PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038387

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038387

Enterprise Asset Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

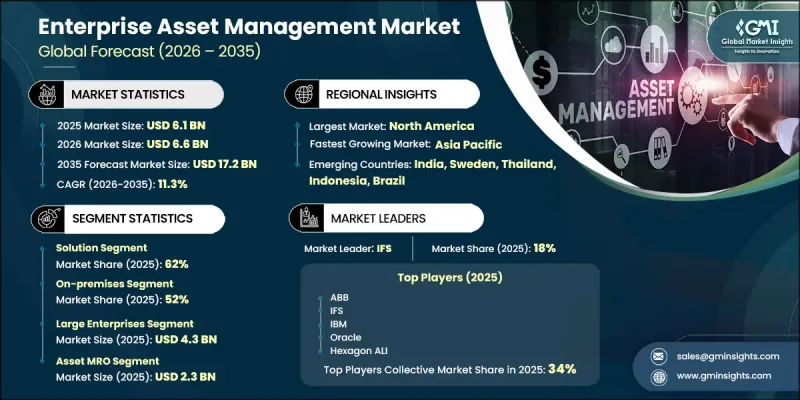

The Global Enterprise Asset Management Market was valued at USD 6.1 billion in 2025 and is estimated to grow at a CAGR of 11.3% to reach USD 17.2 billion by 2035.

Market growth is strongly supported by the rising adoption of digital technologies aimed at improving asset performance, optimizing maintenance schedules, and enabling predictive maintenance strategies across industries. The competitive environment is increasingly shaped by mergers, acquisitions, and strategic partnerships that enhance solution capabilities and market reach. Organizations operating in asset-intensive sectors are leveraging enterprise asset management systems to improve operational efficiency, reduce unplanned downtime, and strengthen decision-making accuracy. Integration of advanced technologies such as artificial intelligence, Internet of Things connectivity, and big data analytics is enabling real-time asset monitoring and delivering predictive insights that improve performance and reduce operational costs. The ongoing shift toward digital transformation in asset management processes is positioning EAM solutions as critical tools for achieving scalable, efficient, and sustainable operations. Although the COVID-19 period initially slowed implementation due to budget limitations, workforce disruptions, and postponed capital investments, it also exposed significant gaps in asset visibility and maintenance planning. This led many organizations to accelerate digital transformation initiatives, strengthening long-term demand for EAM solutions across global industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.1 Billion |

| Forecast Value | $17.2 Billion |

| CAGR | 11.3% |

The solutions segment accounted for 62% share in 2025 and is expected to grow at a CAGR of 10.5% from 2026 to 2035. Growth in this segment is driven by increasing demand for integrated software platforms that enable real-time asset tracking, predictive maintenance, and complete lifecycle management. These solutions support end-to-end asset oversight from procurement to retirement, while incorporating technologies such as artificial intelligence and IoT to enhance predictive analytics capabilities, minimize downtime, and improve overall operational efficiency.

The asset maintenance, repair, and operations segment captured USD 2.3 billion in 2025. This segment is undergoing transformation due to rising digital adoption, cost optimization pressures, and increased infrastructure investments. Organizations are progressively moving away from reactive maintenance approaches toward predictive and condition-based strategies. This shift is supported by the growing deployment of IoT sensors and AI-based failure prediction systems, which are improving asset reliability and reducing maintenance-related disruptions across industrial environments.

United States Enterprise Asset Management Market generated USD 2.1 billion in 2025. Market expansion in the country is driven by the widespread implementation of enterprise asset management frameworks across federal, state, and privately funded infrastructure programs. Government agencies managing large-scale infrastructure portfolios are increasingly adopting structured asset management systems to improve operational efficiency, extend asset lifecycles, and ensure regulatory compliance. This strong institutional adoption continues to reinforce the United States' leadership position in the regional market.

Oracle, SAP, IBM, IFS, AVEVA, ABB, Hexagon ALI, Aptean, CGI, and Salesforce are among the key companies operating in the Enterprise Asset Management Market. Companies in the Enterprise Asset Management Market are focusing on strengthening their competitive position through continuous product innovation and platform integration. They are investing heavily in artificial intelligence, IoT connectivity, and advanced analytics to enhance predictive maintenance capabilities and improve asset lifecycle visibility. Strategic partnerships, mergers, and acquisitions are being used to expand technological capabilities and global market reach. Vendors are also prioritizing cloud-based deployments to improve scalability, flexibility, and cost efficiency for end users. In addition, companies are enhancing mobile accessibility and user experience within EAM platforms to support real-time decision-making. Expansion into emerging markets and industry-specific solution development is further helping firms broaden their customer base and reinforce long-term market presence across diverse industrial sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component

- 2.2.2 Deployment Model

- 2.2.3 Organization Size

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Solution providers & platform vendors

- 3.1.1.2 Implementation partners & system integrators

- 3.1.1.3 Technology enablers & infrastructure providers

- 3.1.1.4 Managed service providers

- 3.1.1.5 End-user organizations

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing need for asset lifecycle optimization

- 3.2.1.2 Rising adoption across asset-intensive industries

- 3.2.1.3 Integration with IoT and predictive maintenance technologies

- 3.2.1.4 Regulatory compliance and asset performance standards

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Data management and migration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Shift toward cloud-based and SaaS EAM platforms

- 3.2.3.2 Integration with AI and advanced analytics

- 3.2.3.3 Increasing adoption of mobile EAM solutions

- 3.2.3.4 Convergence with enterprise systems

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 Inflation Reduction Act (IRA)

- 3.5.1.2 Cybersecurity & Infrastructure Security Framework (CISA)

- 3.5.2 Europe

- 3.5.2.1 European Green Deal

- 3.5.2.2 NIS2 Directive & GDPR Compliance Framework

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Dual Carbon Policy Framework

- 3.5.3.2 Digital India Initiative & Smart Infrastructure Mission

- 3.5.4 Latin America

- 3.5.4.1 Brazil National Infrastructure Modernization Program

- 3.5.4.2 Mexico Energy & Industrial Compliance Standards (NOM Framework)

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Net Zero 2050 Strategy

- 3.5.5.2 Saudi Vision 2030 Industrial Digitalization Program

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Base case scenarios

- 3.11 Use cases

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Asset lifecycle management

- 5.2.2 Predictive maintenance

- 5.2.3 Work order management

- 5.2.4 Labor management

- 5.2.5 Facility management

- 5.2.6 Inventory management

- 5.3 Service

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 On premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprise

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Asset MRO

- 8.3 Linear assets

- 8.4 Non-linear assets

- 8.5 Field service management

Chapter 9 Market Estimates & Forecast By End use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Energy & utilities

- 9.3 Manufacturing

- 9.4 IT & telecom

- 9.5 Healthcare

- 9.6 Oil & gas

- 9.7 Transportation & logistics

- 9.8 Government & public sector

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 ABB

- 11.1.2 Aptean

- 11.1.3 AVEVA

- 11.1.4 CGI

- 11.1.5 IBM

- 11.1.6 IFS A

- 11.1.7 Infor

- 11.1.8 Oracle

- 11.1.9 Salesforce

- 11.1.10 SAP

- 11.2 Regional players

- 11.2.1 Asset Panda

- 11.2.2 AssetWorks

- 11.2.3 eMaint

- 11.2.4 EZOfficeInventory

- 11.2.5 Fleetio

- 11.2.6 Ramco Systems

- 11.2.7 Ultimo Software

- 11.3 Emerging players

- 11.3.1 KloudGin

- 11.3.2 Maintenance Connection

- 11.3.3 UpKeep