PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027660

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027660

North America Plastic Waste Pyrolysis Oil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

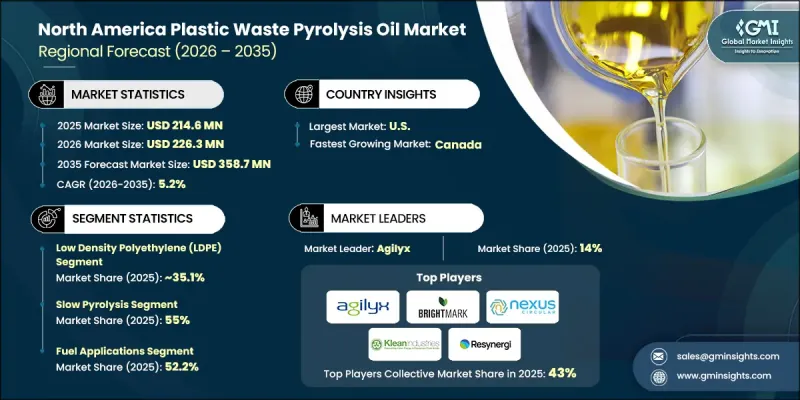

North America Plastic Waste Pyrolysis Oil Market was valued at USD 214.6 million in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 358.7 million in 2035.

Market growth is driven by the accelerating shift toward circular economy models and the increasing need to reduce dependence on conventional fossil fuel feedstocks. Pyrolysis oil is gaining strategic importance across the region as it serves as a valuable input for chemical production, refining processes, and low-carbon fuel applications. Companies are increasingly integrating pyrolysis-based solutions into closed-loop plastic waste management systems to support sustainability targets and decarbonization goals. Regulatory frameworks across North America are also encouraging cleaner production practices, driving investments in technologies that convert end-of-life plastics into usable energy and chemical resources. The market is further supported by advancements in processing technologies, feedstock optimization methods, and upgrading systems that improve product consistency and operational efficiency. Continuous industrial focus on waste reduction and emission control is reinforcing the role of pyrolysis oil in modern manufacturing and energy systems. Growing participation from waste-to-value operators and technology developers is also strengthening the regional ecosystem for advanced plastic recovery solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $214.6 Million |

| Forecast Value | $358.7 Million |

| CAGR | 5.2% |

The low-density polyethylene (LDPE) segment held a share of 35.1% in 2025 and is projected to grow at a CAGR of 5.4% through 2035. LDPE remains the preferred feedstock due to its wide availability, consistent composition, and high conversion efficiency during pyrolysis processing. Its stable processing characteristics allow manufacturers to achieve reliable output quality and improved reactor performance. The dominance of LDPE is further supported by its significant presence in post-consumer waste streams, which ensures a steady raw material supply for pyrolysis oil production across the region.

The slow pyrolysis segment accounted for 55% share in 2025 and is expected to grow at a CAGR of 5.2% during 2026 to 2035. This method maintains a leading position due to its ability to deliver stable and consistent oil yields while processing a wide range of plastic waste types, including contaminated feedstock. Its longer residence time and controlled thermal decomposition process make it suitable for handling heterogeneous waste streams. In contrast, fast and flash pyrolysis technologies are used in specific applications where quicker processing cycles and tailored output characteristics are required.

North America Plastic Waste Pyrolysis Oil Market will grow at a decent CAGR through 2035, supported by the region's strong transition toward circular economy frameworks and low-carbon resource utilization. The region is emerging as a key production hub due to its advanced industrial infrastructure, strong technological capabilities, and well-established waste management networks. Increasing collaboration between technology developers and waste processing companies is further enhancing production efficiency and supporting the commercialization of high-quality pyrolysis oil across various end-use sectors.

Key companies operating in the North America Plastic Waste Pyrolysis Oil Market include Agilyx, Brightmark LLC, Nexus Circular, Klean Industries, Resynergi, Alterra Energy, Encina Development Group, and OMV Aktiengesellschaft. Companies in the North America Plastic Waste Pyrolysis Oil Market are focusing on strengthening their market position through expansion of production facilities, advancement of thermal conversion technologies, and integration of end-to-end recycling solutions. They are investing heavily in research and development to improve process efficiency, feedstock flexibility, and output quality. Strategic partnerships with waste management firms and industrial end users are enabling stronger supply chain integration and scaling of operations. Many players are also developing proprietary reactor designs and upgrading systems to enhance yield and reduce operational costs. Expansion into large-scale commercial projects and pilot demonstrations is helping accelerate technology adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Feedstock Type

- 2.2.3 Pyrolysis Process

- 2.2.4 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing plastic waste crisis & landfill diversion mandates

- 3.2.1.2 Circular economy initiatives & extended producer responsibility (epr) programs

- 3.2.1.3 Rising crude oil prices & demand for alternative feedstocks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements for pyrolysis facilities

- 3.2.2.2 Feedstock collection & contamination challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with refinery & petrochemical infrastructure

- 3.2.3.2 Marine plastic waste valorization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By feedstock type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Feedstock Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Low Density Polyethylene (LDPE)

- 5.3 High Density Polyethylene (HDPE)

- 5.4 Polypropylene (PP)

- 5.5 Polystyrene (PS)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Pyrolysis Process, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Fast Pyrolysis

- 6.3 Flash Pyrolysis

- 6.4 Slow Pyrolysis

Chapter 7 Market Estimates and Forecast, By End-User, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Fuel Applications

- 7.2.1 Marine Fuel

- 7.2.2 Industrial Boiler Fuel

- 7.2.3 Other

- 7.3 Chemical Feedstock

- 7.3.1 Aromatics (BTX - Benzene, Toluene, Xylene)

- 7.3.2 Olefins (Ethylene, Propylene)

- 7.3.3 Others

- 7.4 Heat & Power Generation

- 7.5 Refinery Blending

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

Chapter 9 Company Profiles

- 9.1 Agilyx

- 9.2 Brightmark LLC

- 9.3 Nexus Circular

- 9.4 Klean Industries

- 9.5 Resynergi

- 9.6 Alterra Energy

- 9.7 Encina Development Group

- 9.8 OMV Aktiengesellschaft