PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038272

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038272

Flexible Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

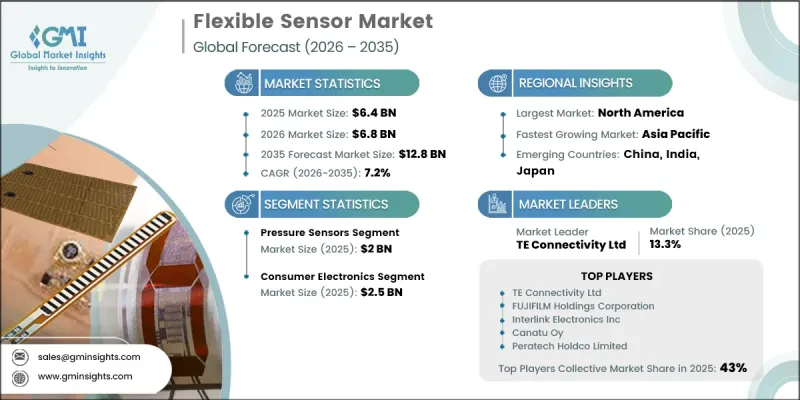

The Global Flexible Sensor Market was valued at USD 6.4 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 12.8 billion by 2035.

The industry is gaining traction as demand for wearable electronics and continuous health monitoring solutions accelerates worldwide. Increasing awareness around preventive healthcare and the rising prevalence of lifestyle-related conditions are encouraging consumers to adopt devices that enable real-time tracking of vital parameters. Flexible sensors are enabling the development of lightweight, skin-friendly, and non-invasive devices that deliver accurate readings without discomfort over extended periods. The shift toward remote patient monitoring across healthcare systems is supporting adoption, while ongoing advancements in material science and sensor design are enhancing performance capabilities. In parallel, growing integration in consumer electronics and next-generation display technologies is reinforcing market expansion, as manufacturers focus on innovation to meet evolving user expectations and functionality requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.4 Billion |

| Forecast Value | $12.8 Billion |

| CAGR | 7.2% |

The pressure sensors segment generated USD 2 billion in 2025, supported by increasing utilization across wearable devices, automotive applications, and advanced consumer electronics. These sensors enable precise measurement of force, motion, and touch, improving device responsiveness and user interaction. Rising demand for compact, lightweight, and high-performance components is further strengthening the segment's growth trajectory, reinforcing its leading position in the global market.

The healthcare segment is anticipated to grow at a CAGR of 8.4% through 2035, driven by rapid advancements in wearable medical technologies and remote monitoring systems. Flexible sensors play a critical role in enabling continuous tracking of patient health metrics, contributing to improved clinical outcomes and enhanced efficiency in healthcare delivery. Their growing adoption across hospitals, home care environments, and diagnostic applications reflects the increasing need for real-time, data-driven healthcare solutions.

North America Flexible Sensor Market accounted for 37.9% share in 2025, supported by strong technological adoption and a well-established ecosystem of manufacturers and end users. The region's leadership is further reinforced by high penetration of wearable devices, increasing deployment of intelligent industrial systems, and strong demand for advanced health monitoring solutions. Economic growth and innovation-driven investments continue to support the widespread integration of flexible sensor technologies across multiple industries.

Key players operating in the Global Flexible Sensor Industry include Tekscan Inc, Interlink Electronics Inc, FlexEnable Limited, KWJ Engineering Inc, TE Connectivity Ltd, FUJIFILM Holdings Corporation, Canatu Oy, BeBop Sensors Inc, Isorg SA, Thin Film Electronics ASA, T+Ink Inc, SynTouch LLC, Plastic Logic Limited, Peratech Holdco Limited, ElastiSense, NextInput Inc, Flexpoint Sensor Systems Inc, and Sensitronics LLC. Companies in the flexible sensor market are focusing on continuous innovation, strategic collaborations, and advanced material development to strengthen their competitive position. They are investing heavily in research and development to enhance sensor accuracy, flexibility, and durability while reducing production costs. Partnerships with healthcare providers, consumer electronics manufacturers, and automotive firms are enabling broader application integration and faster commercialization. Many players are also expanding their product portfolios to cater to emerging use cases such as wearable healthcare and smart devices.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Sensor Type trends

- 2.2.2 Application trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for wearable electronics and health monitoring devices

- 3.2.1.2 Growing adoption in consumer electronics and foldable displays

- 3.2.1.3 Rising use in automotive electronics and smart interiors

- 3.2.1.4 Expansion of internet of things (IoT) ecosystems

- 3.2.1.5 Growing applications in healthcare and biomedical devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and material costs

- 3.2.2.2 Limited durability and reliability compared to rigid sensors

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption in smart textiles and e-textiles

- 3.2.3.2 Development of next-generation flexible and stretchable materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends (Based on paid Database)

- 3.8.1 Historical Price Analysis (2022-2025)

- 3.8.2 Price Trend Drivers

- 3.8.3 Regional Price Variations

- 3.8.4 Price Forecast (2026-2035)

- 3.9 Trade Data Analysis (Driven by Primary Research)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Sensor Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Pressure sensors

- 5.2.1 Piezoresistive pressure sensors

- 5.2.2 Capacitive pressure sensors

- 5.3 Biosensors

- 5.3.1 Electrochemical biosensors

- 5.3.2 Optical biosensors

- 5.3.3 Others

- 5.4 Temperature sensors

- 5.4.1 Resistive temperature sensors

- 5.4.2 Thermocouple-based sensors

- 5.4.3 Infrared temperature sensors

- 5.5 Chemical sensors

- 5.5.1 Gas sensors

- 5.5.2 Humidity sensors

- 5.6 Strain sensors

- 5.7 Optical sensors

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Monitoring & detection

- 6.3 Quality control & feedback

- 6.4 Measurement

- 6.5 Diagnostics

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.3 Healthcare

- 7.4 Automotive

- 7.5 Aerospace & defense

- 7.6 Energy & utilities

- 7.7 Food & beverage

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 TE Connectivity Ltd

- 9.1.2 FUJIFILM Holdings Corporation

- 9.1.3 FlexEnable Limited

- 9.1.4 Plastic Logic Limited

- 9.2 Regional players

- 9.2.1 Canatu Oy

- 9.2.2 Isorg SA

- 9.2.3 Thin Film Electronics ASA

- 9.2.4 ElastiSense

- 9.3 Niche players

- 9.3.1 Tekscan Inc

- 9.3.2 Interlink Electronics Inc

- 9.3.3 KWJ Engineering Inc

- 9.3.4 BeBop Sensors Inc

- 9.3.5 T+Ink Inc

- 9.3.6 SynTouch LLC

- 9.3.7 Peratech Holdco Limited

- 9.3.8 NextInput Inc

- 9.3.9 Flexpoint Sensor Systems Inc

- 9.3.10 Sensitronics LLC

- 9.3.11 GSI Technologies Inc.