PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027606

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027606

Vegetable Shortening Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

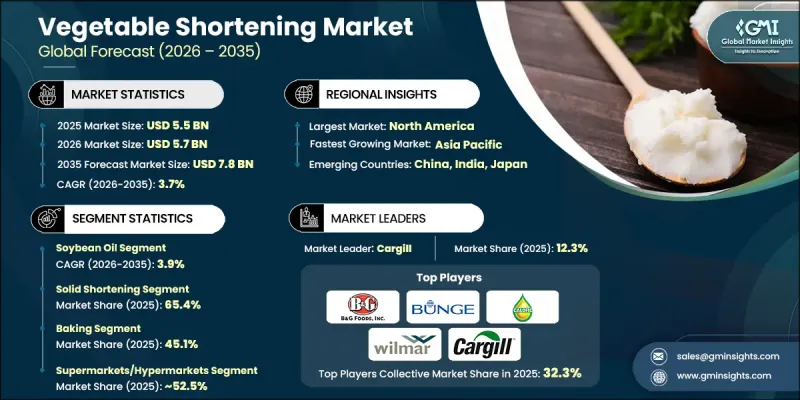

The Global Vegetable Shortening Market was valued at USD 5.5 billion in 2025 and is estimated to grow at a CAGR of 3.7% to reach USD 7.8 billion by 2035.

The market is driven by the baking and food service industries, where vegetable shortening is prized for producing soft, flaky textures in pastries, cookies, cakes, and deep-fried foods while extending shelf life. Rising consumer awareness of health and wellness is influencing market dynamics, with increasing preference for trans fat-free and non-hydrogenated formulations. The growing popularity of plant-based and vegan diets is accelerating demand for sustainable, clean-label, and non-GMO shortening products. Innovation in product formulations and expanding applications in food processing support sustained growth. Market expansion is fueled by two primary factors: the rising consumption of ready-to-eat baked goods and the surge in home baking activities, as consumers seek healthier, convenient, and plant-based alternatives that meet modern dietary and lifestyle trends.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.5 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 3.7% |

The soybean oil segment held a 40.5% share and is expected to grow at a CAGR of 3.9% through 2035. Vegetable shortening sources are highly diverse, including soybean oil, palm oil, cottonseed oil, and sunflower oil. Palm oil remains widely used due to its cost-effectiveness and excellent stability, while soybean oil retains its popularity for nutritional benefits and versatile applications across various food products.

The solid shortening segment accounted for 65.4% share in 2025 and is projected to grow at a CAGR of 3.8% between 2026 and 2035. Shifts in consumer preferences have emphasized convenience, versatility, and functional performance, with solid shortening maintaining a leading position in baking and frying applications. Its ability to deliver consistent textures, prolonged freshness, and ease of use reinforces its dominance among bakers and food processors.

North America Vegetable Shortening Market represented 34.7% share in 2025. The region benefits from high consumer awareness and demand for ready-to-eat baked goods and snacks. The United States accounts for the largest share within the region, driven by widespread use of vegetable shortening in baking, frying, and snack production. Companies are increasingly producing clean-label, plant-based, non-GMO products to align with health-conscious consumer preferences. Rising adoption of vegan and vegetarian diets further supports demand for plant-based shortening, making North America a key growth hub.

Major players in the Global Vegetable Shortening Market include Ventura Foods, NIRMALA AVIJAYA GROUP, Bunge, Wilmar International Ltd, Spectrum Naturals, CALOFIC, Cargill, B&G Foods, Stratas Foods, GOLDEN HOPE - NHA BE EDIBLE OILS CO., LTD, and Manildra Group. Companies in the A are strengthening their position through several strategies, including product innovation, expanding plant-based and non-GMO portfolios, and focusing on clean-label formulations. Manufacturers invest in research and development to create healthier, trans fat-free options while maintaining functional performance. Expanding distribution networks across retail and food service channels enhances market penetration. Strategic partnerships with bakeries, restaurants, and food processors improve visibility and adoption. Companies also leverage marketing campaigns emphasizing sustainability, nutritional benefits, and versatile applications. Investments in advanced production technologies reduce costs and improve product consistency. Continuous consumer engagement, education, and adaptation to dietary trends ensure brand loyalty and long-term competitive advantage in the evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soybean oil

- 5.3 Palm oil

- 5.4 Cottonseed oil

- 5.5 Sunflower oil

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid shortening

- 6.3 Liquid shortening

- 6.4 Powdered shortening

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Baking

- 7.3 Frying

- 7.4 Confectionery

- 7.5 Snacks & savory

- 7.6 Food processing

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets/hypermarkets

- 8.3 Convenience stores

- 8.4 Online retail

- 8.5 Specialty stores

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 B&G Foods, Inc.

- 10.2 Bunge

- 10.3 CALOFIC

- 10.4 Cargill

- 10.5 GOLDEN HOPE - NHA BE EDIBLE OILS CO., LTD

- 10.6 Manildra Group

- 10.7 NIRMALA AVIJAYA GROUP

- 10.8 Spectrum Naturals

- 10.9 Stratas Foods

- 10.10 Ventura Foods

- 10.11 Wilmar International