ice Cream. Companies in the Artisanal Ice Cream Market are strengthening their position through product innovation, premium branding, and strategic expansion. They are focusing on introducing unique flavors and high-quality ingredients to differentiate their offerings and attract a broader consumer base. Investments in sustainable sourcing and clean-label formulations are helping align products with evolving consumer preferences. Brands are also expanding their retail presence and enhancing direct-to-consumer channels to improve accessibility. Additionally, companies are leveraging collaborations and limited-edition launches to create exclusivity and drive engagement, while maintaining a strong emphasis on quality and authenticity to build long-term brand loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Formulation

- 2.2.3 Dietary Attribute

- 2.2.4 Flavor

- 2.2.5 Packaging Format

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for premium & authentic experiences

- 3.2.1.2 Growing health consciousness & clean label preferences

- 3.2.1.3 Expanding plant-based & dietary alternative adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & ingredient price volatility

- 3.2.2.2 Limited distribution infrastructure & cold chain complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with growing middle class

- 3.2.3.2 Innovation in functional & fortified ice cream

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product Formulation

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Formulation, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy-based

- 5.2.1 Traditional cream-based

- 5.2.2 Premium milk-based

- 5.2.3 Others

- 5.3 Plant-based

- 5.3.1 Coconut-based

- 5.3.2 Almond-based

- 5.3.3 Oat-based

- 5.3.4 Soy-based

- 5.3.5 Cashew-based

- 5.3.6 Others

Chapter 6 Market Estimates and Forecast, By Dietary Attribute, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Lactose-free

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Flavor, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Traditional

- 7.2.1 Vanilla

- 7.2.2 Chocolate

- 7.2.3 Strawberry

- 7.3 Fruits & nuts

- 7.3.1 Berry blends

- 7.3.2 Stone fruit varieties

- 7.3.3 Tropical fruit

- 7.3.4 Nut-infused (pistachio, hazelnut, pecan)

- 7.4 Exotic & seasonal

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Packaging Format, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Single-serve

- 8.2.1 Cones (wafer, sugar, waffle)

- 8.2.2 Sticks & bars

- 8.2.3 Cups (<500 ml)

- 8.3 Multi-serve containers

- 8.3.1 Pints (500 ml-600 ml)

- 8.3.2 Tubs (1 L-2 L)

- 8.3.3 Family size (>2 L)

- 8.4 Bulk / foodservice

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & hypermarkets

- 9.3 Specialty stores

- 9.4 Online retail

- 9.5 Foodservice & hospitality

- 9.6 Convenience stores

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Afters Ice Cream

- 11.2 Amorino

- 11.3 Bi-Rite Creamery

- 11.4 Blue Bell Creameries

- 11.5 Coolhaus

- 11.6 Graeter's Ice Cream

- 11.7 Humphry Slocombe

- 11.8 Jeni's Splendid Ice Creams

- 11.9 McConnell's Fine Ice Creams

- 11.10 Morgenstern's Finest Ice Cream

- 11.11 Movenpick

- 11.12 Natural Ice Cream

- 11.13 Nestle

- 11.14 Nick's Ice Cream

- 11.15 Salt & Straw

- 11.16 Unilever

- 11.17 Van Leeuwen Ice Cream

- 11.18 Wanderlust Creamery