PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038426

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038426

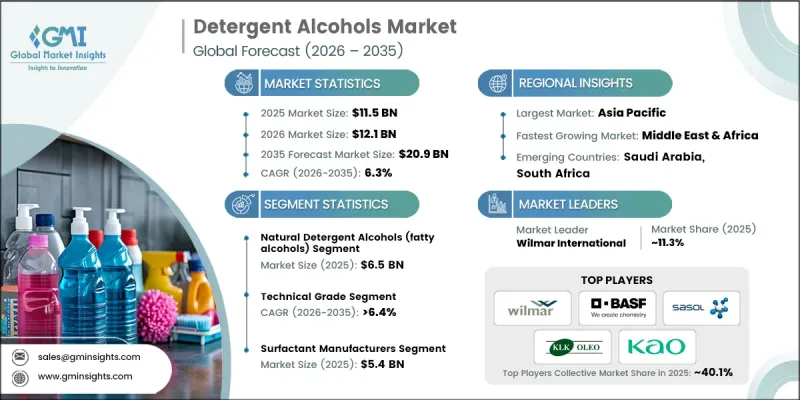

Detergent Alcohols Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Detergent Alcohols Market was valued at USD 11.5 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 20.9 billion by 2035.

The industry continues to expand due to steady demand from both household and industrial cleaning applications, supported by rising awareness of hygiene and growing urban populations. These alcohols play a critical role as base ingredients in surfactant production used across a wide range of cleaning solutions. Increasing consumption of liquid and concentrated detergent formats, along with the expansion of commercial sectors, is reinforcing consistent demand patterns across regions. Changing consumer preferences toward safer, high-performance, and environmentally responsible cleaning products are shaping product development trends. Manufacturers are placing greater emphasis on linear and even-chain alcohols that offer improved biodegradability and formulation adaptability. In addition, growing interest in renewable raw materials is influencing sourcing strategies, while operational enhancements such as regional manufacturing expansion and supply chain optimization are helping companies maintain cost efficiency and product consistency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.5 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 6.3% |

The natural detergent alcohols segment accounted for USD 6.5 billion in 2025 and is expected to grow at a CAGR of 6.8% through 2035. This segment is gaining strong traction due to its compatibility with sustainability goals, including renewable sourcing and enhanced biodegradability. Its suitability for mild and eco-friendly formulations continues to increase its adoption across home care and personal care applications, supported by the rising availability of plant-based raw materials.

The technical grade segment was valued at USD 7.6 billion in 2025 and is projected to grow at a CAGR of 6.4% through 2035. These alcohols remain essential for large-scale surfactant manufacturing, driving consistent demand across high-volume cleaning applications. Other grades are also witnessing growth due to rising requirements for improved purity, stability, and performance across specialized formulations, particularly in hygiene-focused applications.

North America Detergent Alcohols Market accounted for USD 2.4 billion in 2025. The region benefits from a well-established cleaning products industry and a strong focus on premium and sustainable formulations. Demand remains supported by high usage of advanced cleaning solutions and continuous product innovation aimed at improving performance and environmental compatibility.

Key players operating in the Global Detergent Alcohols Market include BASF SE, Wilmar International, Sasol Ltd., KLK Oleo, Kao Corporation, Shell Chemicals (NEODOL), Godrej Industries, SABIC, Musim Mas Holdings, P&G Chemicals, Global Green Chemicals, CREMER OLEO, VVF Ltd., Emery Oleochemicals, and Ecogreen Oleochemicals. Companies in the Detergent Alcohols Market are enhancing their competitive position through strategic investments in sustainable production processes and renewable feedstock integration. They are focusing on improving product quality, yield efficiency, and environmental performance to meet evolving regulatory standards and customer expectations. Expansion of regional production facilities and backward integration strategies are being implemented to manage supply chain risks and raw material volatility. Firms are also entering long-term agreements and collaborations with surfactant manufacturers to secure stable demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Grade

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Natural Detergent Alcohols (Fatty Alcohols)

- 5.2.1 Lauryl Alcohol (Dodecanol)

- 5.2.2 Myristyl Alcohol (Tetradecanol)

- 5.2.3 Cetyl Alcohol (Hexadecanol)

- 5.2.4 Stearyl Alcohol (Octadecanol)

- 5.2.5 Oleyl Alcohol (Octadecenol)

- 5.2.6 Cetyl-Stearyl Alcohol Blends

- 5.2.7 Others

- 5.3 Synthetic Detergent Alcohols

- 5.3.1 Linear Synthetic Alcohols

- 5.3.2 Branched Synthetic Alcohols

- 5.3.3 Others

Chapter 6 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Technical Grade

- 6.3 Cosmetic Grade

- 6.4 Pharmaceutical Grade

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Surfactant Intermediates

- 7.3 Emulsifiers & Viscosity Modifiers

- 7.4 Emollients & Conditioning Agents

- 7.5 Solvents & Carriers

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Surfactant Manufacturers

- 8.3 Consumer Goods Manufacturers

- 8.4 Personal Care & Cosmetics Companies

- 8.5 Industrial & Institutional Suppliers

- 8.6 Specialty Chemical Manufacturers

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Wilmar International

- 10.2 BASF SE

- 10.3 Sasol Ltd.

- 10.4 KLK Oleo

- 10.5 Kao Corporation

- 10.6 Shell Chemicals (NEODOL)

- 10.7 Godrej Industries

- 10.8 SABIC

- 10.9 Musim Mas Holdings

- 10.10 P&G Chemicals

- 10.11 Global Green Chemicals

- 10.12 CREMER OLEO

- 10.13 VVF Ltd.

- 10.14 Emery Oleochemicals

- 10.15 Ecogreen Oleochemicals