PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038376

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038376

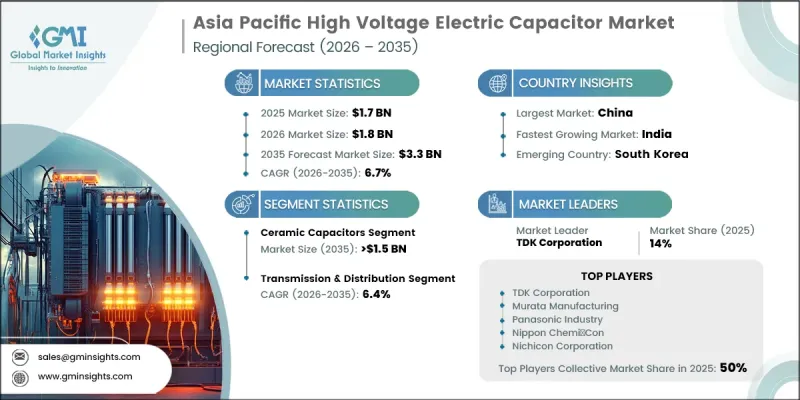

Asia Pacific High Voltage Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia Pacific High Voltage Electric Capacitor Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 3.3 billion by 2035.

The market is evolving rapidly as demand rises for advanced electrical components capable of supporting increasingly complex electronic architectures. Growing integration of sophisticated processing systems across industries is driving the need for higher capacitance and improved performance, which is fueling the adoption of high-voltage electric capacitors across developing economies in the region. At the same time, ongoing advancements in electronic design are placing greater emphasis on compact, efficient, and durable components that can operate under demanding conditions. The expansion of industrialization and infrastructure development is further contributing to market momentum, as power systems require reliable solutions to enhance efficiency and stability. In parallel, technological progress is encouraging the adoption of next-generation capacitor solutions that align with performance expectations and regulatory requirements, strengthening the overall outlook for the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.7% |

The increasing incorporation of electronic control systems in modern vehicles has intensified the demand for capacitors that deliver high performance while maintaining compact size and durability. These components are engineered to function effectively under challenging operating conditions, including high voltage loads and temperature variations, while minimizing resistance and heat generation. Additionally, the regional power sector is witnessing heightened adoption of capacitors due to rising investments in grid infrastructure aimed at meeting growing electricity demand. These components play a critical role in improving system efficiency, enhancing power quality, and reducing transmission losses, which contributes to their expanding utilization. Furthermore, continuous investment in advanced electronic technologies is supporting broader market growth.

The ceramic high voltage electric capacitor segment is projected to reach USD 1.5 billion by 2035. Demand for these capacitors is gaining momentum as industries increasingly prioritize components that offer high reliability, thermal stability, and compact design. Their growing application in energy systems and advanced electronics supports this upward trend.

The consumer electronics segment is expected to grow at a CAGR of 6.9% through 2035. Rising global demand for intelligent and energy-efficient electronic devices is driving this growth trajectory. The implementation of regulatory standards focused on energy efficiency is also encouraging the deployment of advanced capacitor technologies across various applications.

China High Voltage Electric Capacitor Market accounted for USD 600 million in 2025 and is forecast to grow at a CAGR of 7.3% through 2035. Strong economic development, expanding investments in power infrastructure, and favorable policy frameworks are contributing to the country's accelerating market growth.

Key participants in the Asia Pacific High Voltage Electric Capacitor Industry include Murata Manufacturing, TDK Corporation, Panasonic Industry, Samsung Electro-Mechanics, Nichicon Corporation, Nippon Chemi-Con, Rubycon Corporation, Taiyo Yuden, Yageo Corporation, Walsin Technology, Kyocera AVX, ELNA Corporation, Hitachi Energy Xi'an Power Capacitor, AIC Tech, Man Yue Technology Holdings, Seika Electric, Xuansn Electronic, YMIN Capacitors, Yuhchang Electric, and Magnewin Energy. Companies in the Asia Pacific High Voltage Electric Capacitor Market are enhancing their competitive position by focusing on continuous innovation and expanding their product portfolios with advanced, high-efficiency solutions. Strategic collaborations and partnerships are being utilized to strengthen technological capabilities and broaden geographic reach. Many firms are investing in research and development to meet evolving performance standards and regulatory requirements. Capacity expansion and localized manufacturing are helping improve supply chain efficiency and responsiveness to regional demand. Additionally, companies are emphasizing cost optimization, quality enhancement, and customization to address diverse application needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Material trends

- 2.1.3 End use trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.8 Digitalization & IoT integration

- 3.9 Investment analysis & future prospects

- 3.10 Trade data analysis (Driven by Primary Research)

- 3.10.1 Import/export volume & value trends (Driven by Primary Research)

- 3.10.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.11 Price trend analysis (Driven by Primary Research)

- 3.11.1 By material, (USD/Unit) (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the market (Solution Core)

- 3.12.1 AI-driven production optimization (Solution Core)

- 3.12.2 Predictive maintenance & fault detection (Solution Core)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East & Africa

- 4.2.1.5 Latin America

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 key developments

- 4.5.1 Merger & acquisition

- 4.5.2 Partnership & collaboration

- 4.5.3 New product launched

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Material, 2022 - 2035 (USD Million, Million Units)

- 5.1 Key trends

- 5.2 Film capacitors

- 5.3 Ceramic capacitors

- 5.4 Electrolytic capacitors

- 5.5 Others

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million, Million Units)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Automotive

- 6.4 Communication & technology

- 6.5 Transmission & distribution

- 6.6 Others

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Million, Million Units)

- 7.1 Key trends

- 7.2 China

- 7.3 Japan

- 7.4 India

- 7.5 South Korea

- 7.6 Australia

Chapter 8 Company Profiles

- 8.1 AIC Tech

- 8.2 ELNA Corporation

- 8.3 Hitachi Energy Xi'an Power Capacitor

- 8.4 Kyocera AVX

- 8.5 Magnewin Energy

- 8.6 Man Yue Technology Holdings

- 8.7 Murata Manufacturing

- 8.8 Nichicon Corporation

- 8.9 Nippon Chemi-Con

- 8.10 Panasonic Industry

- 8.11 Rubycon Corporation

- 8.12 Samsung Electro-Mechanics

- 8.13 Seika Electric

- 8.14 Taiyo Yuden

- 8.15 TDK Corporation

- 8.16 Walsin Technology

- 8.17 Xuansn Electronic

- 8.18 Yageo Corporation

- 8.19 YMIN Capacitors

- 8.20 Yuhchang Electric