PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038357

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038357

Motorcycle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

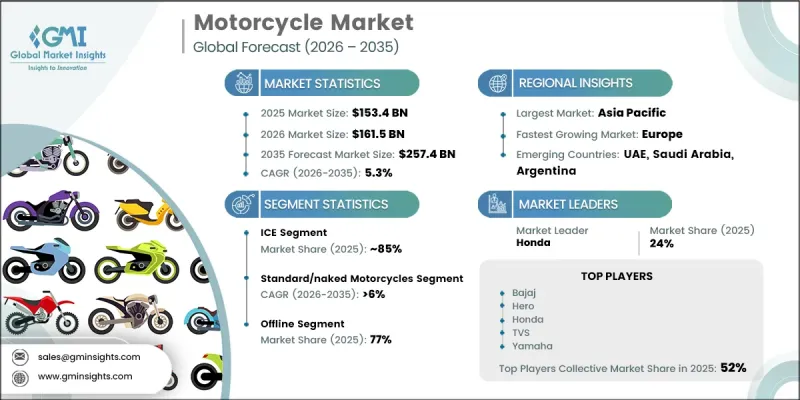

The Global Motorcycle Market was valued at USD 153.4 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 257.4 billion by 2035.

Market growth is fueled by increasing transportation challenges in densely populated areas, where limited parking space and heavy traffic conditions are encouraging the adoption of compact mobility solutions. Motorcycles are widely recognized for offering efficient travel, reduced fuel consumption, and lower ownership costs compared to larger vehicles. The growing need for convenient short-distance transportation and efficient urban mobility is supporting rising demand across both urban and semi-urban regions. In addition, the expanding use of two-wheelers for commercial applications such as delivery and mobility services is further strengthening market growth. Affordability remains a key factor, as motorcycles provide cost-effective transportation options with lower maintenance requirements. At the same time, the industry is witnessing a transition toward electric mobility, supported by regulatory initiatives and advancements in battery performance. Improvements in driving range, operating efficiency, and environmental awareness are accelerating the acceptance of electric motorcycles, contributing to the overall evolution of the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $153.4 Billion |

| Forecast Value | $257.4 Billion |

| CAGR | 5.3% |

The internal combustion engine segment accounted for 85% share in 2025 and is expected to grow at a CAGR of 4% between 2026 and 2035. Continued demand for these motorcycles is driven by their lower initial cost and widespread availability. Their accessibility makes them a preferred option for price-sensitive consumers, particularly in developing regions. In addition, established fueling infrastructure and mature supply chains contribute to their continued dominance, as they offer convenience across diverse geographic areas without reliance on charging networks.

The standard and naked motorcycles segment held 29% share in 2025 and is projected to grow at a CAGR of 6% through 2035. Demand for these models is supported by their balance of performance, comfort, and fuel efficiency, making them suitable for everyday commuting. Their simple design, ease of handling, and relatively low maintenance costs attract a broad consumer base, including first-time buyers. Their lightweight structure and maneuverability also make them well-suited for navigating congested environments, reinforcing their popularity for short-distance travel.

India Motorcycle Market accounted for 34% share and generated USD 57.2 billion in 2025. Strong demand in the country is supported by a large population base and widespread reliance on two-wheelers for daily transportation needs. Rapid urbanization, increasing traffic congestion, and evolving mobility requirements continue to drive adoption. Rising income levels and improved affordability are also encouraging consumers to shift toward more advanced and feature-rich motorcycle models, contributing to sustained market expansion.

Key companies operating in the Global Motorcycle Market include Honda, Yamaha, Bajaj, TVS, Suzuki, Hero, KTM, Kawasaki, Harley-Davidson, and Haojue. Companies in the motorcycle market are strengthening their market position by investing in product innovation and expanding their portfolios to include both conventional and electric models. Manufacturers are focusing on enhancing fuel efficiency, performance, and safety features to meet evolving consumer expectations. Strategic partnerships and collaborations are being utilized to improve technology integration and expand market reach. Companies are also investing in manufacturing capacity and supply chain optimization to ensure consistent product availability. In addition, firms are emphasizing digital sales channels and customer engagement strategies to improve brand visibility. Competitive pricing, financing options, and targeted marketing campaigns are further helping companies attract a wider consumer base and maintain a strong foothold in the global market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Displacement

- 2.2.5 Distribution Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising urbanization and traffic congestion

- 3.2.1.2 Growing demand for fuel-efficient mobility

- 3.2.1.3 Expansion of electric motorcycles

- 3.2.1.4 Increasing disposable income in emerging economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent emission regulations

- 3.2.2.2 High competition and price sensitivity

- 3.2.2.3 Supply chain disruptions

- 3.2.2.4 Safety concerns and accident rates

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in electric two-wheeler segment

- 3.2.3.2 Expansion in Africa and Southeast Asia

- 3.2.3.3 Development of connected motorcycles

- 3.2.3.4 Rise of motorcycle leasing and sharing services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 U.S. Department of Transportation (DOT)

- 3.4.1.5 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Regulation

- 3.4.2.2 CE Marking Compliance

- 3.4.2.3 REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals)

- 3.4.2.4 EU Tire Labelling Regulation

- 3.4.2.5 National Type Approval & Road Homologation Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC)

- 3.4.3.2 Indian Central Motor Vehicle Rules (CMVR)

- 3.4.3.3 Japanese Industrial Standards (JIS)

- 3.4.3.4 ASEAN Harmonized Technical Regulations

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Institute of Metrology (INMETRO) Regulations

- 3.4.4.2 Brazilian National Traffic Council (CONTRAN)

- 3.4.4.3 Mexican NOM Tire Safety Standards

- 3.4.4.4 Regional Import & Certification Requirements

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) Tire Regulations

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.3 South African National Regulator for Compulsory Specifications (NRCS)

- 3.4.5.4 National Road Traffic Act (NRTA) Compliance

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Cruiser motorcycles

- 5.3 Sport motorcycles

- 5.4 Touring motorcycles

- 5.5 Standard/naked motorcycles

- 5.6 Adventure/dual-sport motorcycles

- 5.7 Off-road/dirt motorcycles

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Displacement, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Under 250cc

- 7.3 250cc-500cc

- 7.4 500cc-1000cc

- 7.5 Above 1000cc

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Offline

- 8.3 Online

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Personal

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Manufacturers

- 11.1.1 BMW Motorrad

- 11.1.2 Ducati

- 11.1.3 Haojue

- 11.1.4 Harley-Davidson

- 11.1.5 Honda

- 11.1.6 Kawasaki

- 11.1.7 KTM

- 11.1.8 Suzuki

- 11.1.9 Triumph

- 11.1.10 Yamaha

- 11.2 Regional Manufacturers

- 11.2.1 Hero MotoCorp

- 11.2.2 Bajaj Auto

- 11.2.3 Royal Enfield

- 11.2.4 TVS Motor

- 11.3 Emerging Manufacturers

- 11.3.1 Aprilia

- 11.3.2 Benelli

- 11.3.3 CFMoto

- 11.3.4 Indian Motorcycle

- 11.3.5 MV Agusta

- 11.3.6 Zero Motorcycles