PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045824

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045824

Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

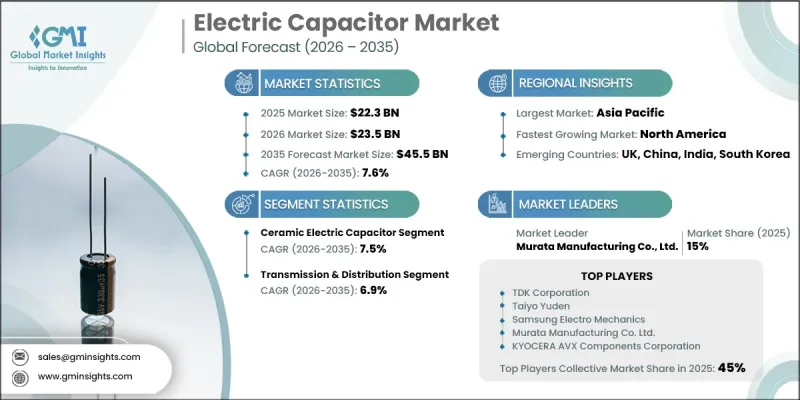

The Global Electric Capacitor Market was valued at USD 22.3 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 45.5 billion by 2035.

The market is witnessing steady expansion as capacitors remain essential components across modern electrical and electronic systems, supporting energy storage, voltage stabilization, and signal processing functions. Rising adoption of advanced electronic devices, coupled with growing integration of high-performance microprocessors, is significantly increasing demand for higher-capacity and compact capacitor solutions. Expanding industrialization and rapid technological adoption in emerging economies are further strengthening market growth. Strong investments in consumer electronics, automotive electrification, and industrial automation are also contributing to sustained demand. In modern electric vehicles, increased use of electronic control units has accelerated capacitor deployment due to their ability to deliver stable performance under high voltage, vibration, and temperature variations while maintaining compact size and lightweight structure. Continuous expansion of manufacturing facilities and increasing electrification trends across industries are further supporting long-term market development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.3 Billion |

| Forecast Value | $45.5 Billion |

| CAGR | 7.6% |

The ceramic capacitor segment is projected to grow at a CAGR of 7.5% through 2035. Ceramic capacitors are widely preferred due to their high reliability, compact structure, and cost efficiency, making them suitable for high-frequency and temperature-intensive applications. The ongoing miniaturization of electronic devices and the rising need for high-density circuit integration have significantly boosted the adoption of multilayer ceramic capacitor technologies across multiple end-use industries.

The transmission and distribution application segment is expected to grow at a CAGR of 6.9% by 2035. Capacitors play a vital role in enhancing grid efficiency, improving power quality, and enabling stable electricity flow across long-distance transmission systems. Increasing electricity demand, coupled with rising integration of renewable energy sources into power grids, is driving the deployment of high-voltage capacitor systems to ensure operational stability and efficiency in modern utility infrastructure.

U.S. Electric Capacitor Market was valued at USD 3.1 billion in 2025 and is projected to grow at a CAGR of 7.8% through 2035. Market expansion in the country is driven by ongoing upgrades to power transmission and distribution infrastructure. Rising adoption of smart grid systems aimed at improving energy efficiency and supporting renewable energy integration is further increasing capacitor utilization across the power sector. Continuous modernization of electrical networks is reinforcing long-term demand growth.

Key players operating in the Global Electric Capacitor Industry include Murata Manufacturing Co., Ltd., TDK Corporation, Panasonic, Samsung Electro Mechanics, Vishay, Yageo Corporation, Nichicon, Siemens, ABB, KYOCERA AVX Components Corporation, Cornell Dubilier, Elna, Havells, ROHM, Schneider Electric, Taiyo Yuden, Walsin, Wima, Kemet, and Xuansn. Companies in the electric capacitor market are actively focusing on miniaturization and high-capacitance development to meet the rising demand from compact electronic systems. Strong investment in research and development is enabling the creation of high-performance, energy-efficient capacitor technologies. Strategic collaborations with automotive and electronics manufacturers are strengthening supply chain integration and product customization capabilities. Manufacturers are also expanding production facilities in high-growth regions to improve cost efficiency and meet localized demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Material trends

- 2.1.3 Polarization trends

- 2.1.4 Voltage trends

- 2.1.5 End use trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.8 Digitalization & IoT integration

- 3.9 Investment analysis & future prospects

- 3.10 Price trend analysis

- 3.10.1 By material, (USD/Unit)

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-driven production optimization

- 3.11.2 Predictive maintenance & fault detection

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East & Africa

- 4.2.1.5 Latin America

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 key developments

- 4.5.1 Merger & acquisition

- 4.5.2 Partnership & collaboration

- 4.5.3 New product launched

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Material, 2022 - 2035 (‘000 Units, USD Billion)

- 5.1 Key trends

- 5.2 Film capacitors

- 5.3 Ceramic capacitors

- 5.4 Electrolytic capacitors

- 5.5 Others

Chapter 6 Market Size and Forecast, By Polarization, 2022 - 2035 (‘000 Units, USD Billion)

- 6.1 Key trends

- 6.2 Polarized

- 6.3 Non-polarized

Chapter 7 Market Size and Forecast, By Voltage, 2022 - 2035 (‘000 Units, USD Billion)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Size and Forecast, By End use, 2022 - 2035 (‘000 Units, USD Billion)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Communications & technology

- 8.5 Transmission & Distribution

- 8.6 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (‘000 Units, USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Austria

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Chile

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Cornell Dubilier

- 10.3 Elna

- 10.4 Havells

- 10.5 Kemet

- 10.6 KYOCERA AVX Components Corporation

- 10.7 Murata Manufacturing Co., Ltd.

- 10.8 Nichicon

- 10.9 Panasonic

- 10.10 ROHM

- 10.11 Samsung Electro Mechanics

- 10.12 Schneider Electric

- 10.13 Siemens

- 10.14 Taiyo Yuden

- 10.15 TDK Corporation

- 10.16 Vishay

- 10.17 Walsin

- 10.18 Wima

- 10.19 Xuansn

- 10.20 Yageo Corporation