PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038306

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038306

Automotive LiDAR Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

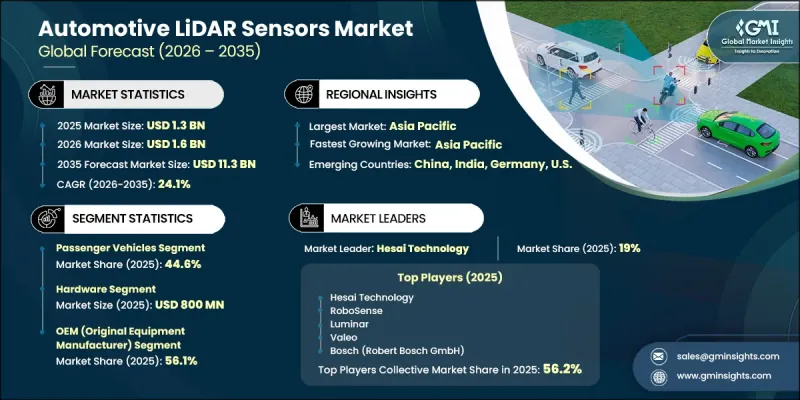

The Global Automotive Lidar Sensors Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 24.1% to reach USD 11.3 billion by 2035.

Increasing emphasis on vehicle safety, precision navigation, and real-time environmental awareness is encouraging automakers to incorporate high-performance perception systems. LiDAR technology is gaining strong traction due to its ability to deliver accurate spatial mapping and object detection, which are critical for next-generation driving capabilities. As mobility solutions evolve, the demand for reliable, high-resolution sensors continues to rise across both passenger and commercial vehicle categories. Continuous innovation in sensor design, improved cost efficiency, and advancements in system integration are further supporting widespread adoption. Additionally, regulatory focus on safety and the growing need for intelligent transportation systems are reinforcing the importance of LiDAR in shaping the future of connected and autonomous vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $11.3 Billion |

| CAGR | 24.1% |

The automotive LiDAR sensors market is further supported by the rapid deployment of advanced driver assistance technologies in modern vehicles. Automakers are increasingly integrating LiDAR systems to enhance perception capabilities and improve the performance of automated driving features. This growing shift toward higher levels of automation is strengthening the role of LiDAR as a critical component in enabling safer and more reliable vehicle operation. As consumer expectations evolve toward enhanced safety and convenience, the demand for advanced sensing technologies continues to gain momentum, supporting overall market growth.

The passenger vehicles segment held a 44.6% share in 2025, driven by the rising adoption of advanced driver assistance systems in premium and mid-range vehicles. Manufacturers are integrating sophisticated safety and automation features into new vehicle platforms to enhance driving performance and operational efficiency. Increasing consumer focus on safety and advanced functionality is further accelerating the adoption of LiDAR technology within this segment, reinforcing its leading position.

The processing unit segment is anticipated to grow at a CAGR of 26.6% through 2035. This growth is attributed to the increasing need for high-performance computing systems capable of processing complex data generated by LiDAR sensors. Advancements in processing technologies, including artificial intelligence and in-vehicle computing platforms, enable real-time data interpretation and faster decision-making. As autonomous driving systems require rapid and accurate responses, demand for advanced processing units continues to rise significantly.

North America Automotive Lidar Sensors Market accounted for 28.5% share in 2025, supported by the strong adoption of advanced safety technologies and the increasing integration of autonomous features in vehicles. The region is characterized by significant investments in research and development, along with a growing focus on intelligent mobility solutions. Automakers are actively developing LiDAR-enabled systems to improve performance across varying driving conditions. Supportive regulatory frameworks and initiatives promoting innovation in transportation technologies are further contributing to market expansion across the region.

Key companies operating in the Global Automotive Lidar Sensors Market include Luminar Technologies, Ouster Inc., Innoviz Technologies, Hesai Technology, RoboSense (Suteng Innovation), Valeo, Continental AG, Bosch (Robert Bosch GmbH), Denso Corporation, Aeva Technologies, Cepton Inc., Quanergy Solutions, Ibeo Automotive Systems, and Sony Semiconductor Solutions. Companies in the Automotive Lidar Sensors Market are focusing on technological innovation and strategic collaborations to strengthen their competitive position. They are investing heavily in research and development to improve sensor accuracy, range, and cost efficiency while enhancing scalability for mass production. Partnerships with automotive manufacturers and technology firms are helping accelerate integration into next-generation vehicles. Companies are also expanding production capabilities and optimizing supply chains to meet growing demand. Emphasis on software development, including AI-driven perception systems, is improving data processing and real-time decision-making capabilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vehicle type trends

- 2.2.2 Component trends

- 2.2.3 Sales channel trends

- 2.2.4 Technology type trends

- 2.2.5 Range capability trends

- 2.2.6 Application trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of ADAS and semi-autonomous driving features

- 3.2.1.2 Strong push for vehicle safety and evolving regulatory expectations

- 3.2.1.3 Rising demand for 3D mapping and high-definition environmental modeling

- 3.2.1.4 Growing use of LiDAR in commercial vehicles and intelligent mobility ecosystems

- 3.2.1.5 Rapid advancements in low-cost solid-state and FMCW LiDAR

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of LiDAR sensors and system integration

- 3.2.2.2 Limited readiness of supporting autonomous driving infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Growing integration of LiDAR in Level 3 and Level 4 vehicle platforms

- 3.2.3.2 Expansion of LiDAR-enabled smart mobility and commercial fleet automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.3 Commercial vehicles

- 5.4 Off-road vehicles

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Processing unit

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 OEM (original equipment manufacturer)

- 7.3 Tier-1 supplier

Chapter 8 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Mechanical LiDAR

- 8.3 Solid-state LiDAR

- 8.3.1 MEMS-based LiDAR

- 8.3.2 Flash LiDAR

- 8.3.3 Optical phased array (OPA) LiDAR

- 8.3.4 FMCW LiDAR

- 8.4 Hybrid LiDAR

Chapter 9 Market Estimates and Forecast, By Range Capability, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Short-range (<50 meters)

- 9.3 Mid-range (50-170 meters)

- 9.4 Long-range (>170 meters)

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 L2+ ADAS

- 10.3 L3-L5 autonomous driving

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Hesai Technology

- 12.1.2 RoboSense

- 12.1.3 Luminar

- 12.1.4 Valeo

- 12.1.5 Bosch (Robert Bosch GmbH)

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Ouster Inc.

- 12.2.1.2 Aeva Technologies

- 12.2.1.3 Cepton Inc.

- 12.2.1.4 Quanergy Solutions

- 12.2.2 Asia Pacific

- 12.2.2.1 Denso Corporation

- 12.2.2.2 Sony Semiconductor Solutions

- 12.2.3 Europe

- 12.2.3.1 Ibeo Automotive Systems

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Innoviz Technologies

- 12.3.2 Muetec Inc.